Order a report

Custom-made industry research, company ratings, competitor analysis

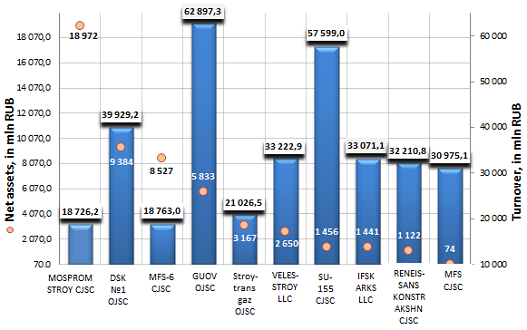

Net assets of building companies of Moscow and Moscow region

Information agency Credinform offers to get acquainted with the ranking of building companies of Moscow and Moscow region. The companies with the highest volume of revenue involved in this activity were selected in the mentioned region by the experts according to the data from the Statistical Register for the latest available period (for the year 2013). Then, the first 10 enterprises selected by turnover were ranked by decrease in net assets index.

Net assets index is one of key indicators of activity of any commercial organization. This index is calculated as a difference between total assets and total liabilities.

Net assets of a company should be at least positive. Negative net assets – it is a sign of the failure of an enterprise, pointing to that it is completely dependent on creditors and hasn’t own funds.

Net assets should be not only positive, but also should exceed the amount of the authorized capital of an enterprise. It means that in its course of business a company not only hasn’t gone through funds primarily invested by the owner, but also has ensured their gain. Net assets being less than the authorized capital is permissible only for newly founded enterprises in the first year worked. In the following years if net assets will become less than the authorized capital, the civil code and the legislation on joint-stock companies demand to reduce the authorized capital down to the value of net assets. If an organization has the authorized capital being so then at minimum level (10 000 RUB), it is opened a question about its further existence.

| № | Name, INN | Net assets, 2013, ths RUB | Authorized capital, 2013, ths RUB | Turnover, 2013, mln RUB | Solvency index GLOBAS-i® |

|---|---|---|---|---|---|

| 1 | Mospromstroy CJSC INN 7710034310 |

18 971 686 | 120 000 | 18 726 | 236 (high) |

| 2 | Domostroitelny kombinat №1 OJSC INN 7714046959 |

9 384 087 | 248 | 39 929 | 200 (high) |

| 3 | Mosfundamentstroy-6 CJSC INN 7711006612 |

8 526 691 | 4400 | 18 763 | 200 (high) |

| 4 | Glavnoe upravlenie obustroystva voysk OJSC INN 7703702341 |

5 833 223 | 3 013 611 | 62 897 | 251 (high) |

| 5 | Stroytransgaz OJSC INN 5700000164 |

3 166 657 | 125 269 | 21 027 | 267 (high) |

| 6 | Velesstroy LLC INN 7709787790 |

2 649 899 | 9 393 | 33 223 | 323 (satisfactory) |

| 7 | Stroitelnoe upravlenie№155 CJSC INN 7736003162 |

1 456 129 | 1203 | 57 599 | 211 (high) |

| 8 | Investitsionno-finansovaya stroitelnaya kompaniya ARKS LLC INN 7714275324 |

1 440 635 | 4000 | 33 071 | 224 (high) |

| 9 | Reneissans konstrakshn CJSC INN 7708185129 |

1 122 301 | 50 000 | 32 211 | 192 (the highest) |

| 10 | Monolit-fundamentstroy CJSC INN 7714266785 |

74 003 | 10 | 30 975 | 204 (high) |

First of all it should be noted that the amount of net assets of all TOP-10 companies conforms to the level, established under legislation of the RF, i.e. exceed the amount of their authorized capital.

Picture. Net assets of building companies of Moscow and Moscow region, TOP-10

The first place of the ranking belongs to the company Mospromstroy CJSC, which showed the highest value of net assets among building companies of Moscow and Moscow region. The enterprise is one of long-livers of Russian construction market. Going beyond Moscow, it implements actively regional projects of industrial and housing construction. Considering the combination of financial and non-financial indicators the company got a high solvency index GLOBAS-i®, what points to its ability to pay off its debt in time, with minimal risk of default.

The largest on turnover building company of the metropolitan area - Glavnoe upravlenie obustroystva voysk OJSC - took the 4th place in the ranking, with the net assets index at the rate of 5833 mln RUB, what significantly outweighs the amount of the company’s authorized capital and answers to the recommended standards. The company also got a high solvency index GLOBAS-i®, that testifies to its financial stability.

In spite of that the amount of net assets of all TOP-10 companies meets the requirements of the legislation of the RF on the combination of financial and non-financial indicators the company Velesstroy LLC got a satisfactory solvency index GLOBAS-i®. Therefore, the solvency margin of this organization doesn’t guarantee that debts will be paid off in time and fully.

Now therefore, the enterprises should control the amount of net assets to avoid the liquidation by tax authorities.