Order a report

Custom-made industry research, company ratings, competitor analysis

Activity trends of wine making companies

Information agency Credinform has prepared a review of activity trends of the largest Russian wine producers.

The largest companies (ТОP-100) engaged in grape growing and wine production in terms of annual revenue were selected according to the data from the Statistical Register for the latest available periods (2013 - 2018). The analysis was based on data of the Information and Analytical system Globas.

Net assets is a ratio reflecting the real value of company's property. It is calculated annually as the difference between assets on the enterprise balance and its debt obligations. The ratio is considered negative (insufficiency of property), if company’s debt exceeds the value of its property.

The largest winery in terms of net assets is NAO ABRAU-DYURSO, INN 2315092440, Krasnodar region. In 2018 net assets of the company amounted to more than 4,5 billion RUB. The smallest size of net assets in TOP-100 had LLC LAZURNAYA YAGODA, INN 2309107440, Krasnodar region. The lack of property of the company in 2018 was expressed in negative terms -1,7 billion RUB.

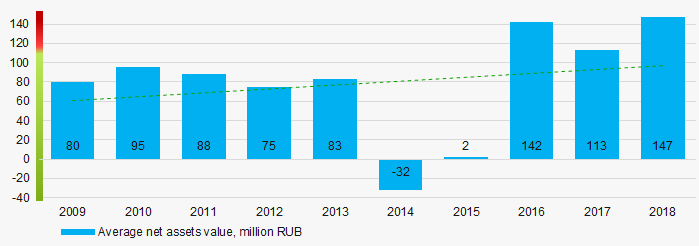

For the last ten years, the average values of net assets showed the growing tendency (Picture 1).

Picture 1. Change in average net assets value in 2009 – 2018

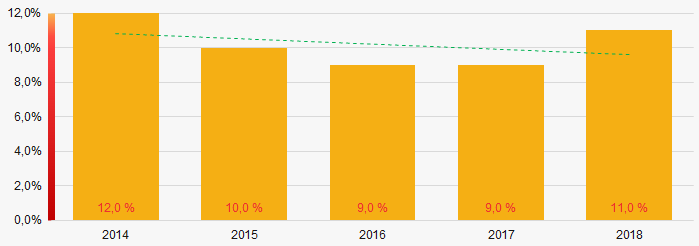

Picture 1. Change in average net assets value in 2009 – 2018For the last five years, the share of ТОP-100 enterprises with lack of property showed the decreasing tendency (Picture 2).

Picture 2. The share of enterprises with negative net assets value in ТОP-100

Picture 2. The share of enterprises with negative net assets value in ТОP-100Sales revenue

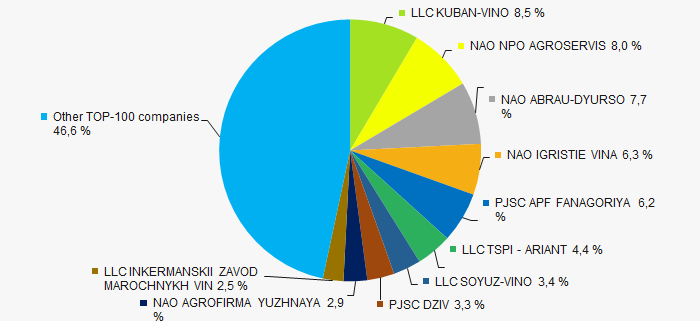

In 2018, the total revenue of 10 largest companies amounted to 53% from ТОP-100 total revenue (Picture 3). This fact testifies the high level of monopolization.

Picture 3. Shares of TOP-10 in TOP-100 total revenue for 2018

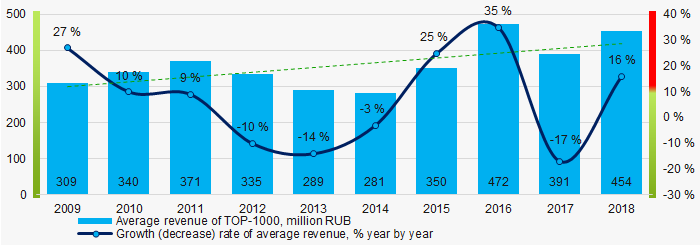

Picture 3. Shares of TOP-10 in TOP-100 total revenue for 2018In general, the growing trend in sales revenue is observed (Picture 4).

Picture 4. Change in average revenue in 2009 – 2018

Picture 4. Change in average revenue in 2009 – 2018Profit and loss

The largest company in terms of net profit is also NAO ABRAU-DYURSO, INN 2315092440, Krasnodar region. In 2018 the company’s profit amounted to 1,2 billion RUB.

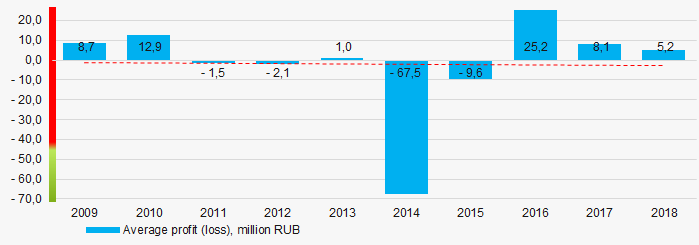

For the last ten years, the average profit values were negative within four years. In general, the decreasing tendency is observed (Picture 5).

Picture 5. Change in average profit (loss) in 2009 – 2018

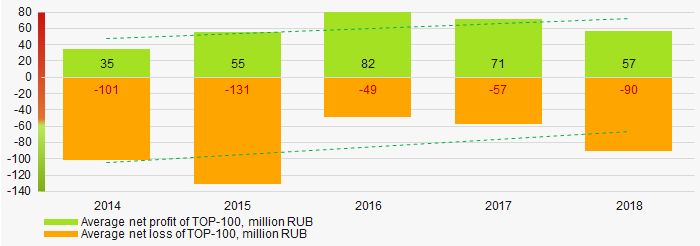

Picture 5. Change in average profit (loss) in 2009 – 2018Over a five-year period, the average net profit values of ТОP-100 show the growing tendency, along with this the average net loss is decreasing (Picture 6).

Picture 6. Change in average net profit/loss of ТОP-100 companies in 2014 – 2018

Picture 6. Change in average net profit/loss of ТОP-100 companies in 2014 – 2018Main financial ratios

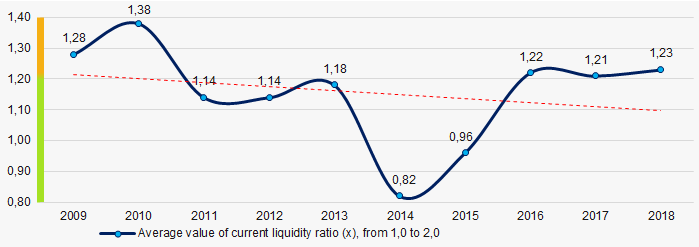

For the last ten years, the average values of the current liquidity ratio were within the recommended values - from 1,0 to 2,0, with decreasing tendency (Picture 7).

The current liquidity ratio (ratio of total working capital to short-term liabilities) shows the sufficiency of company’s assets to meet short-term obligations.

Picture 7. Change in average values of current liquidity ratio in 2009 – 2018

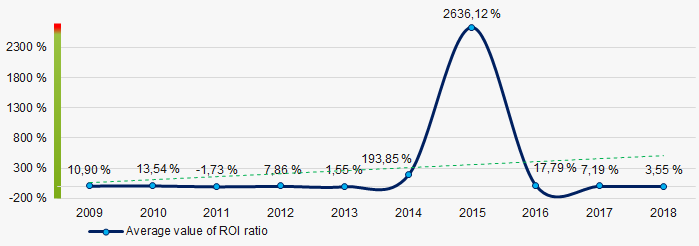

Picture 7. Change in average values of current liquidity ratio in 2009 – 2018For the last ten years, the growing tendency of ROI ratio is observed (Picture 8).

The ROI ratio is calculated as a ratio of net profit to sum of stockholder equity and long-term liabilities and shows the return from equity involved in commercial activities and long-term borrowed funds.

Picture 8. Change in average values of ROI ratio in 2009 – 2018

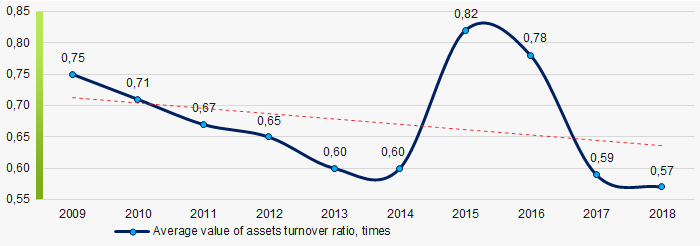

Picture 8. Change in average values of ROI ratio in 2009 – 2018Assets turnover ratio is the ratio of sales revenue and company’s average total assets for a period. It characterizes the effectiveness of using of all available resources, regardless the source of their attraction. The ratio shows how many times per year the full cycle of production and circulation is performed, generating the corresponding effect in the form of profit.

For the last ten years, this business activity ratio demonstrated the downward trend (Picture 9).

Picture 9. Change in average values of assets turnover ratio in 2009 – 2018

Picture 9. Change in average values of assets turnover ratio in 2009 – 2018 Small businesses

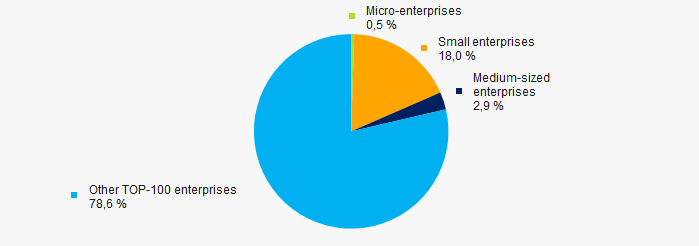

58% of ТОP-100 companies are registered in the Unified register of small and medium-sized enterprises of the Russian Federal Tax Service. Herein, their share in TOP-100 total revenue amounted to 21,4%, which is slightly lower than national average value (figure 10).

Picture 10. Shares of small and medium-sized enterprises in ТОP-100

Picture 10. Shares of small and medium-sized enterprises in ТОP-100Main regions of activity

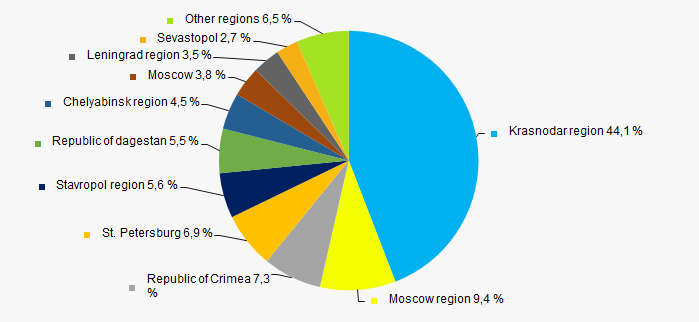

ТОP-100 companies are registered in 18 regions and unequally located across the country, taking into account the geographical location and climatic characteristics of the raw material base. More than 44% of the largest enterprises in terms of revenue are located in Krasnodar region (Picture 11).

Picture 11. Distribution of TOP-100 revenue by regions of Russia

Picture 11. Distribution of TOP-100 revenue by regions of RussiaFinancial position score

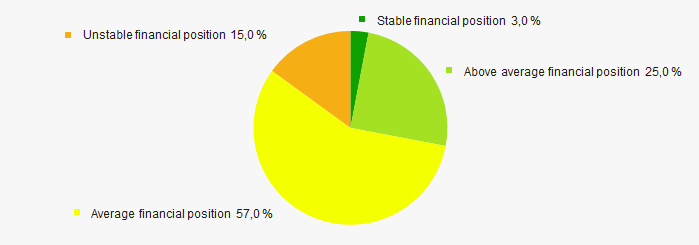

An assessment of the financial position of TOP-100 companies shows that the largest part have the average financial position (Picture 12).

Picture 12. Distribution of TOP-100 companies by financial position score

Picture 12. Distribution of TOP-100 companies by financial position scoreSolvency index Globas

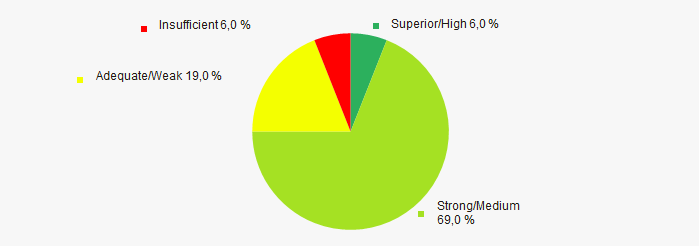

Most of TOP-100 companies got superior/high or strong/medium Solvency index Globas, this fact shows the ability of the companies to meet their obligations in time and fully (Picture 13).

Picture 13. Distribution of TOP-100 companies by Solvency index Globas

Picture 13. Distribution of TOP-100 companies by Solvency index GlobasConclusion

A complex assessment of the largest Russian wine producers, taking into account the main indexes, financial ratios and indicators, demonstrates the presence of positive trends (Table 1).

| Trends and assessment factors | Relative share, % |

| Growth/drawdown rate of average net assets value | |

| Increase / decrease in the share of enterprises with negative net assets | |

| The level of competition / monopolization | |

| Growth/drawdown rate of average revenue | |

| Growth/drawdown rate of average net profit (loss) | |

| Increase / decrease in average net profit of ТОP-100 companies | |

| Increase / decrease in average net loss of ТОP-100 companies | |

| Increase / decrease in average values of current liquidity ratio | |

| Increase / decrease in average values of ROI ratio | |

| Increase / decrease in average values of assets turnover ratio, times | |

| Share of small and medium-sized businesses by revenue more than 22% | |

| Regional concentration | |

| Financial position (the largest share) | |

| Solvency index Globas (the largest share) | |

| Average value of factors | |

![]() favorable trend (factor),

favorable trend (factor), ![]() unfavorable trend (factor).

unfavorable trend (factor).