Every year, the Russian business faces new challenges and opportunities, forming plans and strategies under the constantly changing economic and political conditions. 2024 will be no exception.

A number of significant changes to the Russian legislation are expected to come into force. The dynamics of global sanctions will continue to intensify, getting new instruments of restrictions. The importance of analyzing possible risks in international interaction will increase significantly, requiring a deeper understanding of the variability of the international scene and business flexibility during the economic transformation.

The moratorium on inspections has been extended again

The regime for canceling scheduled business inspections has been extended until 2024 (Resolution of the Government of the Russian Federation dated December 14, 2023 No. 2140). This rule applies to organizations of the moderate, medium and significant risk categories, but does not cover tax audits that will be conducted in accordance with the established plan.

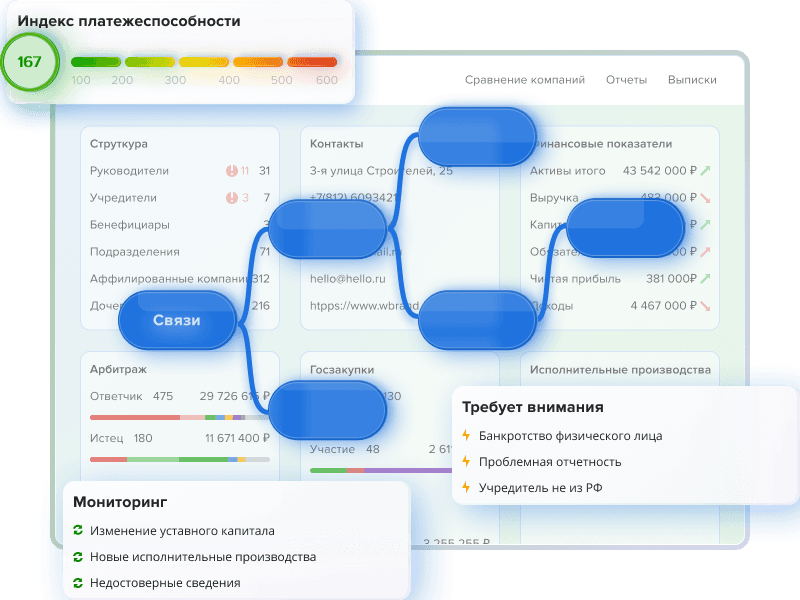

Information on the results of inspections can show how well the company fulfills certain requirements when carrying out business activities. The results of the audits provide information about the extent to which the company complies with the requirements in carrying out its activities. Analysis of the results of both scheduled and unscheduled inspections, as well as carrying out preventive measures, can be conducted in Globas. Globas will automatically displays relevant information if violations are detected or warnings are issued based on the results of the inspection.

New income limits for the simplified tax system

In accordance with the order of the Ministry of Economic Development dated October 23, 2023 No. 730, legal entities and individual entrepreneurs will be able to switch to the Simplified Tax System in 2024, provided that their income for the nine months of 2023 is less than 149,5 million rubles. Companies and individual entrepreneurs will not be able to use the simplified tax system in 2024 if their income since the beginning of the year is over 265,8 million rubles.

In Globas you can analyze detailed information about taxes and fees of your counterparty, track the application of special tax regimes and the dynamics of the tax burden from year to year, as well as the financial condition and stability of your partner.

New deadlines for publishing open data from the Federal Tax Service

Starting from December 25, 2023, information on arrears in paying taxes, fees and insurance premiums will be posted on the Federal Tax Service website not monthly, but quarterly - on the 25th day of every third month in a quarter.

Information about the name of the taxpayer and the amount of the debt will be indicated as of the 10th day of February, April, August and October. Currently, the information is for the 1st day of the month of publication.

As open data from the Federal Tax Service is published, it will be duly added to Globas, so that you do not miss critically important information and always know whether the counterparty is fulfilling its tax obligations.

Fines for violating the law on foreign agents

In accordance with the Federal Law No. 364-FZ dated July 24, 2023, penalties have been introduced for failure to comply with the legislation on foreign agents. The law provides for liability for failure to comply with orders or warnings from the state control authority regarding compliance with legislation on foreign agents and for failure to eliminate identified violations within the period established by law. Persons who have committed a violation are subject to a fine of 30-50 thousand rubles. Officials may be fined 70-100 thousand rubles or disqualified for two years. Legal entities may face a fine of 200-300 thousand rubles.

You can check your counterparty and persons associated with it for inclusion in the List of Foreign agents, as well as Lists of those excluded from foreign agents and persons associated with foreign agents using Globas and Sanctions Compliance module.

Sanctions of Russia

Russia has created a legislative toolkit for introducing blocking sanctions. The President of Russia signed the Federal Law "On Amendments to Certain Legislative Acts of the Russian Federation" No. 422-FZ dated 04.08.2023. The document comes into force since February 1, 2024.

Key provisions:

1. Liability measures have been established for the Russian legal entities in the banking sector, in the field of insurance, brokerage services, etc., for failure to comply with the Russian special economic measures.

2. Administrative measures to comply with the special economic measures are carried out by the Bank of Russia, including orders, restrictions on activities for up to six months, and a fine of up to 5 million rubles.

3. The concept of a “blocked person” has been introduced, which may include a foreign state, organization, foreign citizen, stateless person, as well as legal entities controlled by foreign organizations, citizens, stateless persons.

4. The “50% Rule” has been established to determine the controllers of a legal entity.

5. The rights of blocked persons are determined, including the possibility of receiving a salary (not exceeding 10 thousand rubles per month) or payment for medical services (not exceeding 10 thousand rubles per month).

To analyze the existence of sanctions risks according to global lists of sanctions, including the list of special economic measures of Russia, you can use the Sanctions Compliance as an additional module to Globas subscription.

Globas

Sanctions Compliance

Module for in-depth sanctions screening. While checking, over 40 new criteria are used. Sanctions Compliance makes it possible to check Russian and foreign counterparties, persons, water and air transport. Related entities are also checked: beneficial owners, shareholders, management, affiliated and subsidiary companies. The functionality of the module contains extensive information about the imposed sanctions and restrictions, including those under the 50% Rule, additional sources and deeper analytics on companies, persons and objects under restrictions and included in various risk registers.