Order a report

Custom-made industry research, company ratings, competitor analysis

Redomicilation to Russia

The law on termination of the double tax treaty between Russia and the Netherlands was signed on May 26, 2021 due to the refusal of the Netherlands government to rise tax rate to 15% for dividends and interest transferred from the Russian subsidiaries to foreign accounts. The treaty will be no longer in force from January 1, 2022, if the notice of denunciation is sent before the end of June 2021.

Cyprus, Malta and Luxembourg have agreed to change the doubly tax treaty on such conditions as Russia established.

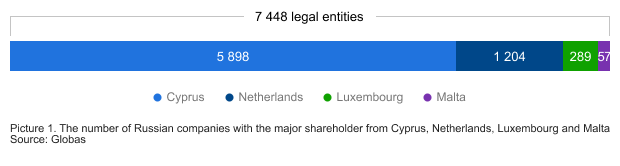

Russian companies controlled by the foreign residents

The residents of four countries, the treaty is revised with, control 7 448 Russian legal entities including 337 the largest taxpayers with the annual revenue exceeding 10 billion RUB.

The Cyprus residents control 5 898 companies including 218 the largest taxpayers, and 1 204 entities with 104 the largest taxpayers count for the Netherlands.

Consequences of termination of the double tax treaty with the Netherlands

The double tax treaty with the Netherlands made it possible to withdraw profit from Russia in the form of dividends at the 5% rate, and interest on debenture at the 0% rate. In 2019, 339,9 billion RUB were transferred to the Netherlands in this way. According to the Central bank of Russia, the volume of foreign direct investment in the reinvestment of income from the Netherlands to Russia amounted to 118,6 billion RUB, i.e. 2,9 times less than the withdrawn capital.

Now the rate will be risen to 15% for dividends and to 20% for interest. If a legal entity operates without a permanent establishment, it will be obliged to pay the income tax in two jurisdictions. Moreover, such kind of companies cannot count on the reduction of rates in Netherlands at the distribution of interest and dividends in Russia. Taxes paid in the Netherlands will not be counted for individuals either.

It will be a milestone for the Russian business: it is head for the foreign corporations obtaining profit in Russia to pay taxes at the full rates especially in light of the fact that many of them are of the Russian origin.

The largest taxpayers controlled by the Dutch legal entities:

JSC VIMPEL-COMMUNICATIONS, JSC AVTOVAZ, LLC YANDEX,

JSC FORTUM, LLC CORPORATE CENTER X 5,

JSC TRANSMASHHOLDING, LLC URAL LOCOMOTIVES

Consequences of changes of the double tax treaty with Cyprus

Formally not considered as an offshore zone, Cyprus with its very loyal tax legislation was the most attractive country for large companies of the Russian origin until recently. Over 1,9 trillion RUB were transferred to Cyprus in 2019, while the foreign direct investment in the reinvestment of income from Cyprus to Russia were 3,7 times less and amounted to 512 billion RUB.

A new treaty with Cyprus is already in force since January 1, 2021. The tax rate for dividends was increased form 5% to 15% and for interest – from 0% to 15%. After applied changes, there is the first case of redomicilation. On March 2021, LENTA INTERNATIONAL PUBLIC JOINT-STOCK COMPANY was redomiciled from Cyprus to the special administrative region in Kaliningrad, the major shareholder of LLC LENTA-2, owner of Lenta hypermarket chain.

Special administrative regions or SAR are regions with preferential tax regime located in the islands Russky (Vladivostok) and Oktyabrsky (Kaliningrad). The main purpose of SAR establishment is the repatriation of capital and protection of legal entities from sanctions.

The largest taxpayers controlled by the Cyprus residents are engaged in the metallurgical industry:

JSC NOVOLIPETSK STEEL MILL, JSC MAGNITOGORSK IRON & STEEL WORKS,

JSC PIPE METALLURGICAL COMPANY

Harbors for the Russian business

The Ministry of Finance of Russia plans to start negotiations with Singapore, Switzerland and Hong Kong for changes in double tax treaty. The possible strategy for the holding companies is to have no foreign residents as shareholders, which will lead to reorganization of their corporate structure. Special administrative regions in Vladivostok and Kaliningrad may provide an alternative where there is a 5% tax rate for dividends for public international holding companies (“public IHC”). Moreover, there is a bill on application of this regime for non-public IHC.

The following shareholders of large corporations were established in SAR:

LENTA INTERNATIONAL PUBLIC JOINT-STOCK COMPANY,

OK RUSAL INTERNATIONAL PUBLIC JOINT-STOCK COMPANY,

EN+ GROUP INTERNATIONAL PUBLIC JOINT-STOCK COMPANY,

ROSENERGO INVESTMENTS INTERNATIONAL PUBLIC JOINT-STOCK COMPANY,

INTERNATIONAL COMPANY AKTIVUM shareholder of JSC MMC NORILSK NICKEL)

The creation of special administrative regions is the transfer of international practices of offshore administration to Russia. In the future, this will make it possible not only to re-domicile Russian companies, but also to attract foreign ones. Subject to the revision of the treaties under the terms of Russia, the rate on dividends and interest in foreign jurisdictions will be increased to 15%, and it will be 0-5% in domestic offshores.