Order a report

Custom-made industry research, company ratings, competitor analysis

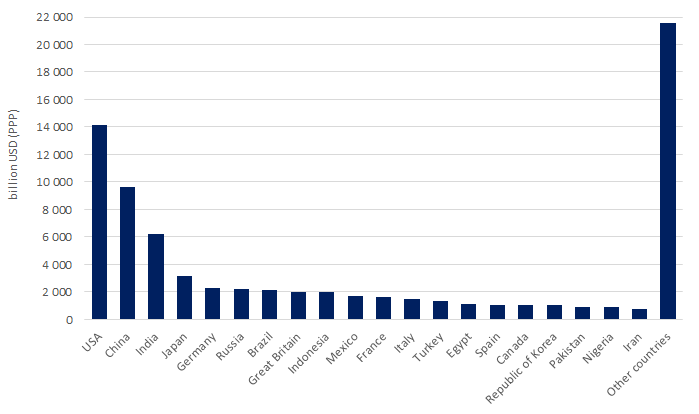

Top-20 of countries by consumer market volume

The consumer market is formed by purchasing power. The higher the purchasing power and economic well-being of the population, the more it spends. The more people spend, the more attractive the country is as a market for producers. The scale of the consumer market significantly defines the political weight and importance of the State in global trade.

One of the main criteria for assessing the attractiveness and potential of the consumer market for the international investors is the total amount of personal expenses of the population on goods, services, material goods, in other words – the final consumption of the private households.

In Top-20 ranking by the sum of personal expenses on goods and services, Russia takes the sixth place. In 2018 the local households spent 2 191 billion USD on goods and services.

The consumption in Russia has features that affect on the total amount. In particular, a significant proportion of natural self-sufficiency. This may include self-repair and maintenance of residential premises, as well as the consumption of goods obtained from own subsidiary husbandry. Statistics does not take into account such purchases.

The first three places in Top-20 take USA, China and India.

According to the 2018 results, the U.S. population spent 14 141 billion USD on goods and services, that is 18.1% of the expenditure of residents around the world (Table 1).

Despite the fact that China is 4.3 times ahead of USA in terms of population, the consumer market of China is estimated at a smaller amount of 9 603 billion USD.

India takes the third place with the sum of 6 198 billion USD.

| № | Country | Expenditure, billion USD | Share in global expenditure, % |

| All countries | 78 289 | 100,0 | |

| Top-20 | 56 759 | 72,5 | |

| 1 | USA | 14 141 | 18,1 |

| 2 | China | 9 603 | 12,3 |

| 3 | India | 6 198 | 7,9 |

| 4 | Japan | 3 133 | 4,0 |

| 5 | Germany | 2 309 | 2,9 |

| 6 | Russia | 2 191 | 2,8 |

| 7 | Brazil | 2 120 | 2,7 |

| 8 | Great Britain | 2 005 | 2,6 |

| 9 | Indonesia | 1 992 | 2,5 |

| 10 | Mexico | 1 696 | 2,2 |

| 11 | France | 1 600 | 2,0 |

| 12 | Italy | 1 462 | 1,9 |

| 13 | Turkey | 1 353 | 1,7 |

| 14 | Egypt | 1 141 | 1,5 |

| 15 | Spain | 1 081 | 1,4 |

| 16 | Canada | 1 065 | 1,4 |

| 17 | Republic of Korea | 1 025 | 1,3 |

| 18 | Pakistan | 936 | 1,2 |

| 19 | Nigeria | 935 | 1,2 |

| 20 | Iran | 773 | 1,0 |

Participants of Top-20 list accumulate 56 759 billion USD or 72.5% of all public expenditure on goods and services. The share of other countries is only 19 530 billion USD or 27,5% of global consumer market (Picture 1).

Picture 1. Top-20 of countries by expenditure on goods and services in 2018, billion USD

Picture 1. Top-20 of countries by expenditure on goods and services in 2018, billion USD