Order a report

Custom-made industry research, company ratings, competitor analysis

Equity funds in automotive manufacture

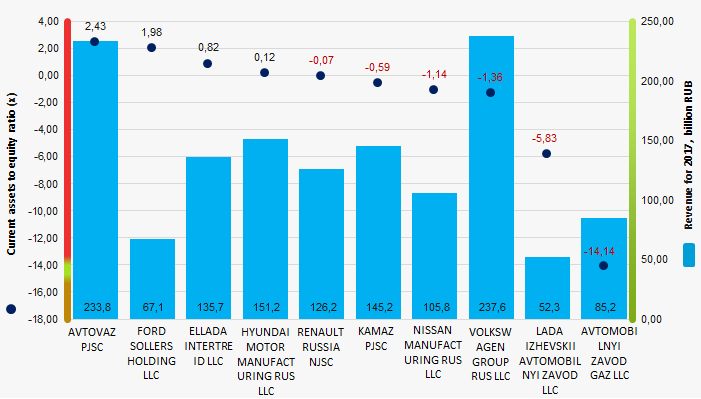

Information agency Credinform represents the ranking of the largest Russian automotive companies. The automobile manufacturers with the largest volume of annual revenue (TOP-10) were selected for the ranking, according to the data from the Statistical Register for the latest available periods (for 2015 - 2017). Then they were ranked by current assets to equity ratio (Table 1). The analysis was made on the basis of the data of the Information and Analytical system Globas.

Current assets to equity ratio (х) characterizes company’s ability to maintain the level of own working capital and to finance current assets with own sources. The ratio is calculated as the relation of own current assets of a company to total value of equity. The recommended value is in the range from 0,2 up to 0,5.

Decrease in the ratio indicates a possible slowdown in payment of receivables or tightening of conditions for granting trade credit from suppliers and contractors. The increase points to the growing opportunity to pay off current liabilities.

The experts of the Information agency Credinform, taking into account the actual situation both in the economy as a whole and in the sectors, has developed and implemented in the Information and Analytical system Globas the calculation of practical values of financial ratios that can be recognized as normal for a particular industry. For automobile manufacturers the industry average practical value of the current assets to equity ratio made from 0,41 up to 1,00 in 2017.

For getting of the most comprehensive and fair picture of the financial standing of an enterprise it is necessary to pay attention to all combination of indicators and financial ratios.

| Name, INN, region, type of activity | Revenue, billion RUB | Net profit (loss), billion RUB | Current assets to equity ratio (x), from 0,2 up to 0,5 | Solvency index Globas | |||

| 2016 | 2017 | 2016 | 2017 | 2016 | 2017 | ||

| 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 |

| AVTOVAZ PJSC INN 6320002223 Samara region Car production |

|

|

|

|

|

|

267 Medium |

| FORD SOLLERS HOLDING LLC INN 1646021952 Republic of Tatarstan Manufacture of motor vehicles |

|

|

|

|

|

|

311 Adequate |

| ELLADA INTERTREID LLC INN 3906072056 Kaliningrad region Manufacture of motor vehicles |

|

|

|

|

|

|

207 Strong |

| HYUNDAI MOTOR MANUFACTURING RUS LLC INN 7801463902 St. Petersburg Manufacture of motor vehicles |

|

|

|

|

|

|

209 Strong |

| RENAULT RUSSIA NJSC INN 7709259743 Moscow Manufacture of motor vehicles |

|

|

|

|

|

|

219 Strong |

| KAMAZ PJSC INN 1650032058 Republic of Tatarstan Truck production |

|

|

|

|

|

|

192 High |

| NISSAN MANUFACTURING RUS LLC INN 7842337791 St. Petersburg Manufacture of motor vehicles |

|

|

|

|

|

|

284 Medium |

| VOLKSWAGEN GROUP RUS LLC INN 5042059767 Kaluga region Manufacture of motor vehicles |

|

|

|

|

|

|

237 Medium |

| LADA IZHEVSKII AVTOMOBILNYI ZAVOD LLC INN 1834051678 Udmurtian Republic Manufacture of motor vehicles |

|

|

|

|

|

|

324 Adequate |

| AVTOMOBILNYI ZAVOD GAZ LLC INN 5250018433 Nizhny Novgorod region Manufacture of internal combustion engines of motor vehicles |

|

|

|

|

|

|

219 Medium |

| Total by TOP-10 companies | |

|

|

|

|||

| Avearge value by TOP-10 companies | |

|

|

|

|

|

|

| Industry average value | |

|

|

|

|

|

|

![]() — improvement of the indicator to the previous period,

— improvement of the indicator to the previous period, ![]() — decline in the indicator to the previous period.

— decline in the indicator to the previous period.

The average value of the current assets to equity ratio of TOP-10 enterprises is above industry average, but below recommended and practical values. Four companies from the TOP-10 list improved the indicators in 2017 compared to the previous period.

Picture 1. Current assets to equity ratio and revenue of the largest Russian automotive companies (TOP-10)

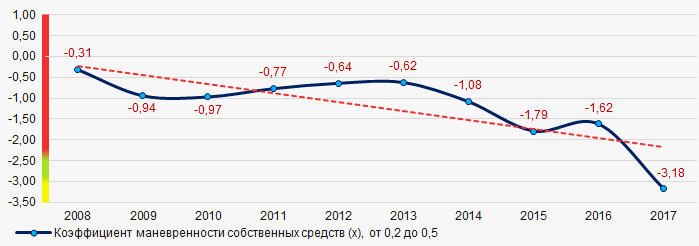

Picture 1. Current assets to equity ratio and revenue of the largest Russian automotive companies (TOP-10)The industry average indicators of the current assets to equity ratio have a downward trend over the course of 10 years (Picture 2).

Picture 2. Change in the industry average values of the current assets to equity ratio of Russian automotive companies in 2008 – 2017

Picture 2. Change in the industry average values of the current assets to equity ratio of Russian automotive companies in 2008 – 2017