Order a report

Custom-made industry research, company ratings, competitor analysis

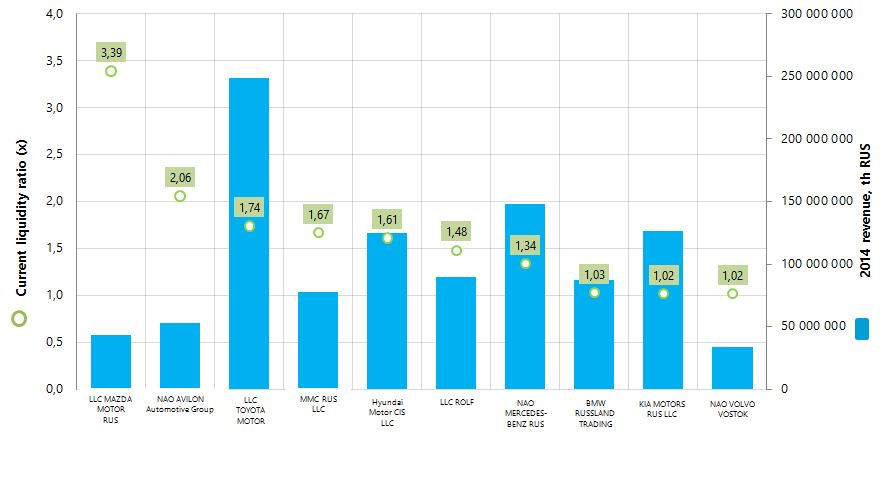

Current liquidity ratio of the largest Russian auto dealers

Information Agency Credinform has prepared the ranking of Russian auto dealers. TOP-10 largest enterprises in terms of revenue were selected according to the data from the Statistical Register for the latest available period (for the year 2014). Then, the companies were ranged by Current liquidity ratio (Table 1).

Current liquidity ratio (х) (coverage ratio) is a ratio of total working capital to short-term liabilities. The ratio shows the sufficiency of company’s assets to meet short-term obligations.

The recommended value is from 1,0 to 2,0. The ratio value less than 1 indicates about the excess of short-term liabilities over current working capital.

For the most full and fair opinion about the company’s financial position, not only compliance with standard values should be taken into account, but also the whole set of financial indicators and ratios.

| Name, INN, Region | 2014 net profit, th RUB | 2014 revenue, th RUB | 2014/2013 revenue, % | Current liquidity ratio, (х) | Solvency index Globas-i |

|---|---|---|---|---|---|

| LLC MAZDA MOTOR RUS INN 7743580770, Moscow |

2 775 897 | 43 119 554 | 120 | 3,39 | 151 The highest |

| NAO AVILON Automotive Group INN 7705133757, Moscow |

1 305 918 | 52 596 319 | 114 | 2,06 | 163 The highest |

| LLC TOYOTA MOTOR INN 7710390358, Moscow region |

4 019 401 | 248 627 531 | 108 | 1,74 | 207 High |

| MMC RUS LLC INN 7715397999, Moscow |

1 510 594 | 77 580 644 | 108 | 1,67 | 208 High |

| Hyundai Motor CIS LLC INN 7703623202, Moscow |

1 227 890 | 124 843 324 | 112 | 1,61 | 238 High |

| LLC ROLF INN 5047059383, Moscow region |

2 732 356 | 89 443 332 | 132 | 1,48 | 190 The highest |

| NAO MERCEDES-BENZ RUS INN 7707016368, Moscow |

5 720 774 | 147 624 280 | 123 | 1,34 | 205 High |

| GESELLSCHAFT MIT BESCHRANKTER HAFTUNG "BMW RUSSLAND TRADING ООО" INN7712107050, Moscow |

-1 002 893 | 87 607 721 | 108 | 1,03 | 263 High |

| KIA MOTORS RUS LLC INN 7728674093, Moscow |

-8 202 055 | 126 362 972 | 104 | 1,02 | 282 High |

| NAO VOLVO VOSTOK INN 5032048798, Kaluga region |

-144 541 | 33 477 074 | 90 | 1,02 | 279 High |

The current liquidity ratio of TOP-10 companies varies from 3,39 to 1,02, that satisfies the lower bound of recommended values. In 2014, with industry average value of 1.28, the average ratio of 10 largest auto dealers amounted to 1,64.

All participants of TOP-10 have the highest and high solvency index Globas-i, that shows their stable financial condition.

First two places of the ranking take LLC MAZDA MOTOR RUS and NAO AVILON Automotive Group with Current liquidity ratios, exceeding the upper bound of recommended values, as current assets of the enterprises significantly exceed short-term liabilities. According to 2013 results the leaders of the ranking were LLC JAGUAR LAND ROVER and HONDA MOTOR RUS LLC with ratio values 3,28 and 2,87 accordingly. According to 2014 results these two companies were not included in TOP-10.

Picture 1. 2014 revenue and current liquidity ratio of the largest Russian auto dealers (TOP-10)

According to 2014 results, the annual revenue of TOP-10 enterprises amounted to 1 031 bln RUB, that is 12% higher than total revenue in 2013. However, net profit indicators of these companies demonstrate negative dynamics. Thus, 2014 total net profit of TOP-10 enterprises amounted to 9,9 bln RUB, it decreased by 53% in comparison with previous period. Only 4 out 10 participants (LLC MAZDA MOTOR RUS, MMC RUS LLC, LLC ROLF, NAO MERCEDES-BENZ RUS) increased net profit in 2014. Other companies showed decline or even net loss.

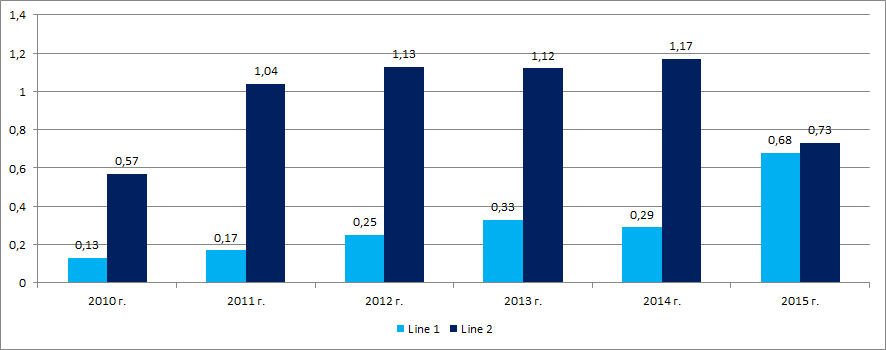

Taking into account the increased inflation and reduced consumer demand, the industry as a whole demonstrates negative dynamics. For example, below is the data from the Federal State Statistics Service about the stock of cars in trade enterprises in comparison with the data about wholesale sales of passenger cars, including light cars, minibuses, special passenger cars etc. (Picture 2).

The analysis shows the threefold increase in car stocks among trade industry in 2015 with almost 40% decline in sales in monetary terms.

Auto dealers are characterized by high concentration of enterprises in Moscow – the largest financial center of the country. This fact is confirmed by the data from the Information and analytical system Globas-i on distribution across the country of 100 largest registered companies of the industry in terms of 2014 revenue (TOP-7 of Regions):

Moscow - 51

Moscow region - 18

Saint-Petersburg - 7

Krasnodar region - 3

Nizhny Novgorod region - 3

Novosibirsk region - 3

Sverdlovsk region - 3