Order a report

Custom-made industry research, company ratings, competitor analysis

Profitability of management companies of housing and utilities

Information agency Credinform offers a ranking of the largest Russian enterprises of housing management sector. The companies with the largest volume of annual revenue (TOP-10) were selected for the ranking, according to the data from the Statistical Register for the latest available periods (2015 - 2017). Then they were ranked by equity turnover ratio (Table 1). The analysis is based on data of the Information and Analytical system Globas.

Net profit ratio (%) is calculated by dividing net profit (loss) by net sales and demonstrates the company’s profutablity of sales.

There is no statutory value for the ratio, that is why it is recommended to compare companies of the same industry or time-varying behavior of the ratio of a particular company. Negative value of indicators speaks for the company’s net loss. The higher is the indicator, the more efficiently the company operates.

The experts of the Information agency Credinform, taking into account the actual situation both in the economy as a whole and in sectors, have developed and implemented in the Information and Analytical system Globas the calculation of practical values of financial ratios that can be recognized as normal for a particular industry. For enterprises engaged in housing management the practical value of net profit ratio is from 1,03%.

For the most complete and objective view of the financial condition of the enterprise it is necessary to pay attention to the complex of indicators and financial ratios of the company.

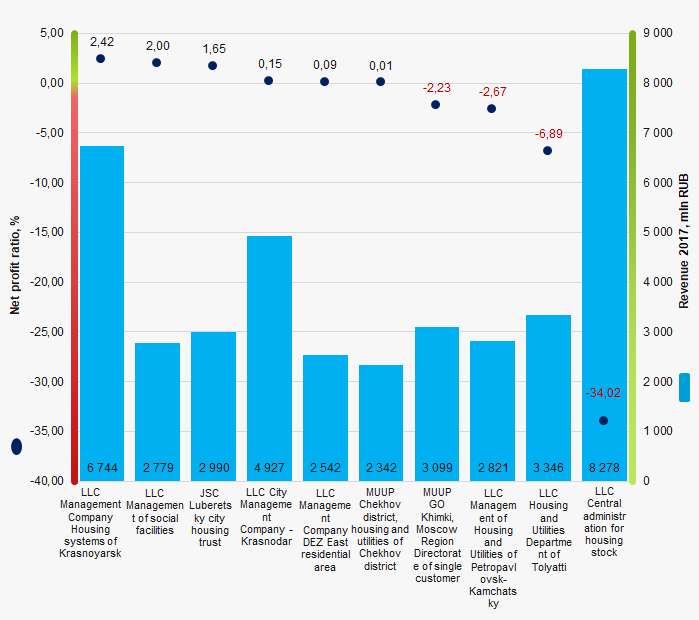

| Name, INN, region | Revenue, mln RUB | Net profit (loss), mln RUB | Net profit ratio, % | Net profit ratio, % Globas | |||||||||

| 2016 | 2017 | 2016 | 2017 | 2016 | 2017 | ||||||||

| 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | ||||||

| LLC Management Company Housing systems of Krasnoyarsk INN 2461201672 Krasnoyarsk territory |

2329,4 | 6744,0 | -14,6 | 163,0 | -0,63 | 2,42 | 249 Strong | ||||||

| LLC Management of social facilities INN 8608053160 Khanty-Mansi autonomous district - Yugra |

2725,1 | 2778,5 | 107,7 | 55,6 | 3,95 | 2,00 | 234 Strong | ||||||

| JSC Luberetsky city housing trust INN 5027130207 Moscow region |

2739,2 | 2989,6 | 11,1 | 49,5 | 0,41 | 1,65 | 210 Strong | ||||||

| LLC City Management Company - Krasnodar INN 2311104687 Krasnodar territory |

4698,6 | 4926,7 | 4,5 | 7,2 | 0,10 | 0,15 | 230 Strong | ||||||

| LLC Management Company DEZ East residential area INN 8602021147 Khanty-Mansi autonomous district - Yugra |

2415,8 | 2542,3 | 1,9 | 2,4 | 0,08 | 0,09 | 242 Strong | ||||||

| MUUP Chekhov district housing and utilities of Chekhov district INN 5048052077 Moscow region |

2063,0 | 2341,8 | -31,9 | 0,3 | -1,55 | 0,01 | 212 Strong | ||||||

| MUUP GO Khimki, Moscow Region Directorate of a single customer INN 5047054547 Moscow region In process of reorganization in the form of merger of other legal entities since 20.11.2017 |

3129,7 | 3098,7 | -145,6 | -69,2 | -4,65 | -2,23 | 325 Adequate | ||||||

| LLC Management of Housing and Utilities of Petropavlovsk-Kamchatsky INN 4101122429 Kamchatka territory |

3344,9 | 2820,7 | -80,1 | -75,2 | -2,39 | -2,67 | 378 Adequate | ||||||

| LLC Housing and Utilities Department of Tolyatti INN 6321300279 Samara region |

3639,0 | 3346,5 | 17,6 | -230,6 | 0,48 | -6,89 | 333 Adequate | ||||||

| LLC Central administration for housing stock INN 7704307993 Moscow A case of recognition the company bankrupt is considered |

10207,5 | 8278,4 | -1 510,3 | -2 815,9 | -14,80 | -34,02 | 550 Insufficient | ||||||

| Total for TOP-10 companies | 37292,1 | 39867,4 | -1639,7 | -2912,9 | |||||||||

| Average value for TOP-10 companies | 3729,2 | 3986,7 | -164,0 | -291,3 | -1,90 | -3,95 | |||||||

| Industry average value | 11,6 | 11,6 | 0,2 | 0,1 | 1,39 | 1,03 | |||||||

— growth of indicator to the previous period, — decrease of indicator to the previous period.

Over the five-year period, the average size of the net assets of TOP-1000 companies tend to increase (Picture 1).

The average indicator of net profit ratio of TOP-10 companies is below the industry average. Seven companies of TOP-10 demonstrated the upside in 2017.

Picture 1. Net profit ratio and revenue of the largest Russian companies of housing management sector (TOP-10)

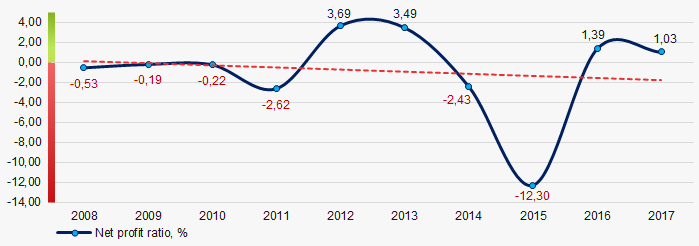

Picture 1. Net profit ratio and revenue of the largest Russian companies of housing management sector (TOP-10)Over the past 10 years, the industry average values of net profit ratio have a trend to decrease (Picture 2).

Picture 2. Change in the average industry values of net profit ratio of the largest Russian companies of housing management sector in 2008 – 2017

Picture 2. Change in the average industry values of net profit ratio of the largest Russian companies of housing management sector in 2008 – 2017