Order a report

Custom-made industry research, company ratings, competitor analysis

Dynamics of investment activity in Russia: state and prospects

In 2014 there was a slump of foreign investment in the Russian economy. According to the data of the Bank of Russia, direct foreign investment in the non-banking sector of RF were amounted to USD 20, 2 bln., following the results of the first half of 2014; that is 52% less than in the same period of 2013.

Sanctions from the Occident as well as economic slowdown and devaluation of the rouble have resulted in reduction of the foreign capital inflows. A high degree of uncertainty concerning the country’s economy development still remains; that makes investors to wait for better period. At the same time active investment inflow in 2018 is expected due to the gas supply through the Sila Sibiri (the Power of Siberia) gas pipeline and holding FIFA World cup in Russia.

One of the sources of investment in the economy of RF can be foreign legal entities, acting as shareholders of Russian companies. According to the data of the Information and analytical System GLOBAS-i of Credinform agency, 47 954 companies with foreign shareholders are registered in Russia. 53% of them own 100% of authorized capital. It bears reminding, that in 2013 this index was 52%.

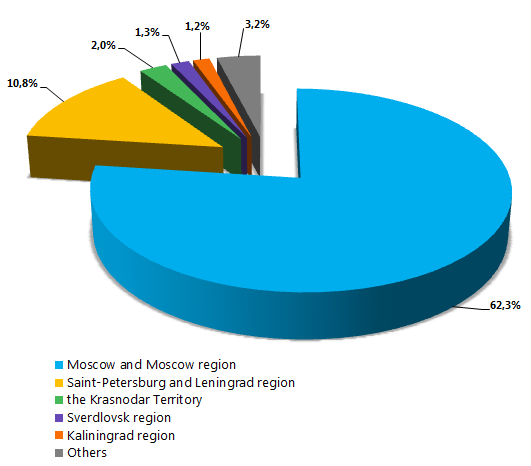

The majority of 47 954 companies with foreign capital are located in Moscow and Moscow region (62,3%), Saint-Petersburg and Leningrad region (10,8%) and the Krasnodar Territory (2%). Companies with the following activity types are leaders among Russian enterprises: wholesale, lease of own real estate and consulting in the field of business and management.

Figure. Allocation of companies with foreign capital by the subjects of Russia

Slump of foreign investment in the Russian economy is observed against capital outflow. According to the data of the Higher School of Economics, net capital outflow from Russia has exceeded USD 110 bln from January 2014; that goes beyond all official forecasts. As a reminder, in the estimation of the Ministry of Economic Development of the Russian Federation net capital outflow for 2014 had to be amounted to USD 100 bln. At the same time the Bank of Russia has announced USD 90 bln amount.

However devaluation of the rouble together with food embargo have resulted in total imports reduction; this helped to strengthen the trade balance under the conditions of export revenue stagnation. As a result monies transferred in Russia not only exceeded payments to other countries and international organizations, but also doubled for 3 quarters of 2014 and amounted to USD 52,3 bln in comparison with the same period of the previous year. Almost two-thirds of its growth is accounted for reduction of visible imports by 6,4%, to the amount of USD 232,7 bln. At the same time export remains at last year’s level with amount of USD 383,8 bln.

Foreign investment play a major role in the development of the country’s economy, because modern technologies, new management methods, highly qualified specialists are attracted together with investment; manpower skills also grows.

Along with that the general trend of capital outflow from emerging markets should be noted. Investors are waiting for stabilization of the situation with the object of getting high return on investment. But in spite of even the most favorable rates, the situation can be stabilized not earlier than in the second half of 2015.