Order a report

Custom-made industry research, company ratings, competitor analysis

Russia in the frame of interrelations with the new economic leaders - China and India

The 21st St. Petersburg International Economic Forum (SPIEF), traditionally gathering leading politicians, representatives of the largest businesses and business circles, took place in Saint Petersburg from June 1–3, 2017. Special attention in the program of 2017 was given to India and China.

The subject of the Forum and interest to these countries are expectable, because under complicated relations with the western partners Russia widens integration contacts not only among EAEC members but also with new centers of East and South Asia where two the world-largest economies are forming. Experts in Russia and abroad pay undeservedly little attention to this matter: the GDP volumes are traditionally compared by the nominal rate of the national currency to the US dollar. Developing countries are remarkably behind the Golden billion in this comparison. This includes Russia, being on a small-scale position especially after the rouble devaluation.

However the accuracy of such analyses could be called into question due to the differences in purchasing power of currencies and price level on similar products in different countries. Applying the calculation by purchasing-power parity (PPP), the GDP of China exceeds the USA’s one and consolidated GDP of the EU countries. The point is that India today is the third among the largest economies, living Japan and Germany behind, and significantly outrunning China by the GDP growth (see table 1).

| Rank | Country | GDP (PPP),$ trn | GDP growth at the end of 2016, % | |

| 1 |  |

China | 23,2 | 6,7 |

| - |  |

EU | 20,9 | 1,9 |

| 2 |  |

USA | 19,4 | 1,6 |

| 3 |  |

India | 9,5 | 7,0 |

| 4 |  |

Japan | 5,4 | 1,0 |

| 5 |  |

Germany | 4,1 | 1,9 |

| 6 |  |

Russia | 3,9 | -0,2 |

| 7 |  |

Indonesia | 3,3 | 5,0 |

| 8 |  |

Brazil | 3,2 | -3,4 |

| 9 |  |

Great Britain | 2,9 | 2,0 |

| 10 |  |

France | 2,8 | 1,3 |

1According to the IMF (International Monetary Fund: Forecasted estimates for 2017)

Asia is gradually becoming the center of global development, and it is more than ever important for Russia to stand in with this region both in policy and mutual commodity turnover.

Dynamics of external turnover of Russia with China and India

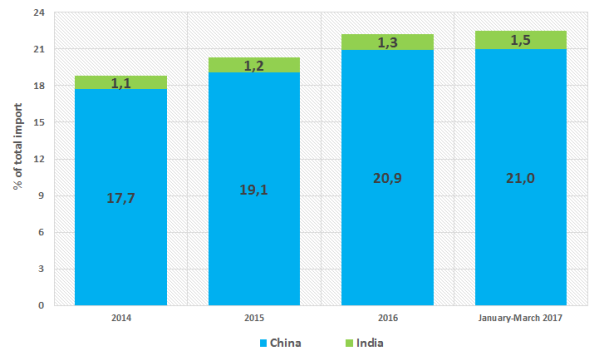

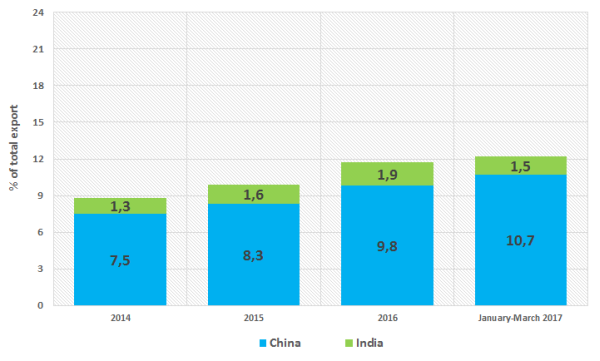

By the volume of commodity turnover India takes a back seat among countries involved in commercial relations with Russia. However there is a positive dynamics: its share in the total import volume amounted to 1,1% in 2014, but it was 1,3% in 2016 (19th rank). Supplies of the Russian goods to the Indian market are also not exceeded 2% (16th rank) of the total volume of the Russian export in monetary terms.

Speaking about the other Russian’s neighbor in the east, there is a different situation. China is the 1st by import and the 2nd by export (after the Netherlands), and its share is on the rise: following the results of January-March 2017, the share of import amounted to 21% of total volume in monetary terms, and of export - to 10,7% (see pictures 1.1 and 1.2).

Picture 1.1. Share of China and India in the RF’s import, % of its total volume in monetary terms

Picture 1.1. Share of China and India in the RF’s import, % of its total volume in monetary terms Picture 1.2. Share of China and India in the RF’s export, % of its total volume in monetary terms

Picture 1.2. Share of China and India in the RF’s export, % of its total volume in monetary termsStructure of external turnover of Russia with China and India

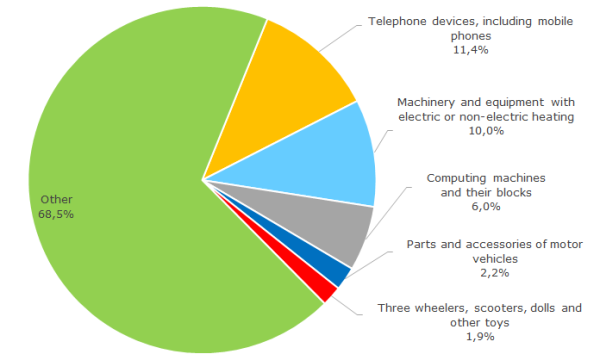

China supplies a broad list of products to the Russian market: various equipment and machinery, clothing, toys, fabrics. Following the results of 2016, the highest volume of purchases fell for mobile and fixed-line phones – 11,4% of total import in monetary terms; machinery and equipment with electric and non-electric heating – 10%; computing machinery – computers, facilities for record and storage of information – 6%; parts and accessories for cars – 2,2%; kids bikes, scooters, toys – 1,9%.

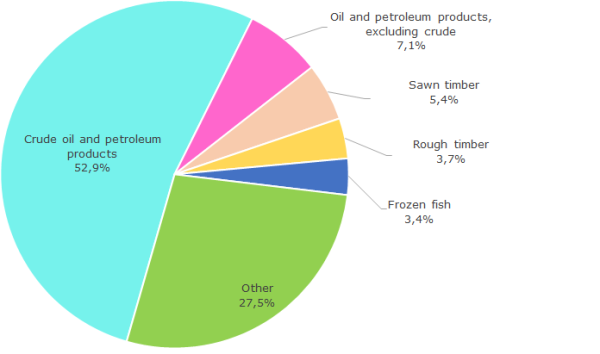

Speaking about export from the RF to China, unfortunately, low value-added goods are leading – oil and oil products, sawn and rough timber (see pictures 2.1 and 2.2).

Picture 2.1. Structure of import from China to Russia, % of its total volume in monetary terms in 2016

Picture 2.1. Structure of import from China to Russia, % of its total volume in monetary terms in 2016 Picture 2.2. Structure of export from Russia to China, % of its total volume in monetary terms in 2016

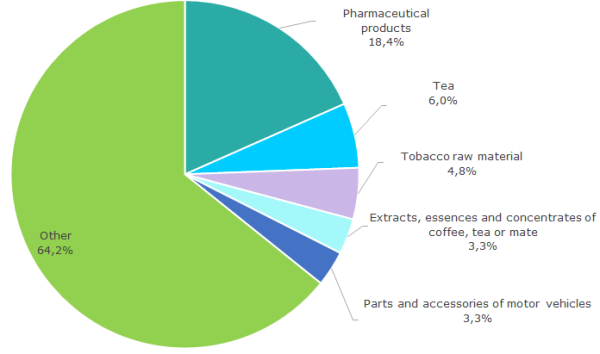

Picture 2.2. Structure of export from Russia to China, % of its total volume in monetary terms in 2016Distinctive feature of the Indian import is supply of pharmaceutical products to the Russian market – 18,4% of total volume, as well as tea, tobacco, coffee, extracts and essences from plants growing in humid temperate climate – 14,1% of annual import.

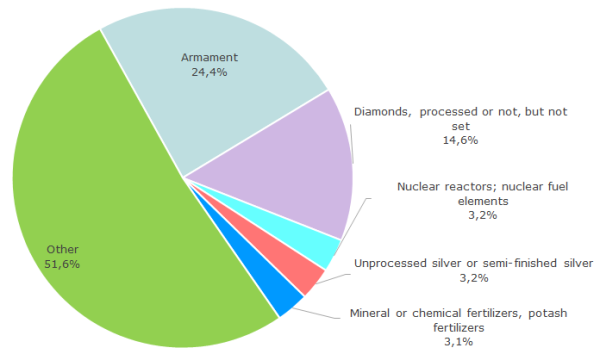

In its trade with India, Russia specializes in hi-tech goods: first of all, in the armament, being the principal exports – 24,4% of total proceeds in cash or 1,3 bln US dollars in 2016 (see pictures 3.1 and 3.2). India also procures nuclear fuel elements from Russia and continues the second construction phase of Kudankulam Nuclear Power Plant – common project of two states in nuclear power. Taking into account the population exceeding billion, India’s electrical demand is huge.

Picture 3.1. Structure of import from India to Russia, % of its total volume in monetary terms in 2016

Picture 3.1. Structure of import from India to Russia, % of its total volume in monetary terms in 2016 Picture 3.2. Structure of export from Russia to India, % of its total volume in monetary terms in 2016

Picture 3.2. Structure of export from Russia to India, % of its total volume in monetary terms in 2016The largest business in Russia with Chinese or Indian controlling participation

According to the Information and Analytical system Globas, currently there are about 790 active companies in Russia with dominant Chinese participation (controlling stake in the capital belongs to natural persons or legal entities from China). The table 2 contains companies largest in term of annual turnover (Top-5). These are enterprises of various sectors: telecommunications, gas filling stations, real estate, auto sales. While the EU authorities artificially limit the contacts of their entrepreneurs with Russia, Chinese investors actively aspire the Russian market.

| Rank | Company | Business scope | Revenue, 2015, bln RUB |

| 1 | ZTE-Communication Technologies, Ltd. ИНН: 7717147218 |

Telecommunications and mobile communications | 9,7 |

| 2 | LTD PHAETON - FUEL NETWORK NUMBER 1 ИНН: 7813474313 |

Trade with fuel, chain of gas filling stations | 6,8 |

| 3 | Geely Motors LLC ИНН: 7716641537 |

Sale of cars | 5,4 |

| 4 | JOINT-STOCK COMPANY RUSTEHNOLOGII LLC ИНН: 7114502310 |

Production of galvanized steel | 4,4 |

| 5 | ZAO BALTIC PEARL ИНН: 7801377058 |

Developer | 4,2 |

Currently there are 60 companies in Russia under Indian control, that is not to the potential of cooperation. The companies are mainly engaged in production of pharmaceuticals. The largest among them is Glenmark Impex LLC with annual turnover about 3 bln RUB.

| Rank | Company | Business scope | Revenue, 2015, bln RUB |

| 1 | Glenmark Impex LLC ИНН: 7709345865 |

Pharmaceutical industry | 3,0 |

| 2 | AGT LLC ИНН: 6165173567 |

Agriculture | 1,7 |

| 3 | ZAO DINA INTERNATIONAL ИНН: 7724586008 |

Sale and maintenance of medical equipment | 1,2 |

| 4 | Sun Pharmaceutical Industries Ltd. ИНН: 7728638440 |

Pharmaceutical industry | 0,9 |

| 5 | Hreya Life Sciences Ltd. ИНН: 7715641990 |

Pharmaceutical industry | 0,7 |

India demonstrates impressive development rates. Once backward, the country now has and develops new industries – pharmaceutical, electronic, IT, etc. Domestic business structures should size up the market, which will be the first in the world by a number of consumers in the near future. According to the population counter, 1 316 mln. people currently live in India, and 1 383 mln. – in PR China. Moreover, India is traditionally wary of China and could become a kind of counterbalance, taking into account significant negative trade balance of the country with PRC: the volume of the Russian export to China is one third less than import from this country.

Currently Russia and PRC have close cooperation in both economy and politics. The country is becoming important for the Russian energy corporations (construction of “The Power of Siberia” gas pipeline is at the final stage). At the same time, considering the scale of potential demand, products of manufacturing industry and agriculture still have a very weak position in export structure.

Russia has turned to the East. This is proved by good level of political relations with new world leaders and participation in development of economic connections being profitable for all parties. The SPIEF’17 has also demonstrated this fact with a number of major agreements signed within its frameworks: agreement on the amount of 239,4 bln RUB (4,2 bln US dollars) between the SC "Rosatom" and the Indian Atomic Energy Corporation on the construction of the 5th and 6th power units at the Kudankulam NPP; agreement on the amount of 28,5 bln RUB between EuroChem MHC and the Chinese corporation ChemChina on a joint industrial production in Russia; and other promising agreements.