Order a report

Custom-made industry research, company ratings, competitor analysis

Isolation of Russia is canceled

Dear Madams and Sirs,

In spite of the significant cooling in relations with the Occident, EU states coalition remains the main foreign trade partner of Russia. 48,2% of trade in monetary terms (377,4 bln US Dollars) has fallen to its share in 2014. Remarkably, Russia is the third by importance for EU for that matter after China and the USA.

However, sanctions war and stagnation of the Russian economy have resulted in reduction of the total turnover value with EU by 9,6%.

In general, the trade volume of Russia with other countries amounted to 783,5 bln US Dollars in 2014, that is 7% lower than in 2013 (842,2 bln Dollars in 2013; maximum for the whole post-Soviet period). 239 countries and territories were involved in export-import operations with Russia.

Import for the period under review has reduced more than the Russian export: import by 9,2% and export by 5,6%. In monetary terms import amounted to 285,9 bln US Dollars, export to 497,6 bln US Dollars.

The main reason of import reduction was devaluation of the rouble in the whole 2014, as well as falling demand. It will be difficult to replace the drop-down import: devaluation and import falling during the 1998 crisis had speeded up domestic enterprises by means of previously unused capacities, but now this resource is limited.

Referring to the rating of the most important trade partners excluding commercial unions. China takes the first place (88,4 bln US Dollars), Netherlands takes the second (73,3 bln US Dollars), and Germany is the third (70,1 bln US Dollars).

External turnover with the neighboring Ukraine fell by 29,6% (to 27,9 bln US Dollars). The negative trend of indexes rapid reduction will clearly continue in 2015. Despite of imposed sanctions, trade with the USA has increased by 5,5% in 2014 (up to 29,2 bln US Dollars).

| № | Partner countries | Foreign trade volume of the RF for 2014, bln US Dollars | Increase (reduction) comparing to 2013, % | Share of external turnover to the total, % |

| Total | 783 453,7 | -7,0 | 100 | |

| EU | 377 390,5 | -9,6 | 48,2 | |

| 1 | China | 88 373,4 | -0,5 | 11,3 |

| 2 | Netherlands | 73 284,0 | -3,5 | 9,4 |

| 3 | Germany | 70 087,6 | -6,5 | 8,9 |

| 4 | Italy | 48 471,2 | -10,0 | 6,2 |

| 5 | Turkey | 31 620,3 | -3,4 | 4,0 |

| 6 | Belarus | 31 511,3 | -7,8 | 4,0 |

| 7 | Japan | 30 793,9 | -7,3 | 3,9 |

| 8 | USA | 29 146,2 | 5,5 | 3,7 |

| 9 | Ukraine | 27 862,3 | -29,6 | 3,6 |

| 10 | South Korea | 27 300,2 | 8,5 | 3,5 |

At the same time Russia has begun phased trade flow redistribution to Asian, African and Latin American countries. Among the main partner countries with total turnover of more than 3 bln dollars, Singapore is on top (see table 2) in term of its growth (+152,5% to 2013); Egypt takes the second place (+86%).

| № | Partner countries | Growth of foreign trade volume of the RF to 2013, % | Foreign trade volume, mln US Dollars |

| 1 | Singapore | 152,5 | 6 156,2 |

| 2 | Egypt | 86,0 | 5 478,7 |

| 3 | Denmark | 23,2 | 4 506,9 |

| 4 | Malaysia | 22,7 | 3 297,0 |

| 5 | Latvia | 19,8 | 13 450,4 |

| 6 | Thailand | 18,7 | 3 986,5 |

| 7 | Brazil | 15,7 | 6 335,5 |

| 8 | Azerbaijan | 12,0 | 4 009,1 |

| 9 | Estonia | 10,7 | 5 326,9 |

| 10 | Belgium | 8,8 | 12 798,7 |

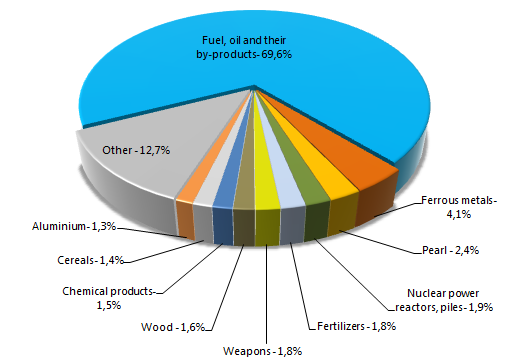

The structure of the Russian export remains uniform and is based on depleting resources. Excluding oil and gas the country imports ferrous metals (4,1% of total export in monetary terms), precious and semiprecious stones, pearl (2,4%), hi-tech equipment for nuclear power industry (1,9%), fertilizers (1,8%), weapons (1,8%), wood (1,6%), products of chemical industry (1,5%), cereals (1,4%), aluminum (1,3%) and other items (12,7%).

Figure 1. Structure of the Russian export in monetary terms, 2014, %

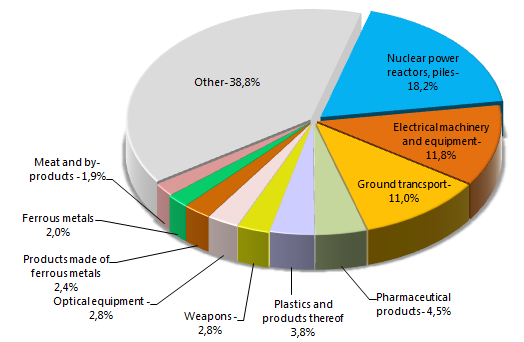

The structure of the Russian import is not so uniform. Russia purchases a wide range of products, mainly equipment for power industry (18,2% of total import in monetary terms), electrical machinery and equipment (11,8%), lorries and cars (11%), medicines (4,5%), plastics (3,8) and other (see figure 2).

Figure 2. Structure of the Russian import in monetary terms, 2014, %

According to the experts of the Credinform information agency, the reduction of foreign trade volume will continue next year, but as a temporary thing. Growth recovery in 2016 will be possible at exchange and economic climate stabilization and greater credit resources access. Today Russia finds new trade partners and discovers new markets, despite of external constraints. Isolation, being discussed by some Western countries’ leaders, doesn’t happen.

For all information on Russian and foreign enterprises, as well as analytical reports on various economic sectors you can refer to our Custom Service Department specialists:

+7 (812) 406 8414 (Saint-Petersburg), +7 (495) 640 4116 (Moscow).