Order a report

Custom-made industry research, company ratings, competitor analysis

Trends in brewing

Information Agency Credinform has prepared the review of trends in brewing.

The largest enterprises (TOP-10 and TOP-800) in terms of annual revenue were selected according to the data from the Statistical Register for the latest available periods (2015 and 2016). The analysis was based on data of the Information and Analytical system Globas.

Legal forms and unreliable data

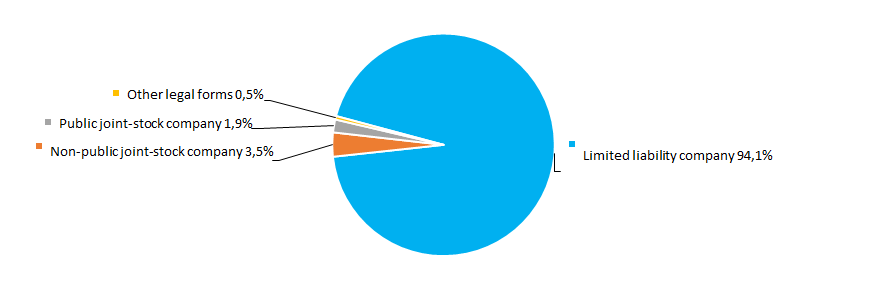

The most popular legal form among companies in the field of brewing is Limited Liability Company. A significant place also take non-public joint stock companies (Picture 1).

Picture 1. Distribution of TOP-800 companies by legal forms

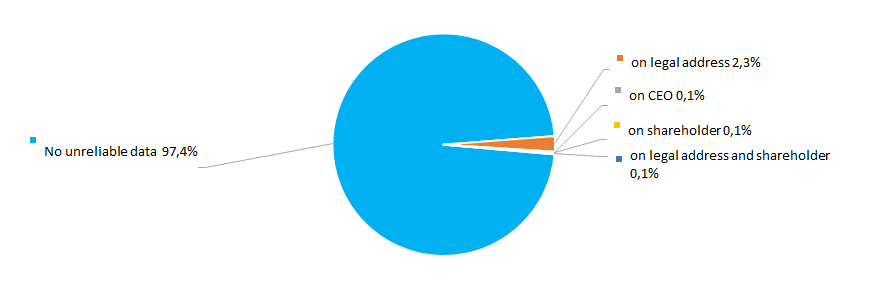

Picture 1. Distribution of TOP-800 companies by legal formsAccording to the results of investigation of the Federal Tax Service of the RF, 2,6% of companies in the industry have records of unreliable data entered into the Unified State Register of Legal Entities (Picture 2).

Picture 2. Shares of TOP-800 companies, having records of unreliable data in the Unified State Register of Legal Entities

Picture 2. Shares of TOP-800 companies, having records of unreliable data in the Unified State Register of Legal EntitiesSales revenue

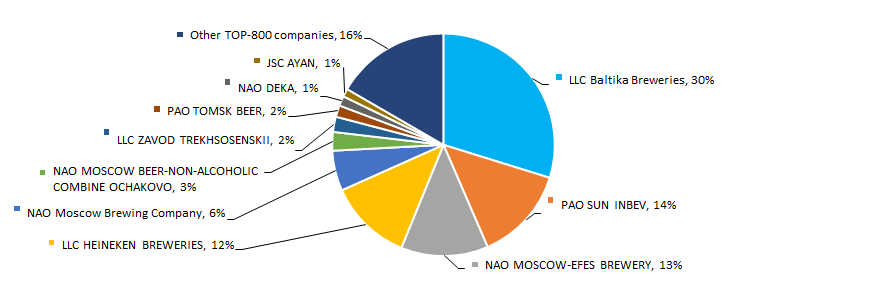

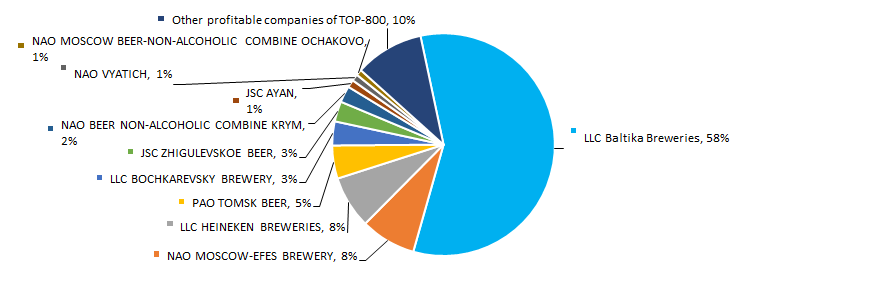

In 2016 total revenue of 10 largest companies amounted to 84% from TOP-800 total revenue. This fact testifies high level of monopolization within the industry. In 2016, the largest company by total revenue is LLC Baltika Breweries (Picture 3).

Picture 3. Shares of TOP-10 companies in TOP-800 total revenue for 2016

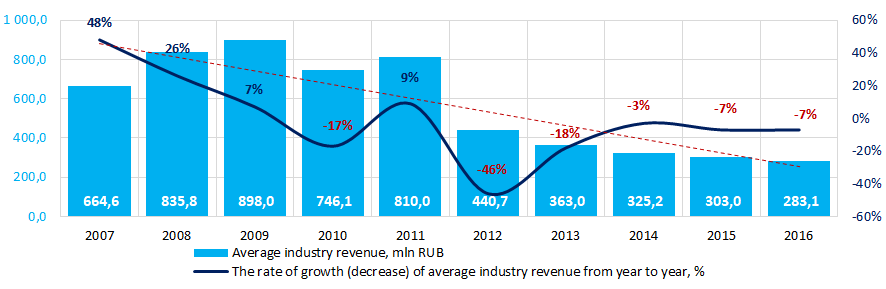

Picture 3. Shares of TOP-10 companies in TOP-800 total revenue for 2016The best results by revenue among the industry for the ten-year period were achieved in 2009. The decrease in average industry indicators was observed within crisis phenomena in the economy in 2010 and 2012-2016. In general, the decrease in sales revenue is observed (Picture 4).

Picture 4. Change of average industry revenue of the companies in the field of brewing in 2007-2016

Picture 4. Change of average industry revenue of the companies in the field of brewing in 2007-2016Profit and loss

In 2016 profit of the 10 largest companies amounted to 90% from TOP-800 total profit. In 2016, the leading position by profit also takes LLC Baltika Breweries (Picture 5).

Picture 5. Shares of TOP-10 companies in TOP-800 total profit for 2016

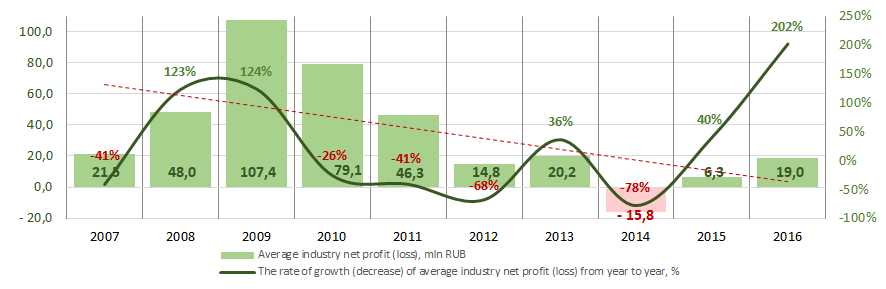

Picture 5. Shares of TOP-10 companies in TOP-800 total profit for 2016For the ten-year period, the average industry revenue values of companies in the field of beer production are not stable. The negative values were observed in 2014 against the background of crisis phenomena in the economy. In recent years, the growth of indicators is observed, however, in general, the revenue ratios demonstrate decreasing tendency. The best results of the industry were observed in 2009 (Picture 6).

Picture 6. Change of average industry profit of the companies in the field of beer production in 2007-2016

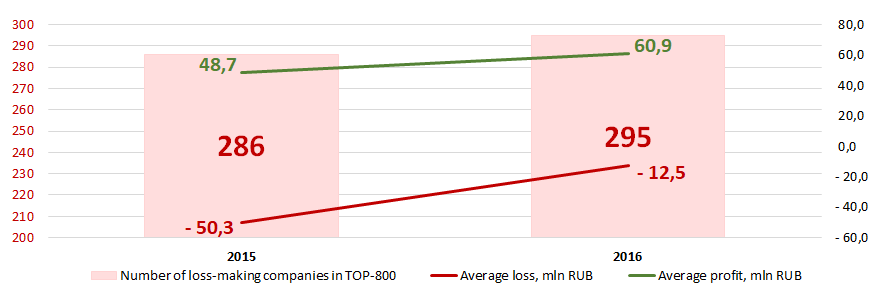

Picture 6. Change of average industry profit of the companies in the field of beer production in 2007-2016In 2015, the TOP-800 list included 286 loss-making companies. In 2016 the number of loss-making companies increased to 295 or by 3%. Meanwhile, their average loss decreased by 75%. The average profit of other companies from TOP-800 list increased by 25% for the same period (Picture 7).

Picture 7. Number of loss-making companies, average loss and profit within TOP-800 companies in 2015 – 2016

Picture 7. Number of loss-making companies, average loss and profit within TOP-800 companies in 2015 – 2016Main financial indicators

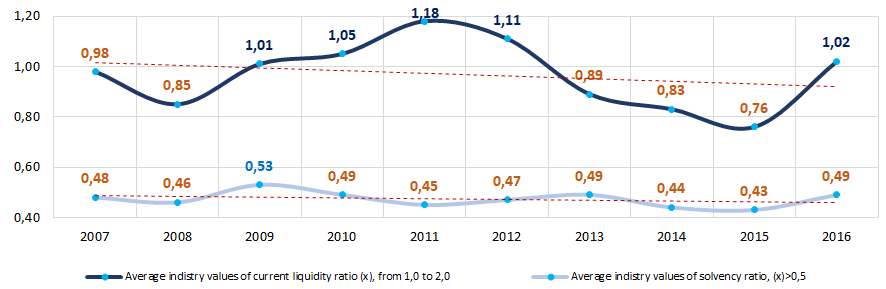

For the ten-year period, the average industry values of current liquidity ratio within five years were lower than recommended values - from 1,0 to 2,0. (yellow color on Picture 8).

Current liquidity ratio (ratio of total working capital to short-term liabilities) shows the sufficiency of company’s assets to meet short-term obligations.

Solvency ratio (ratio of equity capital to total balance) shows the company’s dependence from external borrowings. The recommended value of the ratio is >0,5. The ratio value less than minimum limit signifies about strong dependence from external sources of funds.

The calculation of practical values of financial indicators, which might be considered as normal for a certain industry, has been developed and implemented in the Information and Analytical system Globas by the experts of Information Agency Credinform, taking into account the actual situation of the economy as a whole and the industries. In 2016 the practical value of solvency ratio for the companies in the field of beer production is from -0,12 to 0,41.

For the ten-year period, the average industry values of the ratio within nine years were lower than recommended values and higher than practical values (Picture 8).

In general, the downtrend is observed for both ratios.

Picture 8. Changes of average industry values of current liquidity ratio and solvency ratio of companies in the field of beer production in 2007 – 2016

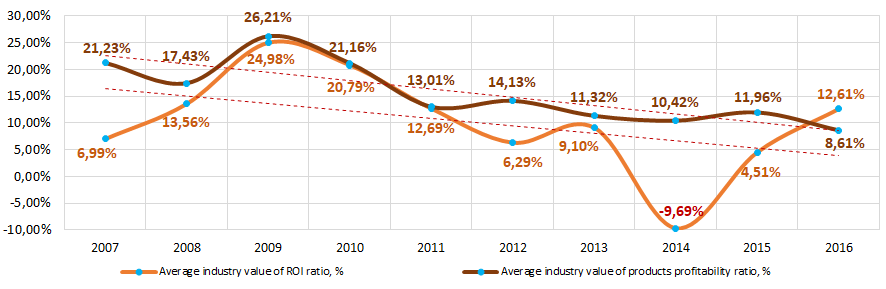

Picture 8. Changes of average industry values of current liquidity ratio and solvency ratio of companies in the field of beer production in 2007 – 2016 For the last ten years, the instability of ROI ratio was observed. In the period of crisis phenomena in the economy in 2014 the ratio decreased to negative values (Picture 9). The ROI ratio is calculated as a ratio of net profit to sum of stockholder equity and long-term liabilities and shows the return from equity involved in commercial activities and long-term borrowed funds.

Within the same period, the products profitability ratio was also unstable (Picture 9). Product profitability ratio is a ratio of sales profit to general expenses. In general, the profitability characterizes the production efficiency.

The greatest growth of indicators was observed in 2009. In general, the ratios demonstrate the negative trend.

Picture 9. Changes of average industry values of ROI ratio and products profitability ratio of companies in the field of beer production in 2007 – 2016

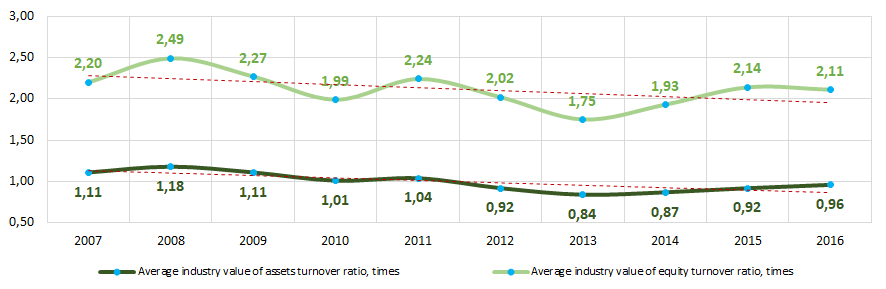

Picture 9. Changes of average industry values of ROI ratio and products profitability ratio of companies in the field of beer production in 2007 – 2016Assets turnover ratio is the ratio of sales revenue and company’s average total assets for a period. It characterizes the effectiveness of using of all available resources, regardless the source of their attraction. The ratio shows how many times per year the full cycle of production and circulation is performed, generating the corresponding effect in the form of profit.

Equity turnover ratio is calculated as a ratio of revenue to yearly average sum of equity and demonstrates the company’s usage rate of total assets.

For the ten-year period, both ratios demonstrated relative stability with slight downtrend (Picture 10).

Picture 10. Changes of average industry values of activity ratios of companies in the field of beer production in 2007 – 2016

Picture 10. Changes of average industry values of activity ratios of companies in the field of beer production in 2007 – 2016Dynamics of business activity

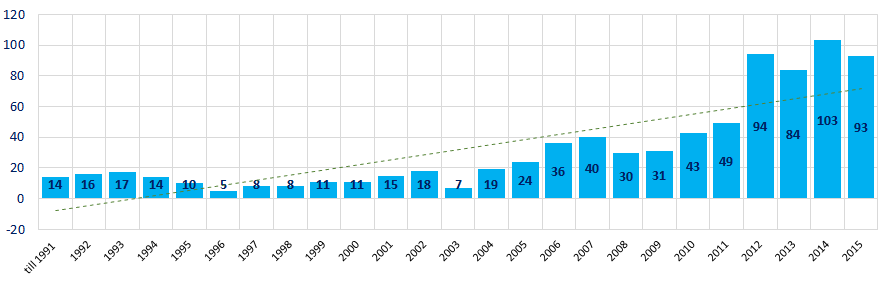

Over a 25-year period, the registered companies from TOP-800 list are unequally distributed by the year of foundation. Most of the companies engaged in beer production were founded in 2014. In general, the increasing tendency is observed (Picture 11).

Picture 11. Distribution of TOP-800 companies by the year of foundation

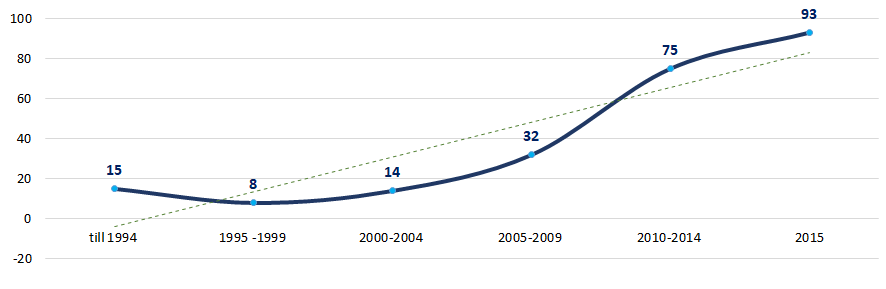

Picture 11. Distribution of TOP-800 companies by the year of foundationThe most outstanding interest of business to beer production is observed after 2010 (Picture 12).

Picture 12. Average number of TOP-800 companies, registered within a year, by year of foundation

Picture 12. Average number of TOP-800 companies, registered within a year, by year of foundation Main regions of activity

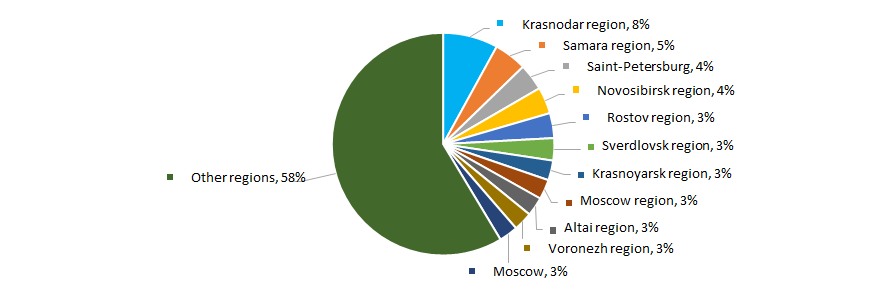

Companies in the field of beer production rather equally distributed across the country. Most of them are registered in Krasnodar region – the region with developed infrastructure of agriculture and food industry (Picture 13).

TOP-800 companies are registered in 78 regions of the Russian Federation.

Picture 13. Distribution of TOP-800 companies by Russian regions

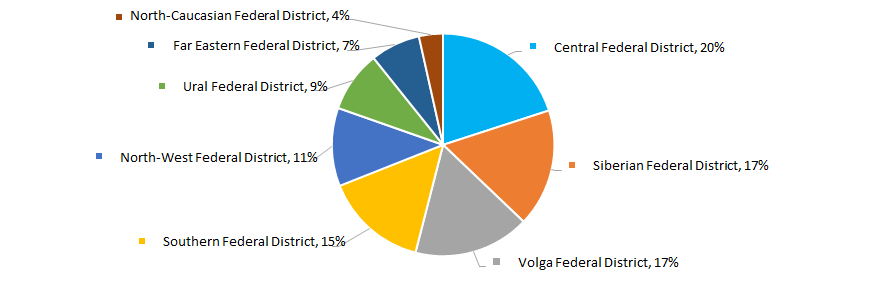

Picture 13. Distribution of TOP-800 companies by Russian regionsMost of the companies of the industry are concentrated in the Central Federal District (Picture 14).

Picture 14. Distribution of TOP-800 companies by Federal Districts of Russia

Picture 14. Distribution of TOP-800 companies by Federal Districts of RussiaThe share of companies from TOP-800 list with branches or representative offices amounted to 2,4%.

Participation in arbitration proceedings

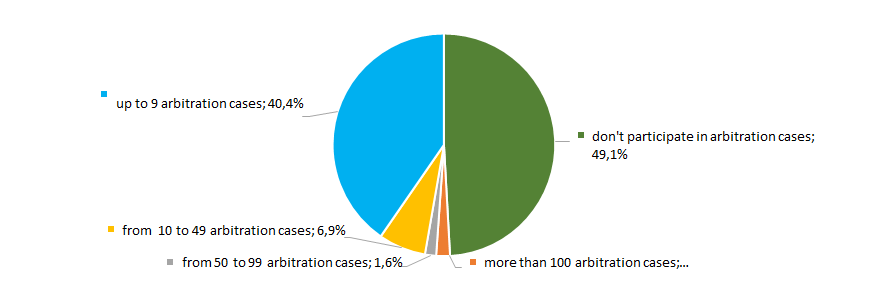

Most companies of the sector either do not participate in arbitration proceedings, or participate in a small number of cases (Picture 15).

Picture 15. Distribution of TOP-800 companies by participation in arbitration proceedings

Picture 15. Distribution of TOP-800 companies by participation in arbitration proceedingsReliability index

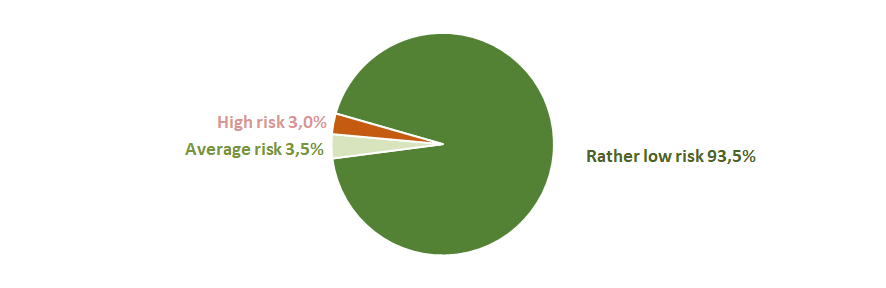

The risk of meeting a fly-by-night company or an unreliable company is extremely low for the most companies of the sector (Picture 16).

Picture 16. Distribution of TOP-800 companies by reliability index

Picture 16. Distribution of TOP-800 companies by reliability indexFinancial position score

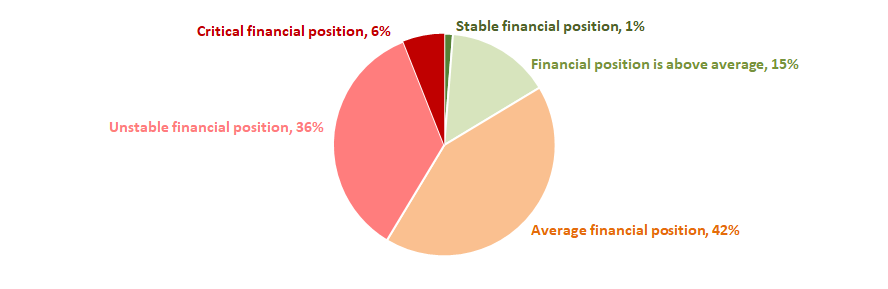

The assessment of company’s financial position shows that more than one third of companies are in unstable and critical financial position and the same number of companies have average financial position (Picture 17).

Picture 17. Distribution of TOP-800 companies by financial position score

Picture 17. Distribution of TOP-800 companies by financial position scoreLiquidity index

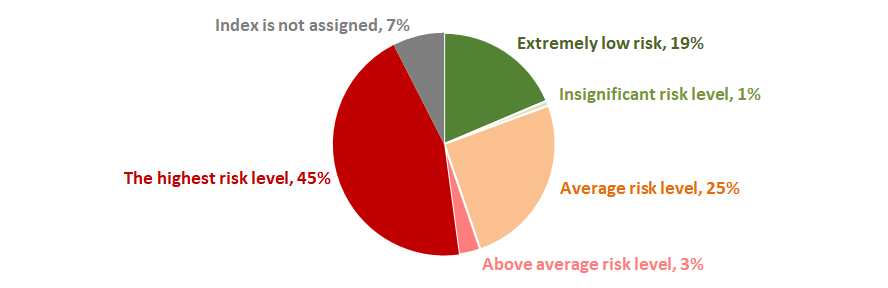

Almost more than a half of industry companies have the highest or above average level of bankruptcy risk in the short-term period (Picture 18).

Picture 18. Distribution of TOP-800 companies by liquidity index

Picture 18. Distribution of TOP-800 companies by liquidity indexSolvency index Globas

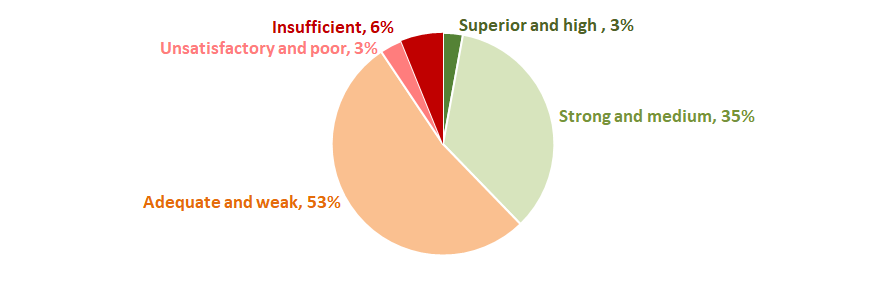

More than a half of TOP-800 companies have adequate and weak solvency index Globas. Thus, almost more than one third of companies have superior, high or strong, medium solvency index Globas (Picture 19).

Picture 19. Distribution of TOP-800 companies by solvency index Globas

Picture 19. Distribution of TOP-800 companies by solvency index Globas Hereby, the complex assessment of beer production companies, taking into account main indexes, financial ratios and indicators, shows negative trends in this field of activity. However, in the last two years, the industry situation started to stabilize.