Order a report

Custom-made industry research, company ratings, competitor analysis

Loan security of companies on UTII

Information agency Credinform presents a ranking of Russian companies on unified tax on imputed income. The largest companies (TOP-10) in terms of annual revenue were selected according to the data from the Statistical Register for the available periods (2017-2019). Then the companies were ranged by loan protection factor (Table 1). The analysis was based on the data from the Information and Analytical system Globas.

Loan protection factor (x) is the ratio of pre-tax earnings and loan interest to the sum of interest payable. It characterizes the security level of creditors from non-payment of interest for the granted loan and shows how many times during the reporting period the company earned means to pay the interest on loans.

The recommended value is >1. No indicator value indicates that the company does not have borrowed funds, therefore, no interest payable to creditors. However, it may not always be the evidence of general well-being as credit resources are necessary for a successful business growth.

In order to get the most comprehensive and fair picture of the financial standing of an enterprise, it is necessary to pay attention to all combination of financial indicators and ratios.

| Name, INN, region | Revenue, million RUB | Net profit (loss), million RUB | Loan protection factor (x), >1 | Solvency index Globas | |||

| 2018 | 2019 | 2018 | 2019 | 2018 | 2019 | ||

| 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 |

| FARMLEND INN 0273028277 Republic of Bashkortostan |

|

|

|

|

|

|

233 Strong |

| JSC PHARMACEUTICAL IMPORT, EXPORT INN 7710106212 Moscow |

|

|

|

|

|

|

202 Strong |

| OOO TK RESURS-YUG INN 2303024188 Moscow |

|

|

|

|

|

|

258 Medium |

| JSC AVTODOM INN 7714709349 Moscow |

|

|

|

|

|

|

247 Strong |

| JSC IPC-AMURNNEFTEPRODUCT INN 2801013238 Amur region |

|

|

|

|

|

|

272 Medium |

| OJSC ILE DE BEAUTE INN 7707061530 Moscow |

|

|

|

|

|

|

305 Adequate |

| LLC OCTOBLUE INN 5029086747 Moscow region |

|

|

|

|

|

220 Strong | |

| JSC NC ROSNEFT – SMOLENKNEFTEPRODUKT INN 6730017336 Smolensk region |

|

|

|

|

208 Strong | ||

| LLC MONEKS TRADING INN 7710323601 Moscow |

|

|

|

|

263 Medium | ||

| JSC LIPETSKNEFTEPRODUKT INN 4822000201 Lipetsk region |

|

|

|

|

296 Medium | ||

| Average value for TOP-10 companies | |

|

|

|

|

|

|

| Average value for TOP-1000 companies | |

|

|

|

|

|

|

![]() improvement compared to prior period,

improvement compared to prior period, ![]() decline compared to prior period

decline compared to prior period

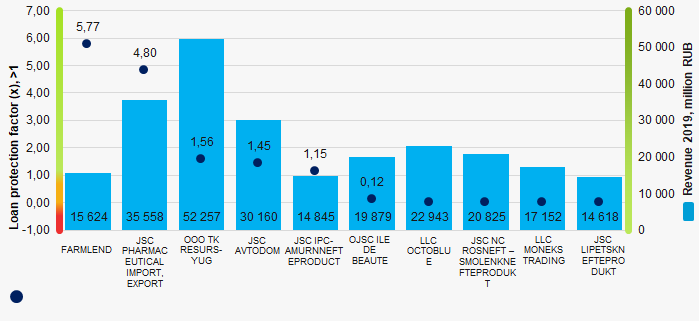

Average value of loan protection factor of TOP-10 is lower than the average value of TOP-1000. Three companies out of six have improved their values in 2019 comparing to the previous period.

Picture 1. Loan protection factor and revenue of the largest Russian companies on UTII (TOP-10)

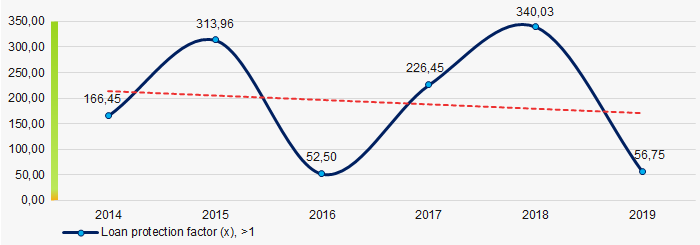

Picture 1. Loan protection factor and revenue of the largest Russian companies on UTII (TOP-10)During 6 years, average values of loan protection factor had a tendency to decrease. (Picture 2).

Picture 2. Change in average values of the loan protection factor of the largest (TOP-1000) Russian companies on UTII in 2014 – 2019

Picture 2. Change in average values of the loan protection factor of the largest (TOP-1000) Russian companies on UTII in 2014 – 2019