Order a report

Custom-made industry research, company ratings, competitor analysis

Rating of socio-economic development of the regions

In the April Credinform Newsletter the rating of the Russian regions by socio-economic development is presented.

Development disparity of the Russian regions is long-standing and remains to be one of the key problems for the government and population. Increase in diversity among regions results in disturbance of social equilibrium of the country in general, as well as in differentiation of subject on leaders (minority) with large migration flows directed in, and territories in state of permanent crisis.

First of all, dissimilarity of figures is caused by availability or lack of mineral resources, development of industry and service sector, concentration of economic activity human and financial flows as a result, and climate conditions at a low-grade. As a rule, economic well-being of a region is a key to its good social development level, but there are exemptions: for example, the Republic of Ingushetia is behind by almost all economic indicators, but leads by the average expected lifespan. At the same time, Chukotka autonomous district with very high fiscal revenues, gross regional product and wage level has very low life span (second to last countrywide). In Yamal-Nenets autonomous district, similar to Chukotka by severe climate and economic situation, the life span is considerably higher and increase in population takes place there.

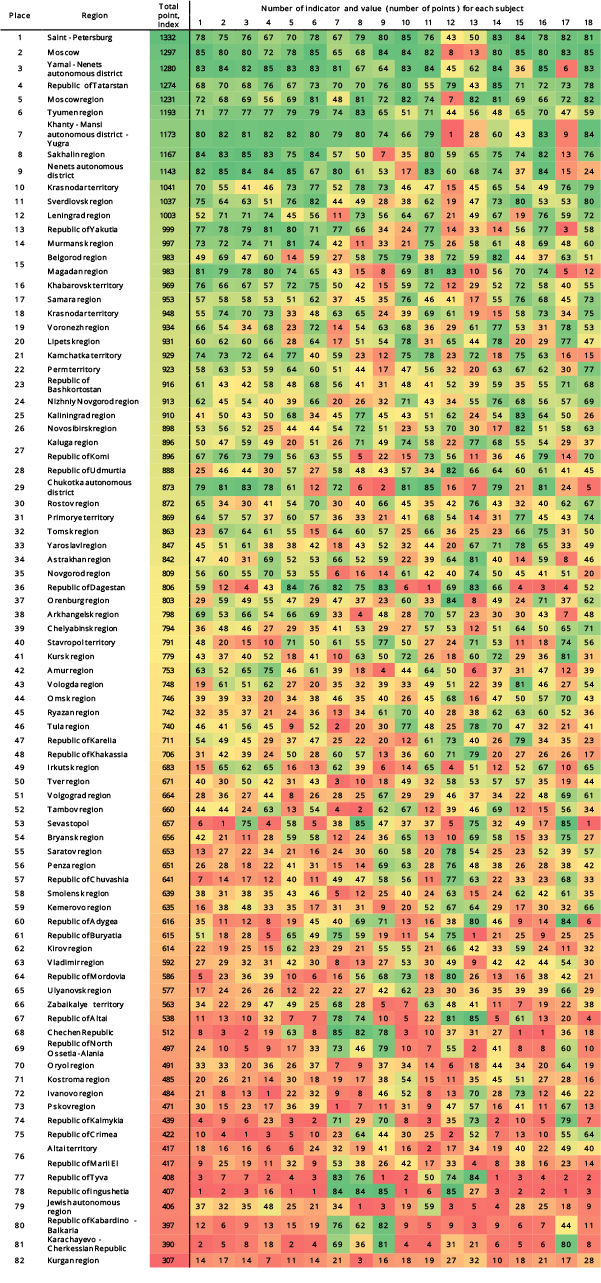

18 figures, the full list of which is presented in Table 1, were used to make a rating. The region can get from 1 to 85 points for each indicator: 85 points go for the best value and 1 for the worst. In summary, the maximum total point (index) is 1530 and the minimal is 18.

The set of indicators shows the development of economic and social potential of every region of the country quite full.

| № | Indicator |

| 1 | Actual final consumption of household per capita by the RF subjects |

| 2 | Gross regional product per capita |

| 3 | Fiscal revenue of the RF subject net of uncompensated receipts per capita |

| 4 | Fixed investment per capita in actual established price |

| 5 | Public catering turnover per capita |

| 6 | Retail sales per capita |

| 7 | Total rate of natural increase per annum |

| 8 | Relative population increase per annum |

| 9 | Life expectancy at birth, both sexes, population at large |

| 10 | Unemployment level, yearly average |

| 11 | Average nominal wage paid |

| 12 | Consumer price index - inflation |

| 13 | Industrial production index |

| 14 | Population with cash income lower than level of the cost of living, as percentage of total population |

| 15 | Number of legal entities per 1000 people of population |

| 16 | Return of taxes and duties to the budget system of the RF by major economic sectors, RUB per 1 resident |

| 17 | Share of old and condemned buildings in the total volume of the housing stock of the RF subject |

| 18 | Fixed assets value at the year-end, by gross book value |

Top three in the rating (see Table 2) consists of Saint-Petersburg with 1332, Moscow (1297) and the Yamal-Nenets autonomous district (1280). Moscow failed to have a lead because of higher annual inflation and lower point for industrial production dynamics. Speaking about relative figures, the capital had decrease in production sector by 3,5% in the past year, and Saint-Petersburg demonstrated increase by 3,9%. However, Moscow got maximum values by the following indicators: actual final consumption of household per capita, number of legal entities per 1000 people of population and fixed assets value. As of St. Petersburg, the level of yearly unemployment is the lowest countrywide, that is why the city got 85 of 85 points. The Yamal-Nenets autonomous district got the highest point for fixed investment per capita and return on taxes and duties to the budget system of the RF per 1 resident.

Sevastopol is the 53rd due to the best indicator of relative population increase (by means of migration) and low percent of condemned buildings. However, the region is at the end by gross regional product per 1 resident and fixed assets value. The Republic of Crimea is the 75th due to poor data on budget income (net of subsidies of the federal center) and fixed investment per capita, as well as high inflation level.

Kurgan region with total index of 307 closes the rating being behind Saint-Petersburg in 4,3 times. The region got high values by none of 18 indicators. Situation both in economic and social sphere is rather bad.

At such a strong level of regional varieties, the state continues to pursue a policy of fiscal equalization redistributing income from “rich” to “poor” that is reasonable under fiscal centralization.

Fundamental changes in the rating should not be expected in a short-term: metropolitan agglomeration and a small group of donor regions concentrating the main resource and industrial potential of the country will keep the leadership in the top ten. In 2017 Moscow stands a good chance to get a leadership in case of local production industry will approach a positive trend.

Speaking about other RF subjects, only the Republic of Crimea is able for significant stabilization due to the range of investment and social programs implemented by the government.

Table 2. Rating of socio-economic development of the regions (Dark green shading – maximum point, dark red shading – minimal point)