Order a report

Custom-made industry research, company ratings, competitor analysis

Responsibility for errors in accounting increased

In April 2016 the Federal Law №77-FL as of 30.03.2016 "On Amendments to the Code of Administrative Offences of the Russian Federation" came into force.

Articles 4.5, 5.11, 29.9 and 81 of the Code of Administrative Offences (hereinafter – the Code) were amended. Administrative responsibility for repeated serious violation of requirements to accounting, including financial accounts, was implemented by the law.

The list of violations considered as serious was significantly extended. Now it includes also the following:

- registration in the accounting register of the fake business factor, as well as fake or pretended object for accounting;

- account management beyond accounting registers;

- preparation of financial statements based on the data not from the accounting registers;

- the absence of primary accounting documents, accounting registers and financial statement within the established document retention periods. This also applies to audit reports concerning financial statement in cases of mandatory audit.

Amounts of fines were also significantly increased. If earlier the fine for public individuals amounted to 2 – 3 thousand RUB, now it varies from 5 to 10 thousand RUB. Repeated offence will be fined at a rate from 10 to 20 thousand RUB or lead to disqualification from 1 to 2 years.

The limitation period for imposition of administrative sanctions for accounting law violation is increased to 2 years since the day of offence. The Code regulations on prolongation of the limitation period are applied to violations committed on or after April 10, 2016, and also on continuing violations disclosed since the mentioned date. Previously the limitation period was one year, because disregard of accounting maintenance rules was considered as violation of fiscal legislation. According to the current legislation, in case of expiry the limitation periods the administrative proceedings cannot be commenced and the already commenced proceeding has to be terminated.

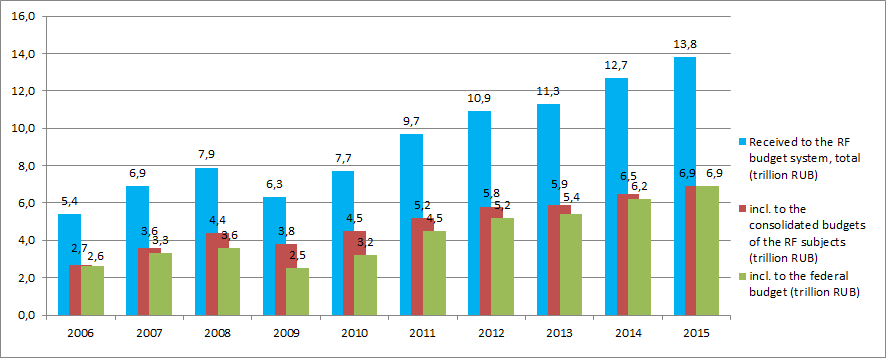

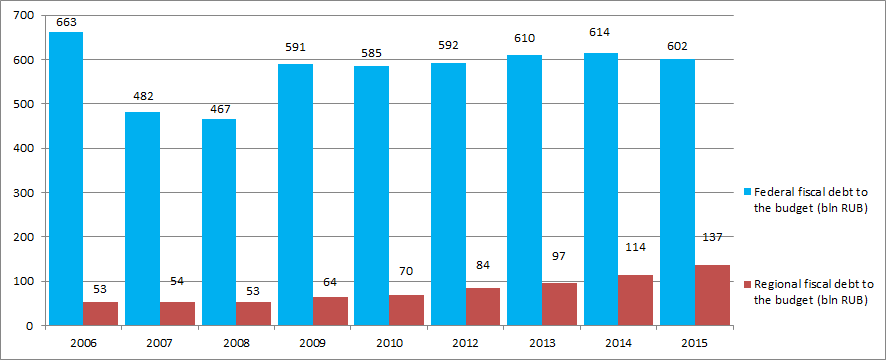

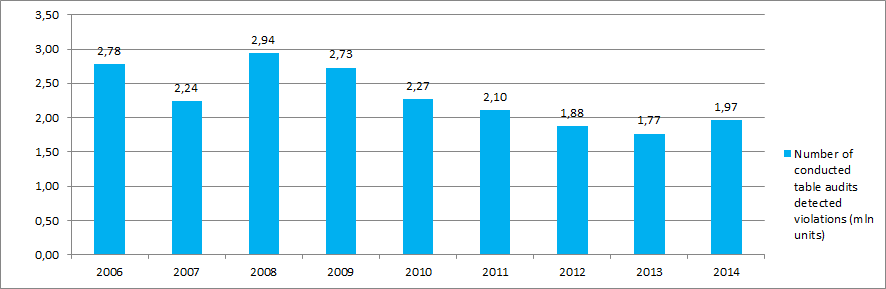

The necessity of measures on harsher the punishment for accounting violations is clear at comparing the data of the Federal tax service on collection of taxes, fees and other mandatory payments, fiscal, penalties and tax sanctions debts to the budget system and on the number of violations detected during the desk audits (Pictures 1, 2, 3).

Picture 1. Assessment and payment of taxes, duties and other mandatory payments to the budget of the Russian Federation

The analyses indicates that the fiscal revenues distribution structure changes with more than one and a half increase of revenues to the budget of Russia for 10 years in general. The share of regional budgets revenues decreased by no 2015 9% in comparison with 2010 is reducing.

Picture 2. Fiscal, penalties and tax sanctions debts to the budget system of the Russian Federation

At the same time, the increase of the fiscal debt to the federal budget by 3% in comparison with 2010 is observed, as well as the debt to the regional budget is increased by 95% for the same period.

Picture 3. Number of conducted desk audits detected violations – total for the Russian Federation

Moreover, there is a discernible trend of tax legislation violations typical for difficult economic conditions, as it was in 2008. The number of violations still remains high. Nearly every second taxpayer has violations detected during the table audits.