Order a report

Custom-made industry research, company ratings, competitor analysis

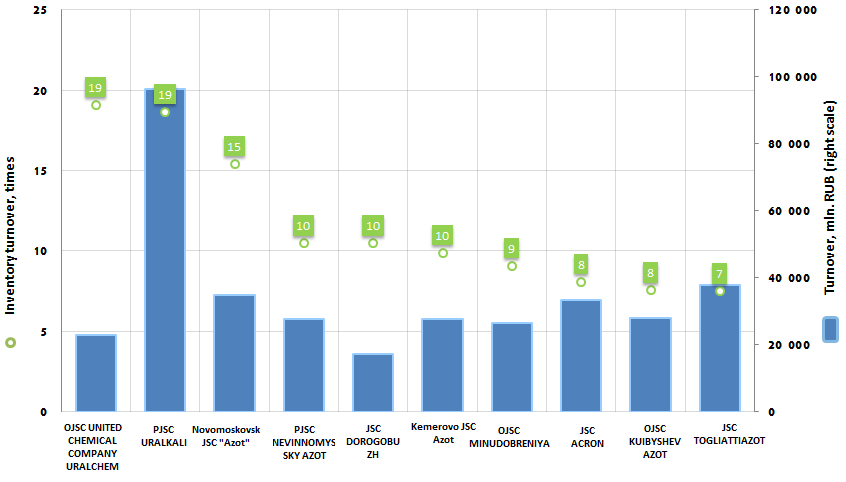

Inventory turnover of the largest Russian enterprises, engaged in manufacture of fertilizers

Information Agency Credinform has prepared the ranking of the companies, engaged in manufacture and supply of fertilizers.

The largest enterprises in terms of revenue were selected according to the data from the Statistical Register for the latest available period (for the year 2013). Then, the companies were ranged by decrease in rate of inventory turnover.

Inventory turnover (times) is a ratio of revenue and average stock value for a period. It shows the efficiency of inventories sales. The higher is the rate, the faster are the production cycle and sale of goods.

Low inventory turnover ratio is the poor indicator of financial and economic activity of the company, it reflects the surplus stocks and (or) poor sales, demand for products; the result is overstocking.

In contrast, the high inventory turnover ratio reflects the mobility of company's funds: the faster is the stock rotation, the faster is the money turnover, invested in stocks, and the return in the form of revenue from sales of finished products; the higher is the inventory turnover - the better for the company. Low stocks are forcing the company to balance on the brink of deficit, that is inevitably lead to losses of customers and unreasonably high expenses on rapid replenishment of stocks: the company has to bring enough goods.

Thus, the optimality of reserves is mandatory for company’s business activities, and inventory turnover is the indicator, which must be constantly updated.

For the most full and fair opinion about the company’s financial statement, not only the average revenue values should be taken into account, but also the whole set of financial indicators and ratios.

| № | Name | Region | Revenue, mln. RUB, 2013 | Inventory turnover, times | Solvency index GLOBAS-i ® |

|---|---|---|---|---|---|

| 1 | OJSC UNITED CHEMICAL COMPANY URALCHEM INN 7703647595 |

Moscow | 22 783,0 | 19 | 297 high |

| 2 | PJSC URALKALI INN 5911029807 |

Perm region | 96 308,9 | 19 | 191 the highest |

| 3 | Novomoskovsk JSC "Azot" INN 7116000066 |

Tula region | 34 966,0 | 15 | 176 the highest |

| 4 | PJSC NEVINNOMYSSKY AZOT INN 2631015563 |

Stavropol region | 27 770,2 | 10 | 205 high |

| 5 | JSC DOROGOBUZH INN 6704000505 |

Smolensk region | 17 359,6 | 10 | 148 the highest |

| 6 | Kemerovo JSC Azot INN 4205000908 |

Kemerovo region | 27 802,0 | 10 | 208 high |

| 7 | OJSC MINUDOBRENIYA INN 3627000397 |

Voronezh region | 26 585,4 | 9 | 197 the highest |

| 8 | JSC ACRON INN 5321029508 |

Novgorod region | 33 420,5 | 8 | 284 high |

| 9 | OJSC KUIBYSHEVAZOT INN 6320005915 |

Samara region | 28 045,1 | 8 | 180 the highest |

| 10 | JSC TOGLIATTIAZOT INN 6320004728 |

Samara region | 37 716,1 | 7 | 152 the highest |