Order a report

Custom-made industry research, company ratings, competitor analysis

Is it worth expecting for the economic recession?

The escalated geopolitical environment in the events surrounding Ukraine provided a large dose of pessimism to many experts in making an assessment of the national economic growth prospects. The Occident’s sanctions have had an impact on worsening of the not very good investment climate as it was. The capital outflow has increased and according to the Ministry of Finance of the Russian Federation it will be 100 bln dollars in the current year. The devaluation of the ruble at the beginning of the year against the Central Bank’s dollar-euro basket broke up the inflationary developments. The raising of the key discount rate up to 7.5% by the Central Bank has dampened the market for a little bit, but now this solution is the drag for a new impulse to development. What is worth expecting for against the background of these events in the current year?

“The Ministry of Finance of the Russian Federation admits the technical recession in the 2nd and 3rd quarters of the 2014”, says Maxim Oreshkin, the director of division of the long-term strategic planning of The Ministry of Finance.

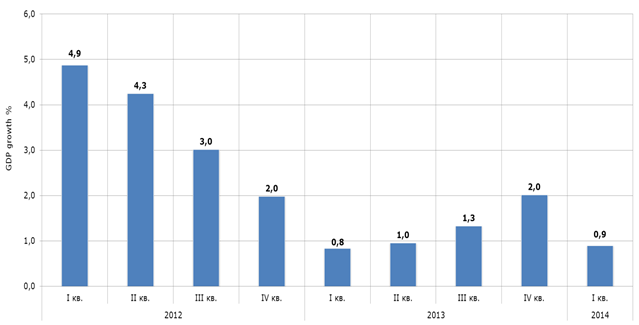

However, not everything is so decisive. On May 15 the Russian Federal State Statistics Service estimated the GDP growth dynamics in the 1st quarter of 2014 at 0.9% that turned out to be 0.1% more than The Ministry of Economic Development and Trade expected in their previous calculation. According to Andrey Klepach, the deputy economics minister, there was not and will be no recession in the economy. There will be lower point in the 1st quarter and taking into account the gradual settlement of a dispute in Ukraine and the sanctions war damping we should expect for its growth acceleration.

Russian GDP growth by quarter, %

There are a number of other facts for the easing of this situation: as on May 20, the Russian stock market has almost won back lost positions in February and April of the current year, caused by the investors panic because of the actions of Russia in Crimea.

Moreover, according to the last estimating of the Russian Federal State Statistics Service in January and April the run-up of the manufacturing output set up 1.4% to January and April in 2013, compared with the same period in the last year there was the industrial recession to -0.6%.

It is gratifying to emphasize that in the considered time-horizon of the current year the manufacturing increased to 2.8%, last year there was the recession to -0.9%.

To sum up, according to our provisional estimate the economy growth at year-end may be 0.6% more than The Ministry of Finance of the Russian Federation considered earlier.