Order a report

Custom-made industry research, company ratings, competitor analysis

Russia is first in Europe by the industrial production volume

Development of countries in the post-industrial period leads to paradoxical results: countries with up-to-date export-oriented manufacturing will benefit in the long view. Russia is among them.

Nominal GDP volume – the market price of all produced goods and rendered services over a year – is one of the key figures in international comparison of economic development of countries and territories.

Nowadays, services sector is prevalent in modern economies. The majority of countries have embraced the post-industrial period. However, we still in need of houses, electric power and manufactured goods.

GDP calculated using the purchasing power parity (PPP) reflects more objectively the achievements of various countries. Data on contribution of manufacturing to GDP makes it possible to compare countries, assess their significance and share in global industrial production.

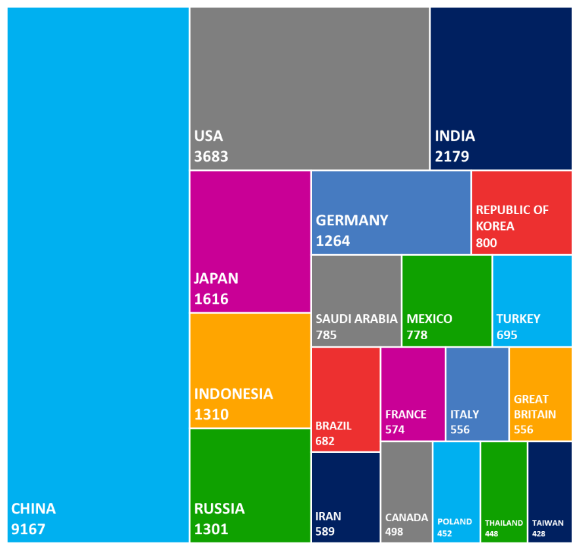

Speaking about the figures, China reasonably has status of “the world’s factory”. Following the results of 2017, over 24% of total industrial production at the amount of 9 167 billion USD at PPP fell for its share. Production makes 39,5% of GDP in China (see Table 1).

Considered as the industrial leader over the last century, now the USA yields the palm: the country produces goods at the amount of 3 683 billion USD or 9,7% of global production, that is 2,5 times less than in China. The United States is trapped with globalization: at the time, American companies have transferred operations to China. This was resulted in huge negative trade balance, which forms particularly due to the trade with China. The country has to import on a massive scale. In this regard, it could well be understood in attempts to remedy the situation by introducing protective duties to reduce dependence on imports.

Being ahead of Germany, Russia is the first in Europe and sixth in the world by industrial production. Our country has developed fuel and energy complex, as well as advanced developments and orders in nuclear power, military-industrial complex, metallurgy, and chemical industry. By the trade surplus volume (when export exceeds import) in absolute monetary terms, Russia ranks third after China and Germany.

| Position | Country | Industrial output volume at PPP, billion USD | Share of manufacturing in GDP, % | Share in global industrial output volume, % | GDP at PPP, billion USD |

| 1 | China | 9 167 | 39,5 | 24,2 | 23 208 |

| 2 | USA | 3 683 | 18,9 | 9,7 | 19 485 |

| 3 | India | 2 179 | 23,0 | 5,8 | 9 474 |

| 4 | Japan | 1 616 | 29,7 | 4,3 | 5 443 |

| 5 | Indonesia | 1 310 | 40,3 | 3,5 | 3 250 |

| 6 | Russia | 1 301 | 32,4 | 3,4 | 4 016 |

| 7 | Germany | 1 264 | 30,1 | 3,3 | 4 199 |

| 8 | Republic of Korea | 800 | 39,3 | 2,1 | 2 035 |

| 9 | Saudi Arabia | 785 | 44,2 | 2,1 | 1 775 |

| 10 | Mexico | 778 | 31,6 | 2,1 | 2 463 |

| - | Top-10 | 22 883 | 30,4 | 60,5 | 75 348 |

| - | Other countries | 14 928 | 28,4 | 39,5 | 52 525 |

| - | Total | 37 811 | 29,6 | 100 | 127 873 |

Source: IMF, World Economic Outlook Database, Credinform calculations

Picture 2 shows distribution of countries by contributions to industrial production. For example, the Great Britain is by 2,3 times behind of Russia – 1 301 billion USD versus 556 billion USD respectively. Once the largest global empire will lose economic and political significance after Brexit.

Picture 1. Top-20 of countries in terms of industrial production volume for 2017, billion USD

Picture 1. Top-20 of countries in terms of industrial production volume for 2017, billion USDSumming up

- China strengthens its status of “the world’s factory”. However, the increasing salaries and ageing of the population could lead to reverse process – corporations will transfer operations to the countries with low-paid work force (India, for instance).

- Due to availability of natural resources and highly developed sectors of heavy industry and fuel and energy complex, the Russia’s contribution to the global division of labor is significant and stable in the long view.

- Occident is losing momentum as the leading industrial countries.