Order a report

Custom-made industry research, company ratings, competitor analysis

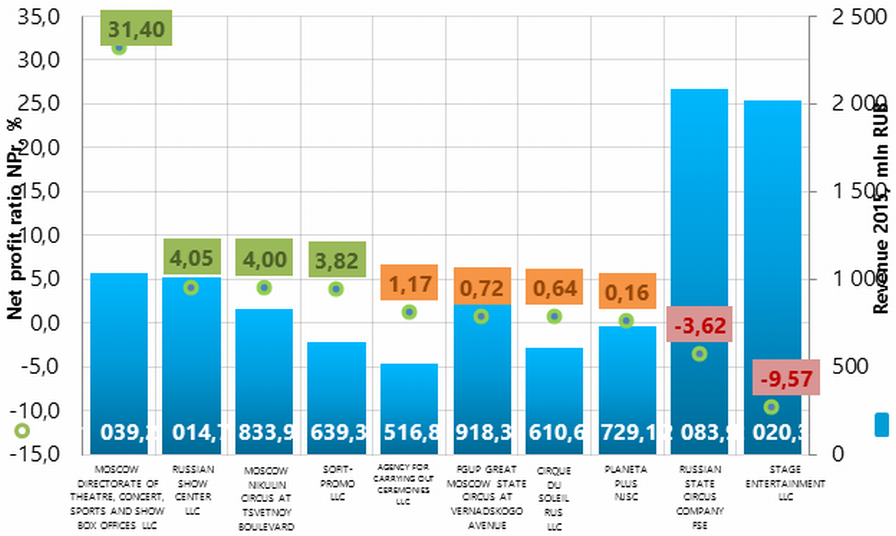

Net profit ratio of the largest Russian creative enterprises in the sphere of art and entertainment

Information agency Credinform has performed a ranking of the largest Russian creative enterprises in the sphere of art and entertainment. Enterprises with the largest annual revenue (TOP-10) for the latest accounting periods available in the State statistical authorities (2015 and 2014) have been selected for the ranking. Then they have been ranked by net profit ratio (Table 1). The analysis was based on data of the Information and Analytical system Globas.

Net profit ratio is calculated as a relation of net profit (loss) to sales revenue, and indicates sales profit rate. There is no standard value for this ratio. It is recommended to compare enterprises within one sector, or change of the ratio in the course of time of a certain company. A negative value of the ratio signals about net loss. A high value shows an efficient operation of the enterprise.

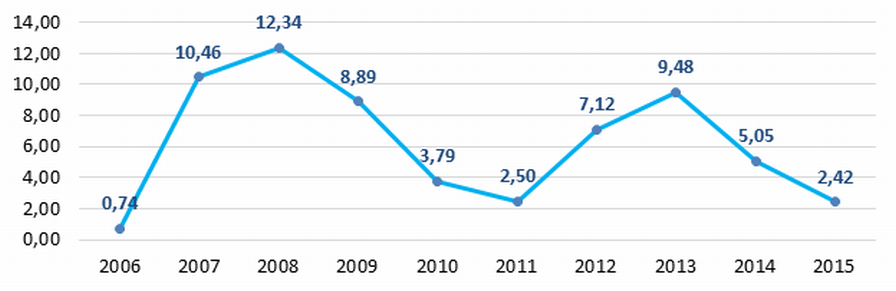

A calculation of practical values of financial ratios, which might be considered as normal for a certain industry, has been developed and implemented in the Information and Analytical system Globas by the experts of Information Agency Credinform, having taken into account the current situation in the economy as a whole and in the industries. The practical value of net profit ratio for creative enterprises in the sphere of art and entertainment in 2015 amounted to 2,42%.

The whole set of financial indicators and ratios of a company is to be considered to get the fullest and fairest opinion about the company’s financial standing.

| Name, INN, region | Net profit, mln RUB | Revenue, mln RUB | NPr, % |

Solvency index Globas® | ||||

| 2014 | 2015 | 2016 | 2014 | 2015 | 2016 | |||

| 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 |

| MOSCOW DIRECTORATE OF THEATRE, CONCERT, SPORTS AND SHOW BOX OFFICES LLC INN 7710944197 Moscow |

198,1 | 326,3 | 264,2 | 868,1 | 1 039,2 | 1 026,5 | 31,40 | 212 High |

| RUSSIAN SHOW CENTER LLC INN 7710666750 Moscow |

37,7 | 41,0 | 17,8 | 1 088,4 | 1 014,7 | 440,3 | 4,05 | 239 High |

| MOSCOW NIKULIN CIRCUS AT TSVETNOY BOULEVARD NJSC INN 7707284367 Moscow |

31,4 | 33,4 | 70,7 | 648,3 | 833,9 | 925,6 | 4,00 | 143 The highest |

| SOFIT-PROMO LLC INN 7839503590 Saint Petersburg |

32,4 | 24,4 | 163,1 | 639,3 | 3,82 | 172 The highest | ||

| AGENCY FOR CARRYING OUT CEREMONIES LLC INN 7725269594 Moscow |

15,4 | 6,1 | 308,3 | 516,8 | 1,17 | 305 Satisfactory | ||

| FGUP GREAT MOSCOW STATE CIRCUS AT VERNADSKOGO AVENUE INN 7736039722 Moscow |

123,9 | 6,6 | 88,9 | 996,0 | 918,3 | 1 125,7 | 0,72 | 165 The highest |

| CIRQUE DU SOLEIL RUS LLC INN 7704704694 Moscow |

-33,8 | 3,9 | -49,8 | 818,6 | 610,6 | 705,2 | 0,64 | 318 Satisfactory |

| PLANETA PLUS NJSC INN 7801140316 Saint Petersburg |

-26,1 | 1,2 | 786,8 | 729,1 | 0,16 | 229 High | ||

| RUSSIAN STATE CIRCUS COMPANY FSE INN 7702060003 Moscow |

43,6 | -75,5 | 49,4 | 1 871,3 | 2 083,9 | 2 116,6 | -3,62 | 263 High |

| STAGE ENTERTAINMENT LLC INN 7704536785 Moscow |

-162,9 | -75,5 | -151,1 | 1 635,8 | 2 020,3 | 1 211,4 | -9,57 | 297 High |

| Total for TOP-10 companies | 259,6 | 174,1 | 9 184,6 | 10 405,9 | ||||

| Average value of TOP-10 companies | 26,0 | 17,4 | 918,5 | 1 040,6 | 3,28 | |||

| Industry average value | 0,4 | 0,1 | 9,5 | 9,6 | 2,42 | |||

*Data for 2016 is given for reference.

The average value of 2015 net profit ratio in TOP-10 companies is higher than the practical value. Four companies of TOP-10 have an index value that is lower than the practical one. Two companies have a negative value, and at the same time, they have the biggest revenue of TOP-10 companies.

Eight of TOP-10 companies have a decrease in revenue or net profit as compared to the prior period, or have loss.

Picture 1. Net profit ratio and revenue of the largest Russian creative enterprises in the sphere of art and entertainment (TOP-10)

Picture 1. Net profit ratio and revenue of the largest Russian creative enterprises in the sphere of art and entertainment (TOP-10)Industry average values of net profit ratio in 2006-2015 (Picture 2) mirror the general macroeconomic situation in the country. Net profit increases during crisis periods.

Picture 2. Change of industry average values of net profit ratio of the largest Russian creative enterprises in the sphere of art and entertainment in 2006 – 2015

Picture 2. Change of industry average values of net profit ratio of the largest Russian creative enterprises in the sphere of art and entertainment in 2006 – 2015 Eight of TOP-10 companies got the highest or a high solvency index Globas, that demonstrates their ability to pay their debts in time and fully.

AGENCY FOR CARRYING OUT CEREMONIES LLC and CIRQUE DU SOLEIL RUS LLC got a satisfactory solvency index Globas, due to information concerning the companies being defendants in debt collection arbitration proceedings, untimely fulfillment of their obligations and unclosed writs of execution. Index development trends are stable.