Order a report

Custom-made industry research, company ratings, competitor analysis

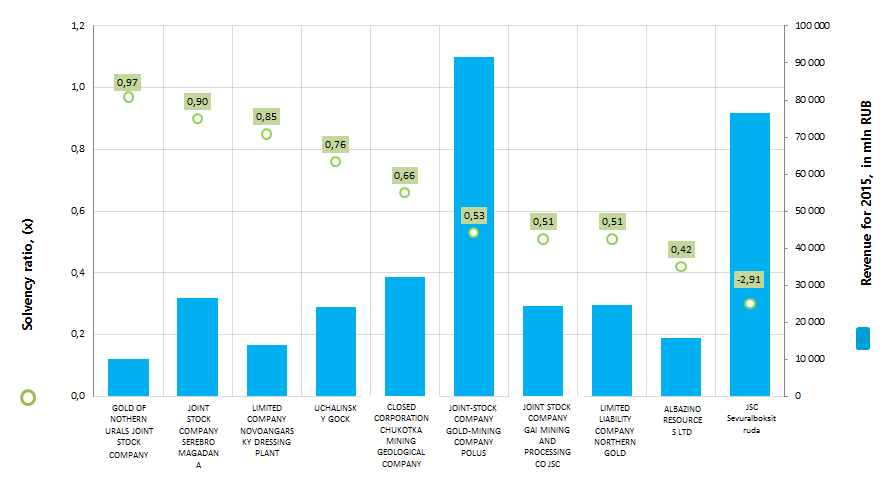

Solvency ratio of the largest Russian enterprises, mining precious and non-ferrous metal ores

Information agency Credinform prepared a ranking of the largest Russian enterprises, mining precious and non-ferrous metal ores.

The enterprises, mining precious and non-ferrous metal ores, with the highest volume of revenue (TOP-10) were selected for the ranking, according to the data from the Statistical Register for the latest available accounting period (for the year 2015). Then the companies were ranked by decrease in solvency ratio (Table 1).

Solvency ratio (х) is calculated as a relation of equity capital to total assets and characterizes the company's dependence on external loans. Recommended value of the ratio is: > 0,5.

The ratio value below the minimum recommended limit means a high dependence on external sources of financing. By the worsening of conjecture in the market it may lead to liquidity crisis and to unstable financial position.

For getting of the most comprehensive and fair picture of the financial standing of an enterprise it is necessary to pay attention to all available combination of ratios, financial and other indicators.

| Name, INN, region | Net profit for 2015, in mln RUB | Revenue for 2015, in mln RUB | Revenue for 2015 by 2014, % | Solvency ratio, (х) | Solvency index Globas-i |

|---|---|---|---|---|---|

| GOLD OF NOTHERN URALS JOINT STOCK COMPANY INN 6617001534 Sverdlovsk region |

5 660,0 | 10 140,6 | 90 | 0,97 | 208 High |

| JOINT STOCK COMPANY SEREBRO MAGADANA INN 4900003918 Magadan region |

11 294,4 | 26 627,8 | 142 | 0,90 | 219 High |

| LIMITED COMPANY NOVOANGARSKY DRESSING PLANT INN 2426003607 Krasnoyarsk territory |

5 250,6 | 13 906,6 | 112 | 0,85 | 162 The highest |

| UCHALINSKY GOCK INN 0270007455 Republic of Bashkortostan |

3 300,7 | 24 151,9 | 127 | 0,76 | 204 High |

| CLOSED CORPORATION CHUKOTKA MINING GEOLOGICAL COMPANY INN 8709009294 Chukotka Autonomous Region |

10 214,7 | 32 335,5 | 87 | 0,66 | 189 The highest |

| JOINT-STOCK COMPANY GOLD-MINING COMPANY POLUS INN 2434000335 Krasnoyarsk territory |

37 827,5 | 91 691,6 | 152 | 0,53 | 183 The highest |

| JOINT STOCK COMPANY GAI MINING AND PROCESSING CO JSC INN 5604000700 Orenburg region |

2 185,1 | 24 511,0 | 141 | 0,51 | 228 High |

| LIMITED LIABILITY COMPANY NORTHERN GOLD INN 8706005044 Chukotka Autonomous Region |

11 227,1 | 24 707,0 | 191 | 0,51 | 246 High |

| ALBAZINO RESOURCES LTD INN 2721128498 Khabarovsk territory |

4 163,4 | 15 724,1 | 136 | 0,42 | 247 High |

| JSC Sevuralboksitruda INN 6631001159 Sverdlovsk region |

5 618,0 | 76 472,8 | 200 | 0,30 | 263 High |

The average value of the solvency ratio in the group of TOP-10 largest enterprises, mining precious and non-ferrous metal ores, was 0,64 in 2015 against 0,60 in 2014. The same index in the group of TOP-100 companies made 0,42 in 2014, by industry average value of 0,48.

Recline in solvency ratio in 2015 compared with the previous year is observed by UCHALINSKY GOCK, JOINT-STOCK COMPANY GOLD-MINING COMPANY POLUS and JOINT STOCK COMPANY GAI MINING AND PROCESSING CO JSC.

ALBAZINO RESOURCES LTD and JSC Sevuralboksitruda did not meet the recommended standard of the ratio as well in 2014 as in 2015. By this the second company showed the maximum growth in revenue in 2015 in regard to 2014 in the group of TOP-10 companies. The decrease in revenue for this period was by GOLD OF NOTHERN URALS JOINT STOCK COMPANY and CLOSED CORPORATION CHUKOTKA MINING GEOLOGICAL COMPANY.

Though, on the combination of financial and non-financial indicators, all enterprises got the highest or high solvency index Globas-i, that indicates their ability to repay their debts in time and fully.

The total revenue of the TOP-10 companies reached 340,3 billion rubles in 2015, that is by 42% more than in 2014. At the same time the total net income in 2014 and in 2015 increased more than twice in relation to the corresponding previous periods.

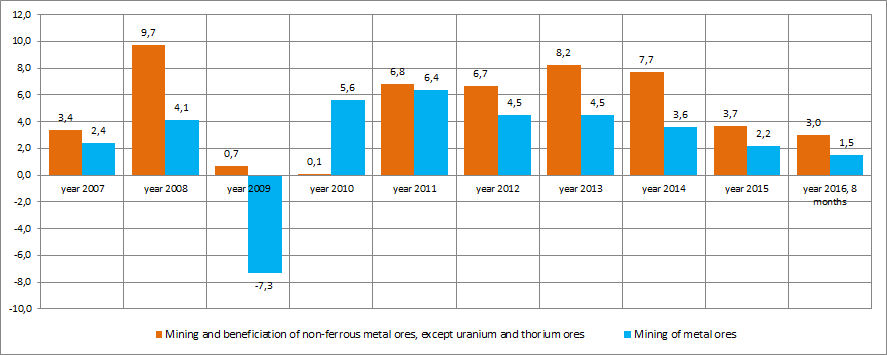

In general, the enterprises of TOP-10 and TOP-100 groups demonstrate a high enough independence on external sources of funds. However, the discernible trend to a decrease in the level of production is observed in this industry recently. This is as evidenced by the data of the Federal State Statistics Service (Rosstat) (Picture 2).

The enterprises, mining precious and non-ferrous metal ores, are distributed across country's regions unequal and biased to the corresponding mineral fields. Thus, according to the data of the Information and analytical system Globas-i, 100 the largest companies on the volume of revenue for 2014 are registered in 22 regions. The greatest number of them is registered in the regions shown in Table 2.

| Region | Number of companies |

|---|---|

| Republic of Sakha (Yakutia) | 13 |

| Magadan region | 11 |

| Irkutsk region | 10 |

| Krasnoyarsk territory | 9 |

| Khabarovsk territory | 8 |

| Chukotka Autonomous Region | 7 |

| Amur region | 6 |

| Sverdlovsk Region | 6 |

| Kamchatka territory | 4 |

| Republic of Bashkortostan | 4 |

Thus, 78% of the largest companies of this industry are concentrated in 10 regions of the country.