Order a report

Custom-made industry research, company ratings, competitor analysis

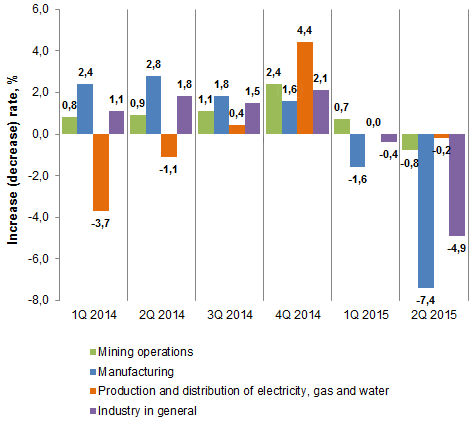

The Russian industry touched the bottom

Following the decline in economic activity and deterioration of macroeconomic conditions (ruble devaluation, bad situation on the commodity markets, high inflation expectations and borrowing rate, sanctions), the significant drop in output is recorded.

The negative dynamics in January-July 2015 compared with January-July 2014 amounted to -3.0%, while the negative developments in the II quarter have intensified: the industry in general fell by 4.9% and manufacturing by 7, 4% over the same period in 2014.

Active consumer demand, which was observed at the end of 2014 (against the national currency upswing), has run low and cannot be the growth driver. On the contrary, today the Russians’ expenses developed, at best, into delayed demand, and in fact are falling following the accrued wages depreciation.

Dynamics of industrial output to the corresponding period of last year, %

Looking at the industry sectors, a positive thing is observed: there are segments that show good growth rates. These include leather production (the growth for the 1st year half was 36%), steel-making equipment (35.7%), canned vegetables (27.6%), cheese (25.7%) etc. (See Table 1).

| № | Commodity group | January-July 2015 in % to January-July 2014 |

|---|---|---|

| 1 | Patent leather and patent laminated leather | 36,0 |

| 2 | Steel-making equipment, casting machines | 35,7 |

| 3 | Counters of production and consumption of the liquid | 31,6 |

| 4 | Canned vegetables and mushrooms | 27,6 |

| 5 | Plastic materials for floor, wall and ceiling covering | 26,1 |

| 6 | Cheese and cheese products | 25,7 |

| 7 | Sheet cast, rolled, drawn and blown glass | 19,7 |

| 8 | Jams, jellies, compotes, fruit and berry puree | 17,7 |

| 9 | Synthetic rubber | 17,5 |

| 10 | Electric motors, DC generators | 17,3 |

On the other hand, there are sectors where the situation is critical (see Table 2): the production of passenger cars decreased by 65.7%; internal combustion engines by 37.3%. That indicates the crisis in the automotive retail sector.

| № | Commodity group | January-July 2015 in % to January-July 2014 |

|---|---|---|

| 1 | Cardboard boxes (transport container) | -65,7 |

| 2 | Mainline passenger cars | -64,7 |

| 3 | Sliced veneer | -60,3 |

| 4 | Men’s trousers | -56,9 |

| 5 | Warm jackets | -55,6 |

| 6 | Mainline freight cars | -54,0 |

| 7 | TV receiving equipment | -40,3 |

| 8 | Golden and silver chains | -40,0 |

| 9 | Copper bars and sections | -39,4 |

| 10 | Internal combustion engines | -37,3 |

Since the inertia is usual for the economic processes, the impact of negative business conditions and fall of consumer demand will be particularly noticeable in the second half of the year. Yet there is no reason to expect the industrial growth recovery. And the events of the second half of August (problems in the Chinese economy, triggering a collapse in international markets) points out a possible sprouting of economic crisis on the top countries of the world.

It is noteworthy that the policy of import substitution initiated by the government, as well as sanctions restrictions on a number of goods from the EU and the United States brought the results: for example, the production of cheese in the 1st year half increased by 25.7%, which will have a positive impact on our food security. With reasonable approach, devaluation of the ruble can be used as an impetus for the industry to domestic counterparts (the development of new industries), and export-oriented companies to sweep new markets.