Order a report

Custom-made industry research, company ratings, competitor analysis

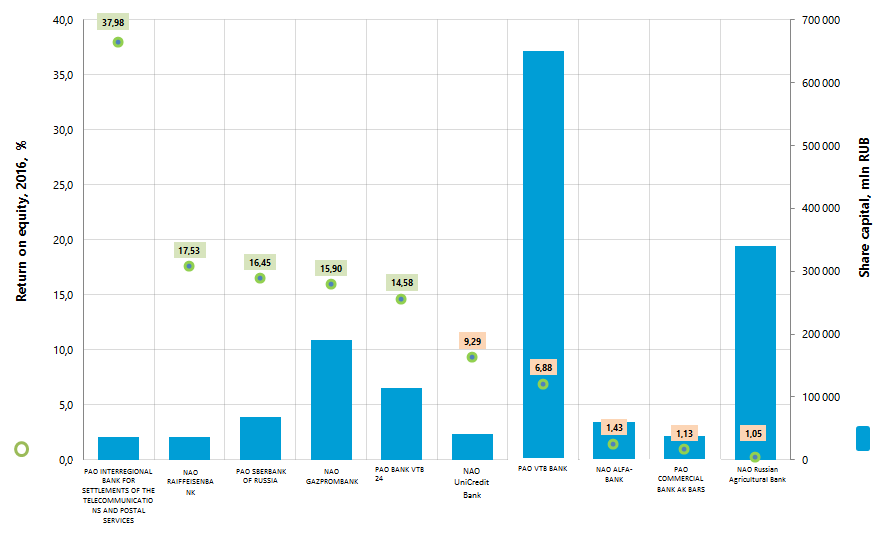

Return on equity of the largest Russian credit institutions

Information agency Credinform offers the ranking of the largest Russian credit institutions. The largest Russian credit institutions with the largest size of equity were selected for the ranking, according to the data of the Central Bank of Russia (CBR) for the reporting period of 2016 (TOP-10). Then they were ranked by the return on equity ratio in 2016 (Table 1).

Return on equity, as one of performance ratios, characterizes the return on bank's capital and is calculated as the relation of net profit to equity of a credit institution. The ratio shows the return on investment of shareholders in terms of accounting profit.

For getting of the most comprehensive and fair picture of the financial standing of an enterprise it is necessary to pay attention to all combination of its financial indicators and ratios.

| Name, BIC, PSRN, region, date of establishment | Share capital, mln RUB | Net profit, 2015, mln RUB | Net profit, 2016, mln RUB | Return on equity, 2015, % | Return on equity, 2016, % | Bank’s financial stability index Globas® |

| PAO INTERREGIONAL BANK FOR SETTLEMENTS OF THE TELECOMMUNICATIONS AND POSTAL SERVICES Moscow BIC 044525848 PSRN 1027700159288 19.05.1991 | 36 864,6 | 10 283,3 | 14 073,3 | 21,06 | 37,98 | 175 The highest |

| NAO RAIFFEISENBANK Moscow BIC 044525700 PSRN 1027739326449 09.06.1996 | 36 711,3 | 20 139,1 | 23 933,1 | 16,13 | 17,53 | 216 High |

| PAO SBERBANK OF RUSSIA Moscow BIC 044525225 PSRN 1027700132195 19.06.1991 | 67 760,8 | 236 256,1 | 516 987,8 | 8,82 | 16,45 | 202 High |

| NAO GAZPROMBANK Moscow BIC 044525823 PSRN 1027700167110 22.01.1992 | 190 234,3 | 34 365,3 | 109 685,1 | 5,32 | 15,90 | 226 High |

| PAO BANK VTB 24 Moscow BIC 044525716 PSRN 1027739207462 17.11.1991 | 113 382,9 | 461,2 | 43 126,1 | 0,17 | 14,58 | 236 High |

| NAO UniCredit Bank Moscow BIC 044525545 PSRN 1027739082106 14.11.1991 | 40 438,3 | 6 003,8 | 16 655,1 | 3,45 | 9,29 | 222 High |

| PAO VTB BANK Moscow BIC 044525187 PSRN 1027739609391 16.10.1990 | 651 033,9 | 48 580,7 | 70 006,6 | 4,79 | 6,88 | 210 High |

| NAO ALFA-BANK Moscow BIC 044525593 PSRN 1027700067328 02.01.1991 | 59 587,6 | 49 591,4 | 5 117,6 | 13,79 | 1,43 | 193 The highest |

| PAO COMMERCIAL BANK AK BARS Republic of Tatarstan BIC 049205805 PSRN 1021600000124 28.11.1993 | 38 015,4 | 9 801,6 | 645,7 | 16,74 | 0,90 | 171 The highest |

| NAO Russian Agricultural Bank Moscow BIC 044525111 PSRN 1027700342890 23.04.2000 | 339 848,0 | 69 207,2 | 909,2 | 16,80 | 0,23 | 180 The highest |

| Total in the group of TOP-10 banks | 1 573 877,0 | 484 689,7 | 801 139,6 | |||

| Average value in the group of TOP-10 banks | 48 469,0 | 801 139,6 | 10,71 | 12,12 | ||

| Industry average value | 1 644,1 | 2 250,7 | 12,37 | 13,05 |

The average values of the return on equity ratio in 2015 - 2016 in the group of TOP-10 banks are below the industry average values (in Table 1 and Picture 1 the green and yellow fillings mark the indicators, which are higher and lower than the industry average values, respectively).

Three banks from the TOP-10 reduced net profit in 2016 in comparison with the previous period (are marked with a red filling in Table 1).

Picture 1. The return on equity and the share capital of the largest Russian banks (TOP-10)

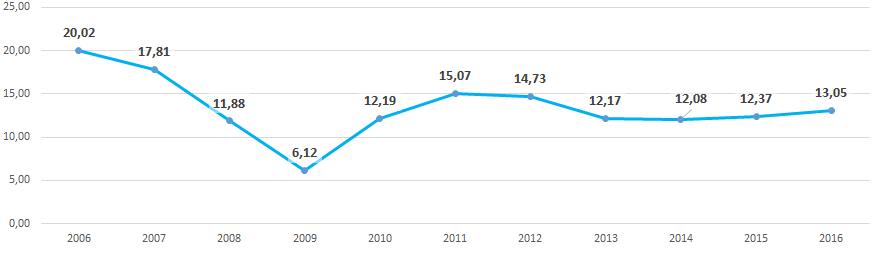

Picture 1. The return on equity and the share capital of the largest Russian banks (TOP-10)The industry average values of the bank's financial stability index (Picture 2) reflect generally the macroeconomic trends. Thus, there is a decrease in ratio values observed in the periods of crisis in the economy in 2007-2009 and in 2013-2014.

Picture 2. Industry average values of the return on equity of the largest Russian banks in 2006 – 2016

Picture 2. Industry average values of the return on equity of the largest Russian banks in 2006 – 2016All TOP-10 banks got the highest and high bank's financial stability index Globas®, that points to their ability to repay their debts in time and fully.