Order a report

Custom-made industry research, company ratings, competitor analysis

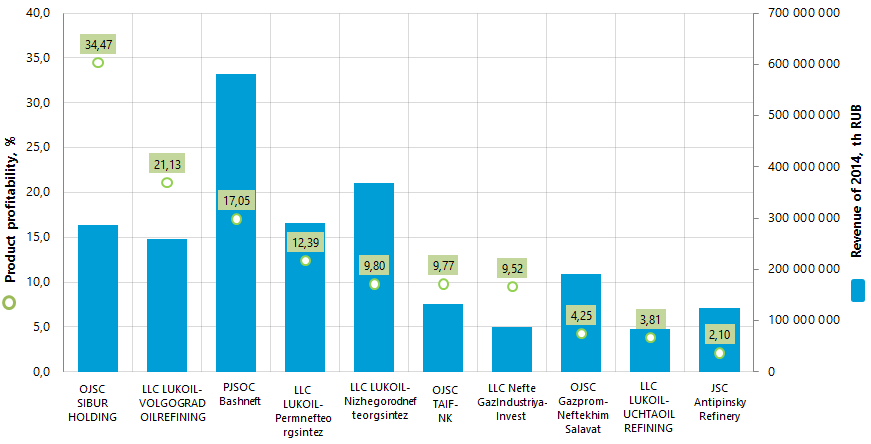

Product profitability ratio of the Russian oil refining companies

Information Agency Credinform has prepared the ranking of the Russian oil refining companies` products. Top-10 enterprises in terms of annual revenue were selected by experts according to the data from the Statistical Register for the latest available period (2014) with oil refining activity. The enterprises were ranked by decrease in the product profitability ratio.

Product profitability is calculated as the ratio of revenue to amount of expenses from ordinary activities. Generally, profitability reflects economic efficiency of production, and product profitability index helps to understand whether output of one or another product is reasonable. There are no specified values for indicators of this group, because they vary strongly depending on the industry.

| № | Name | Revenue of 2014, th RUB | Revenue of 2014 to 2013, %% | Product profitability ratio, % | Solvency index GLOBAS-i® |

|---|---|---|---|---|---|

| 1 | OJSC SIBUR HOLDING INN 7727547261 |

285 545 215 | 117 | 34,47 | 261 High |

| 2 | LLC LUKOIL-VOLGOGRADOILREFINING INN 3448017919 |

259 702 962 | 106 | 21,13 | 158 The highest |

| 3 | PJSOC Bashneft INN 0274051582 |

582 128 345 | 112 | 17,05 | 189 The highest |

| 4 | LLC LUKOIL-Permnefteorgsintez INN 5905099475 |

291 049 782 | 105 | 12,39 | 165 The highest |

| 5 | LLC LUKOIL-Nizhegorodnefteorgsintez INN 5250043567 |

369 313 857 | 105 | 9,80 | 153 The highest |

| 6 | OJSC TAIF-NK INN 1651025328 |

132 010 468 | 104 | 9,77 | 219 High |

| 7 | LLC NefteGazIndustriya-Invest INN 277105194 |

87 281 447 | 126 | 9,52 | 260 High |

| 8 | OJSC Gazprom-Neftekhim Salavat INN 266008329 |

190 633 900 | 114 | 4,25 | 280 High |

| 9 | LLC LUKOIL-UCHTAOILREFINING INN 1102057865 |

83 214 664 | 104 | 3,81 | 221 High |

| 10 | JSC Antipinsky Refinery INN 7204084481 |

124 624 801 | 179 | 2,10 | 315 Satisfactory |

OJSC SIBUR HOLDING takes the lead in the ranking with the product profitability index 34,47%. This is high result twice exceeding industry average index 15,78% and showing the smallest primecost of products in the industry. The company has got high solvency index Globas-i® that shows the ability of the company to pay off the debts in time and to the full extent.

PJSOC Bashneft, showed at the end of 2014 the highest in the industry results according to the revenue value, takes the third place of the ranking with the product profitability index 17,05%, that is close to the industry average index. The enterprise has got the highest solvency index Globas-i® that is a characteristic of high ability to pay off the debts.

However, it worth mentioning that enterprises of the LUKOIL group take the leading position according to the total revenue volume in the industry. This group is represented in the TOP-10 list with four enterprises. The total revenue volume is more than 1,3 trillion RUB that is almost 42% of the TOP-10 total revenue volume. Product profitability indexes of the LUKOIL group range from 21,13% to 3,81%.

JSC Antipinsky Refinery has got the lowest product profitability index among TOP-10 enterprises. Summarizing financial and nonfinancial data, the company has got satisfactory solvency index Globas-i® that is not a guarantee for paying the debts in time and to the full extent. However, this particular enterprise has shown the largest revenue value of 2014 to 2013. Nevertheless, this achievement is negated by the 34 bln RUB loss of 2014 and decreasing product profitability index from 6,29% in 2012 to 2,1% - in 2014.

In general, oil refining companies operate profitably, but demonstrate soft decrease in the average product profitability index: 22,41% - in 2010; 18,7% - in 2011; 15,99% - in 2012; 15,71% - in 2013, with small increase to 15,78% - in 2014. This happened on the back of relatively stable average revenue indexes and high (up to the middle of 2014) global oil prices.

According to the Federal State Statistics Service (Rosstat), in 2015, first in the last few years, 2,4% decrease in primary crude oil processing was observed. Further scenario remains to be seen. According to experts, reserves of the industry are in structural changes and more advanced oil refining.