Order a report

Custom-made industry research, company ratings, competitor analysis

Inventory turnover of sugar manufacturers

Information Agency Credinform has prepared the ranking of inventory turnover of sugar manufacturers. The largest enterprises in terms of revenue volume (TOP-10) were selected according to the data from the Statistical Register for the latest available periods (2015 - 2017). Then they were ranked by decrease in inventory turnover ratio (Table 1). The analysis was made on the basis of the data of the Information and Analytical system Globas.

Inventory turnover (times) is a ratio of revenue to average value of inventories for a period. The ratio shows rate of inventory realization.

Inventory turnover characterises mobility of funds that the company invests in inventories: the faster monetary funds invested in inventories are regained in the form of revenue from sale of finished products, the higher is business activity and efficiency of the recources use with time effect.

There are no recommenmded values for this indicator, because they vary strongly depending on the industry. The higher is value, the better. The experts of the Information agency Credinform, taking into account the actual situation both in the economy as a whole and in sectors, has developed and implemented in the Information and Analytical system Globas the calculation of practical values of financial ratios that can be recognized as normal for a particular industry. For sugar producing companies the practical value of inventory turnover ratio was from 3,01 in 2017.

For getting of the most comprehensive and fair picture of the financial standing of an enterprise it is necessary to pay attention to all combination of indicators and financial ratios.

| Name, INN, region | Revenue, billion RUB | Net profit (loss), billion RUB | Inventory turnover, times | Solvency index Globas | |||

| 2016 | 2017 | 2016 | 2017 | 2016 | 2017 | ||

| 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 |

| LLC RUSAGRO-BELGOROD INN 3126019943 Belgorod region |

|

|

|

|

|

|

249 Strong |

| LLC RUSAGRO-TAMBOV INN 6804008674 Tambov region |

|

|

|

|

|

|

222 Strong |

| LLC AGROSNABSAKHAR INN 4826050108 Lipetsk region |

|

|

|

|

|

|

254 Medium |

| JSC LENINGRADSKY SUGAR PLANT INN 2341006687 Krasnodar territory |

|

|

|

|

|

|

210 Strong |

| JSC USPENSKIY SAHARNIK INN 2357005329 Krasnodar territory |

|

|

|

|

|

|

183 High |

| LLC KRISTALL INN 6824004406 Tambov region |

|

|

|

|

|

|

269 Medium |

| JSC Olkhovatsky Sugar Factory INN 3618003708 Voronezh region |

|

|

|

|

|

|

188 High |

| JSC Zainsky Sakhar INN 1647008721 The Republic of Tatarstan |

|

|

|

|

|

|

233 Strong |

| JSC SUGAR PLANT DOBRINSKI INN 4804000086 Lipetsk region |

|

|

|

|

|

|

198 High |

| JSC ELAN-KOLENOVSKII SUGAR PLANT INN 3617006819 Voronezh region |

|

|

|

|

|

|

189 High |

| Total for TOP-10 companies | |

|

|

|

|||

| Average value for TOP-10 companies | |

|

|

|

|

|

|

| Average industrial value | |

|

|

|

|

|

|

![]() growth decrease of indicator to the previous period,

growth decrease of indicator to the previous period, ![]() decrease of indicator to the previous period.

decrease of indicator to the previous period.

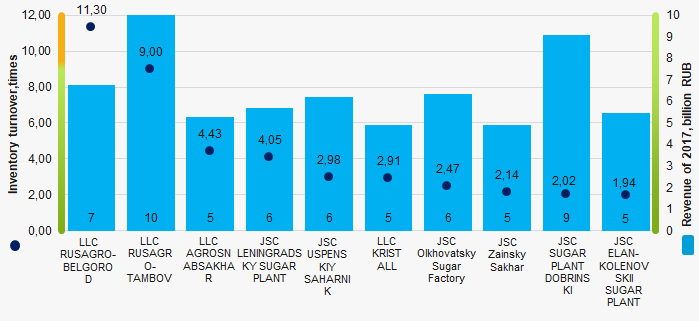

The average indicator of the inventory turnover ratio of TOP-10 companies is above the industry average value and the practical one. In 2017 three companies out of TOP-10 have improved their indicators.

Picture 1. Inventory turnover ratio and revenue of the largest Russian sugar manufacturers (TOP-10)

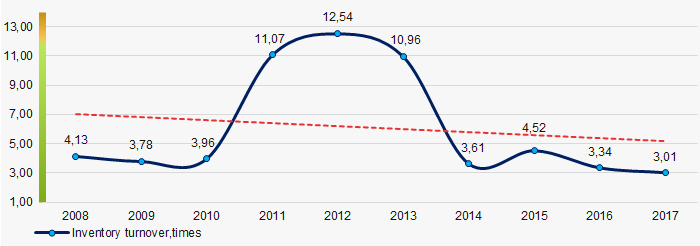

Picture 1. Inventory turnover ratio and revenue of the largest Russian sugar manufacturers (TOP-10)Over a ten-year period the industry average indicators of the inventory turnover ratio have decreasing tendency. (Picture 2).

Picture 2. Change in the average industry values of the inventory turnover ratio of the largest Russian sugar manufacturers in 2008 – 2017

Picture 2. Change in the average industry values of the inventory turnover ratio of the largest Russian sugar manufacturers in 2008 – 2017