Order a report

Custom-made industry research, company ratings, competitor analysis

TOP 10 road construction companies in Moscow

Information agency Credinform represents a ranking of the largest Russian road construction companies in Moscow. Companies with the largest volume of annual revenue (TOP 10 and TOP 50) were selected for the ranking, according to the data from the Statistical Register and the Federal Tax Service for the latest available periods (2018 - 2020). They were ranked by the return on the authorized capital (Table 1). The selection and analysis were based on the data of the Information and Analytical system Globas.

Return on the authorized capital (%) indicates the efficiency of the authorized capital use and shows the amount of net profit accounting for one rouble of the authorized capital.

The higher is the indicator, the more efficient is the usage of capital contributed to the authorized fund. However, it is necessary to consider that too high values, exceeding in several times the average values for economy or sector may indicate low authorized capital at higher net profit.

For the most complete and objective view of the financial condition of the enterprise, it is necessary to pay attention to the complex of indicators and financial ratios of the company.

| Name, INN | Revenue, billion RUB | Net profit (loss), billion RUB | Return on the authorized capital, % | Solvency index Globas | |||

| 2019 | 2020 | 2019 | 2020 | 2019 | 2020 | ||

| 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 |

| JSC DSK AVTOBAN INN 7725104641 |

|

|

|

|

|

|

208 Strong |

| LLC CONCESSION CONSTRUCTION COMPANY No. 1 INN 9729021990 |

|

|

|

|

|

|

264 Medium |

| JSC FOR CONSTRUCTION AND RECONSTRUCTION OF ROADS AND AERODROMES INN 6163002069 |

|

|

|

|

|

|

195 High |

| LLC DORTEKH INN 7728346960 |

|

|

|

|

|

|

222 Strong |

| JSC TSENTRDORSTROI INN 7702059544 |

|

|

|

|

|

|

205 Strong |

| LLC KOLTSEVAYA MAGISTRAL INN 5032273017 |

|

|

|

|

|

|

295 Medium |

| LLC IBT INN 7704818388 |

|

|

|

|

|

|

228 Strong |

| LLC RUS-STROI INN 7707766346 |

|

|

|

|

|

|

239 Strong |

| JSC MOSTOTREST INN 7701045732 |

|

|

|

|

|

|

297 Medium |

| LLC TRANSSTROIMEKHANIZATSIYA INN 7715568411 |

|

|

|

|

|

|

299 Medium |

| Average value for TOP 10 | |

|

|

|

|

|

|

| Average value for TOP 50 | |

|

|

|

|

|

|

| Average industry value | |

|

|

|

|

||

![]() growth of indicator to the previous period,

growth of indicator to the previous period, ![]() fall of indicator to the previous period

fall of indicator to the previous period

The industry average values of the return on the authorized capital is significantly above the industry average ones of TOP 10 and TOP 50. Two companies of TOP 10 had negative values of the indicator and reduced their figures in 2020. In 2019, the fall was recorded for five companies.

In 2020, seven companies included in TOP 10 gained revenue and five legal entities gained net profit. In general, the revenue of TOP 10 climbed at average 2%, and a 3% decrease was recorded in TOP 50. There was a 5% increase in the industry average indicator.

There was a 5% and 41% decrease in profit of TOP 10 and TOP 50 respectively. The industry average profit climbed 3 times.

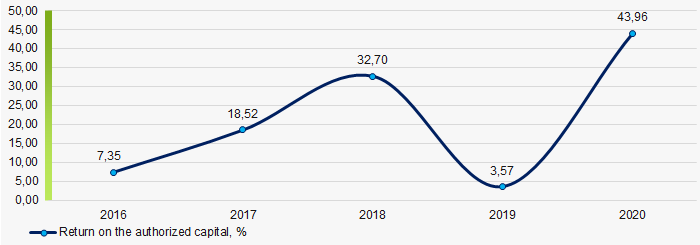

Over the past five years, the industry average values of the return on the authorized capital have increased over three periods. The highest value was recorded in 2020 and the lowest one was in 2019 (Picture 1).

Picture 1. Change in the industry average values of the return on the authorized capital in 2016 - 2020

Picture 1. Change in the industry average values of the return on the authorized capital in 2016 - 2020