Order a report

Custom-made industry research, company ratings, competitor analysis

Solvency of service companies

Information agency Credinform represents a ranking of the largest Russian service companies. The provided personal services (laundry, dry cleaning of fabric and fur items, hairdressing and beauty salons, funeral services, saunas, wellness centers, fitness centers, social services, pet care, etc.) with the largest volume of annual revenue (TOP-10) were selected for the ranking, according to the data from the Statistical Register for the latest available periods (2006 - 2011). They were ranked by the solvency ratio (Table 1). The analysis was based on the data of the Information and Analytical System Globas.

Solvency ratio (х) is equity to total assets. The ratio indicates the company's dependence on external loans. The recommended value is >0,5.

The value below the minimum limit indicates a strong dependence on external sources of funds, which, if market conditions worsen, can lead to liquidity crisis and unstable financial position of the company.

For the most complete and objective view of the financial condition of the enterprise, it is necessary to pay attention to the complex of indicators and financial ratios of the company.

| Name, INN, region, activity | Revenue, million RUB | Net profit (loss), million RUB | Solvency ratio (x), >0,5 | Solvency index Globas in 2020 | |||

| 2009 | 2011 | 2009 | 2011 | 2009 | 2011 | ||

| 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 |

| LLC LINDSTROM INN 7816659619 Saint Petersburg Laundry and dry cleaning of fabric and fur product |

|

|

|

|

|

|

169 Superior |

| JSC LUZHNIKI OLYMPIC COMPLEX INN 7704077210 Moscow Health and fitness |

|

|

|

|

|

|

232 Strong |

| JSC RITUAL-1 INN 7731137099 Moscow Funeral and related services |

|

|

|

|

|

|

256 Medium |

| GBU RITUAL INN 7743096224 Moscow Funeral and related services |

|

|

|

|

|

|

Not assigned |

| JSC FUNERAL HOME GORBRUS INN 7720018290 Moscow region Funeral and related services |

|

|

|

|

|

|

278 Medium |

| LLC SANDUNOVSKIE BANI INN 7702093778 Moscow Health and fitness |

|

|

|

|

|

|

121 Superior |

| JSC STIKS-S INN 7710321266 Moscow Funeral and related services |

|

|

|

|

|

|

275 Medium |

| JSC PASSAZHIR SERVIS INN 7606043703 Yaroslavl region Laundry and dry cleaning of fabric and fur product |

|

|

|

|

|

|

237 Strong |

| LLC MEGGI-2001 INN 5024048699 Moscow region Laundry and dry cleaning of fabric and fur product |

|

|

|

|

|

|

384 Weak |

| Average value for TOP-10 | |

|

|

|

|

|

|

| Average value for TOP-1000 | |

|

|

|

|

|

|

![]() growth of indicator to the previous period,

growth of indicator to the previous period, ![]() decrease of indicator to the previous period

decrease of indicator to the previous period

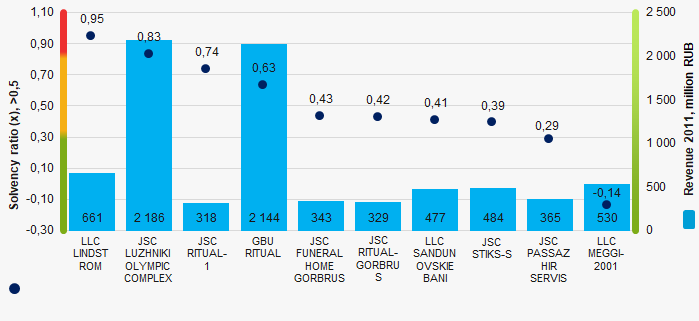

The average indicator of the solvency ratio is above the average value of TOP-1000. Four companies have the value above the recommended one, and four companies improved their figures in 2011 compared to 2009.

Picture 1. Solvency ratio and revenue of the largest service companies (TOP-10)

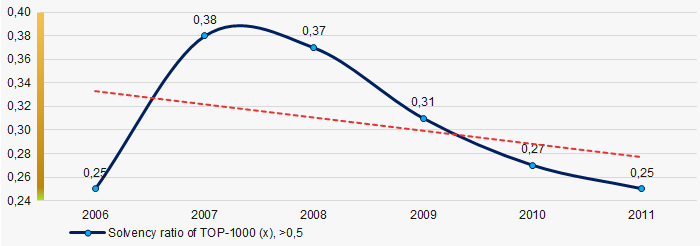

Picture 1. Solvency ratio and revenue of the largest service companies (TOP-10)During six years, the average solvency ratio values of TOP-1000 companies are below the recommended one with a trend to decrease (Picture 2).

Picture 2. Change in the average solvency ratio values of the largest Russian service companies (TOP-1000) in 2006 – 2011

Picture 2. Change in the average solvency ratio values of the largest Russian service companies (TOP-1000) in 2006 – 2011