Order a report

Custom-made industry research, company ratings, competitor analysis

Investment climate: tax benefits at the increase in control

By the RF Government Resolution as of 27.04.2016 N365 “On amendments to certain acts of the Government of the Russian Federation on provision of state guarantees under credits or bonded loans raised for investment projects implementation”, the procedure for provision of state guarantees under credits or bonded loans raised for investment projects implementation was amended.

The primacy has the protection of the national interests in guarantees against unfair recipients of the state support.

The force of rules of provision of state guarantees under credits or bonded loans for investment projects implementation for legal entities, statutorily selected by the Government, is prolonged for the whole June. The rules were added with the methods of conducting the analyses of the recipient’s financial situation, which will be implemented by Vnesheconombank during the check of the potential recipient’s financial situation at the stage of consideration of documents. Moreover, the list of documents necessary for support granting now also contains the form with the potential recipient’s financial situation data and its compliance with other conditions for granting state guarantees.

After the granting, the recipient is obliged to notify Vnesheconombank on all amendments to the accountings. If there are amendments indicating negative financial situation of the recipient, the state guarantees will be withdrawn.

Along with the state control strengthening, the Government ordering by the President has set profit tax relief for participants of regional investment projects. They are applied by the Federal law N144-FL as of 23.05.2016 “On amendments to Part One and Part Two of the Tax Code of the Russian Federation”.

Now regional authorities are allowed to zero out the profit tax rate or reduce it to 10% for the providers invested from 50 to 500 mln RUB to the manufacturing during 3 years, or over 500 mln RUB for 5 years. In this regard the sales income has to be at least 90% of profit earned by the enterprise.

However the following categories will not be able to get tax benefits: investors already using special tax regimes, residents of special economic zones or members of consolidated group of taxpayers, banks, insurance companies, non-government pension funds, professional participants of the securities market and non-profit organizations.

These amendments to the Tax Code will come into force after a month from the date of the Federal law official publication.

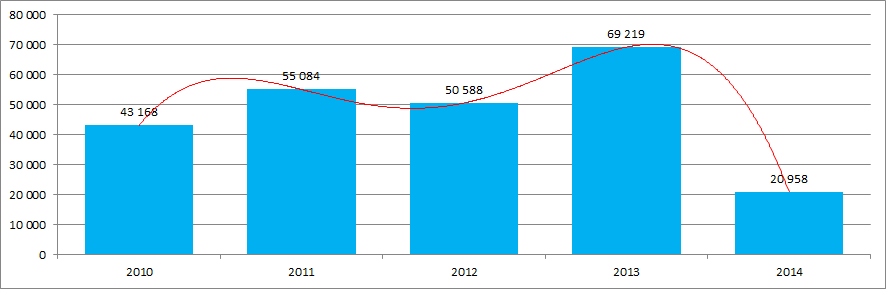

The Government pays careful attention to create favorable environment for investment to the Russian economy for a reason. Reduction in investment is an outstanding feature not only for Russia, but for the world economy in general. According to the data of the United Nations Conference on trade and development (UNCTAD), world foreign direct investment in 2014 reduced by 16,3% and amounted to 1,23 trillion USD. That reduction took place on the background of increase in the gross domestic product, trade, capital investment and employment. The reduction in direct investment to the Russian economy in 2014 was almost 70% in comparison to 2013, which is revealed by the data of the Central Bank of the RF (Picture 1).

Picture 1. Indicators of direct investment to the Russian Federation (according to the balance of payments, mln US dollars)