Order a report

Custom-made industry research, company ratings, competitor analysis

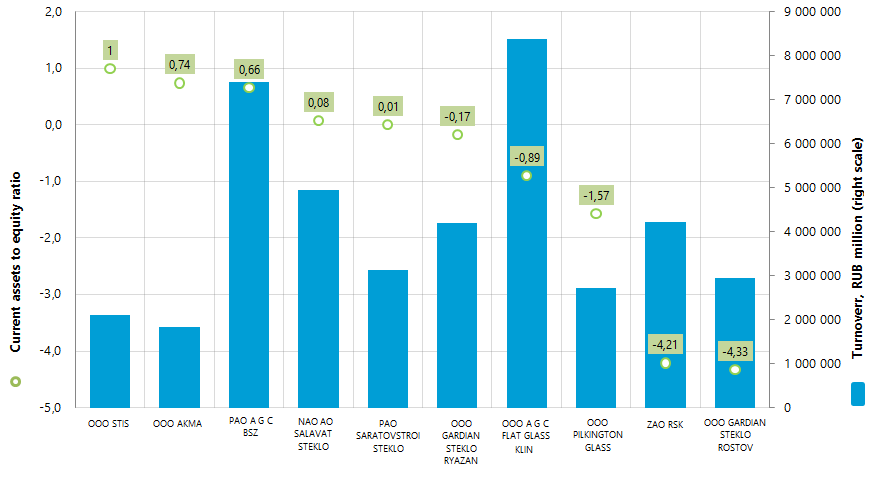

Current assets to equity ratio of plate glass manufacturers

Information agency Credinform has prepared the ranking of plate glass manufacturers on current assets to equity ratio. The largest companies in this industry by revenue from sale for the last available in the Statistical register period (2014) were taken for the investigation. Further the Top-10 enterprises by revenue were ranked in the descending order of current assets to equity ratio value.

Current assets to equity ratio (х) shows the ability of an enterprise to control the rate of own working capital and replenish current assets in case of need at its own sources. This indicator is calculated as a ratio of company’s own current assets to the total sum of own assets. Recommended value: from 0,2 to 0,5.

Decrease of an indicator designates the possible delay in payment of receivables or tightening of trade credit conditions on the part of suppliers or contractors.

| № | Name, tax number | Region | Revenue for 2014 г., RUB million | Current assets to equity ratio, (х) | Solvency index Globas-i® |

|---|---|---|---|---|---|

| 1 | ООО STIS Tax number 6451415520 |

Moscow region | 2 113 458 | 1,00 | 228 (high) |

| 2 | ООО AKMA Tax number 7808032006 |

Saint-Petersburg | 1 836 908 | 0,74 | 262 (high) |

| 3 | PAO A G C BSZ Tax number 5246002261 |

Nizhny Novgorod region | 7 407 998 | 0,66 | 186 (prime) |

| 4 | NAO AO SALAVATSTEKLO Tax number 0266004050 |

Republic of Bashkortostan | 4 942 687 | 0,08 | 208 (high) |

| 5 | PAO SARATOVSTROISTEKLO Tax number 6453054397 |

Saratov region | 3 123 517 | 0,01 | 289 (high) |

| 6 | ООО GARDIAN STEKLO RYAZAN Tax number 6234017547 |

Ryazan region | 4 202 786 | -0,17 | 252 (high) |

| 7 | ООО A G C FLAT GLASS KLIN Tax number 5020033028 |

Moscow region | 8 392 857 | -0,89 | 313 (satisfactory) |

| 8 | ООО PILKINGTON GLASS Tax number 5040054932 |

Moscow region | 2 727 782 | -1,57 | 268 (high) |

| 9 | ZAO RSK Tax number 7802445776 |

Saint-Petersburg | 4 210 347 | -4,21 | 217 (high) |

| 10 | ООО GARDIAN STEKLO ROSTOV Tax number 6148559000 |

Rostov region | 2 948 023 | -4,33 | 302 (satisfactory) |

The first spot of the ranking is taken by OOO Stis with the value of current assets to equity ratio that equals to 1,00. It shows that all company’s own working capital is in turnover and gives evidence to the high degree of freedom to manipulate own assets. The company was given the high solvency index Globas-i® by the experts of Information agency Credinform, which characterize it as a financially stable.

Figure. Current assets to equity ratio of the largest plate glass manufacturers in Russia, Top-10

The industry leader by turnover OOO A G C Flat Glass Klin is placed on the seventh spot of the ranking with the current assets to equity ratio value that equals to -0,89 and satisfactory solvency index Globas-i®.

None of the represented companies in the Top-10 fit in the ratio statutory value. The closest to the statutory values are the indicators 0,66 and 0,08 belonging to PAO A G C BSZ and NAO AO Salavatsteklo respectively, having the prime and high solvency index Globas-i®.

Following the results of 2014 the industry-average indicator of current assets to equity ratio amounted to -1,8, which in the whole speaks for irrational use of the working capital. The indicators of ZAO RSK and OOO Gardian Steklo Rostov are lower that the industry-average ones. It means that the companies have the low mobility rate of own assets due to the fact that the major part of them is invested in the slowly realizable assets instead of the currents assets.