Order a report

Custom-made industry research, company ratings, competitor analysis

Profitability of services of the largest Russian recruitment agencies

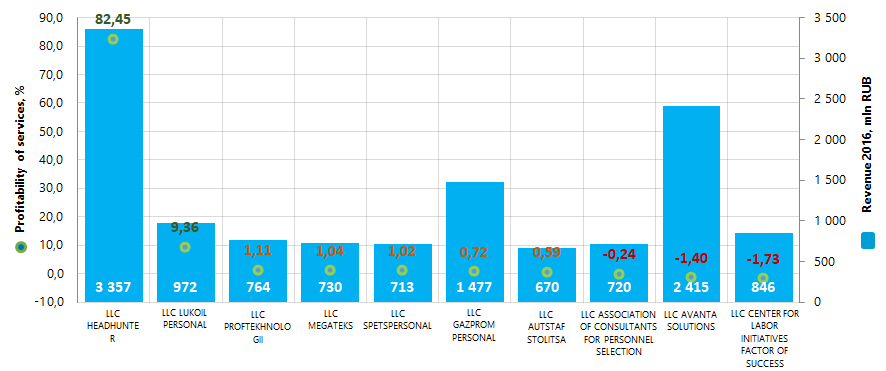

Information agency Credinform prepared a ranking of profitability of services of the largest Russian recruitment agencies. Companies with the highest volume of revenue (TOP-10) were selected for this ranking according to the data from the Statistical Register for the latest available periods (2016 and 2015). The enterprises were ranked by decrease in profitability of services (Table 1). The analysis was based on data from the Information and Analytical system Globas.

Profitability of services or goods (%) is sales profit to expenses from ordinary activities. Profitability in general indicates production efficiency. The analyses of profitability of services allows to conclude about expediency of one or another kind of services. There is no standard value for profitability indicators, because they change in accordance with the industry the company operates in.

Taking into account the actual situation both in economy in general and in the sector, the experts of the Information agency Credinform have developed and implemented in the Information and Analytical system Globas the calculation of practical values of financial ratios, which can be recognized as normal for a particular industry. The practical value for companies engaged in recruitment in 2016 is from 2,29%.

For the most complete and objective view of the financial condition of the enterprise it is necessary to pay attention to the complex indicators and financial ratios of the company.

| Name, INN, region | Revenue, mln RUB | Net profit, mln RUB | Profitability of services, % | Solvency index Globas | |||

| 2015 | 2016 | 2015 | 2016 | 2015 | 2016 | ||

| 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 |

| LLC HEADHUNTER INN 7718620740 Moscow |

2 696,2 | 3 357,4 | 1 142,9 | 1 349,3 | 95,45 | 82,45 | 205 Strong |

| LLC LUKOIL PERSONAL INN 7707320456 Moscow |

748,3 | 972,1 | 12,2 | 51,3 | 1,22 | 9,36 | 168 Superior |

| LLC PROFTEKHNOLOGII INN 4027107319 Moscow |

723,3 | 763,8 | 7,4 | 2,6 | 1,49 | 1,11 | 273 Medium |

| LLC MEGATEKS INN 7807307628 Saint-Petersburg |

594,3 | 594,3 | 2,1 | 1,1 | 0,19 | 1,04 | 218 Strong |

| LLC SPETSPERSONAL INN 6685049037 Moscow |

749,6 | 713,4 | 9,9 | 1,1 | 1,76 | 1,02 | 292 Medium |

| LLC GAZPROM PERSONAL INN 7728794168 Moscow |

1 163,0 | 1 476,7 | 5,5 | -8,3 | -0,80 | 0,72 | 275 Medium |

| LLC AUTSTAF STOLITSA INN 7714743371 Moscow |

854,5 | 669,9 | 7,2 | 1,2 | 1,71 | 1,71 | 279 Medium |

| LLC Association of Consultants for Personnel Selection INN 7728700875 Moscow |

1,7 | 719,9 | 0,0 | 0,0 | -4,67 | -0,24 | 550 Insufficient |

| LLC AVANTA SOLUTIONS INN 7707309438 Moscow |

2 343,8 | 2 415,1 | -129,4 | -62,7 | -4,94 | -1,40 | 285 Medium |

| LLC CENTER FOR LABOR INITIATIVES FACTOR OF SUCCESS INN 7743794420 Moscow |

364,2 | 364,2 | 0,1 | 1,2 | -7,95 | -1,73 | 550 Insufficient |

| Total for TOP-10 | 10 239,0 | 12 664,7 | 1 057,8 | 1 336,9 | |||

| Average value for TOP-10 companies | 1 023,9 | 1 266,5 | 105,8 | 133,7 | 8,35 | 9,29 | |

| Average value for industry | 21,3 | 21,7 | 0,8 | 0,7 | 4,92 | 4,43 | |

Average value of profitability of services ratio for TOP-10 is above the practical and industry average. However only two companies in TOP-10 have values higher than practical in 2016, five – lower, and three companies have negative value (marked with green, orange and red in columns 6 and 7 of Table 1 and on Picture 1). Three companies in the top of the ranking have increased revenue and net profit figures in 2016 compared to the previous period. The rest of companies decreased revenue or net profit, or have losses (filled with red in columns 3 and 5 of Table 1).

Picture 1. Profitability of services ratio and revenue of the largest Russian recruitment agencies (TOP-10)

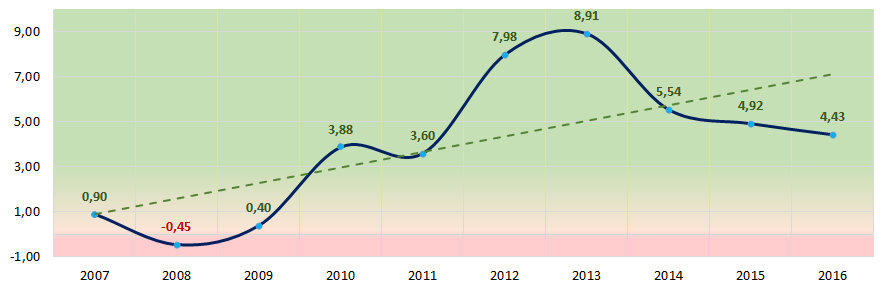

Picture 1. Profitability of services ratio and revenue of the largest Russian recruitment agencies (TOP-10)The average industry indicators of profitability of services ratio over the past 7 years were above practical value (Picture 2). This may indicates a relatively positive trend in in this field.

Picture 2. Change in average industry values of profitability of services ratio of the largest Russian recruitment agencies in 2007 – 2016

Picture 2. Change in average industry values of profitability of services ratio of the largest Russian recruitment agencies in 2007 – 2016Eight companies in TOP-10 got high, strong, medium and superior indexes Globas, that indicates their ability to timely and fully fulfill debt liabilities.

LLC ASSOCIATION OF CONSULTANTS FOR PERSONNEL SELECTION and CENTER FOR LABOR INITIATIVES FACTOR OF SUCCESS have got insufficient Solvency index Globas, due to negative signs peculiar to fly-by-night and unreliable companies. Index development forecast is negative.