Order a report

Custom-made industry research, company ratings, competitor analysis

Development of the Patent system of taxation in 2016

We have already discussed in our publications the patent system of taxation: «Patent system of taxation in 2015».

According to the Federal Laws of 21.07.2014 №244-FL and of 13.07.2015 №232-FL, individual entrepreneurs whose average number of wage workers is not more than 15 employees for the tax period and that sales income amount does not exceed 60 mln RUB, can use the patent system of taxation. These requirements remain unchanged in 2016.

Changes in the application rules of the patent system of taxation concerned in 2016 the kinds of activity list that was raised from 47 to 63 kinds of activity. You can learn full list of activity kinds in the Tax Code of the RF and on the web-site of the Federal Tax Service of the RF.

For example, the following kinds of activity were included to the new list that came into force since January 1, 2016: caring for retired and disabled people, activities related to computer hardware, manufacture and repair of goods made of natural leather, manufacture of bakery, confectionary and dairy products.

As before, in order to account for the tax authorities, it is necessary to keep the income ledger.

In 2016 the growing popularity of the patent system of taxation among individual entrepreneurs was not once mentioned by the mass media. For example, almost 40 thousand patents were acquired for the first half of 2016 in Moscow that is 80% more than for the 6 months of the previous year. Besides, more than half of patents are related to the sphere of retail trade. Growing interest is observed for patents on the right to carry out activities related to public food services, home renovation and other services.

As a result, according to experts, patent system as one of kinds of simplified taxation system becomes ever more effective instrument of tax policy of the Government.

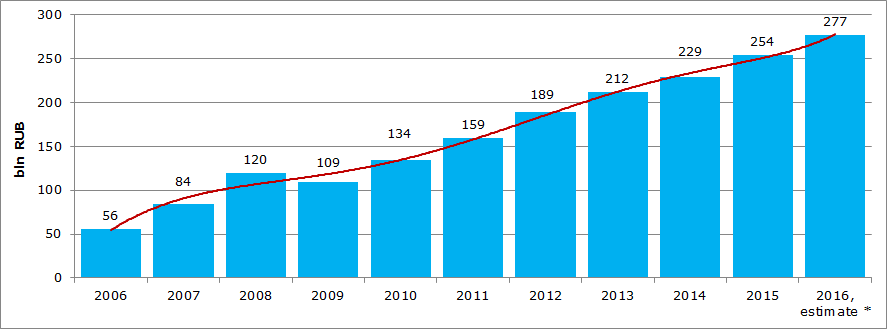

Data from the Federal Tax Service of the RF of assessment and collection of taxes imposed with implementation of the simplified taxation system (Picture 1) confirm the above-mentioned information.

*) – the forecast is based on growth rates for 6 months of 2016

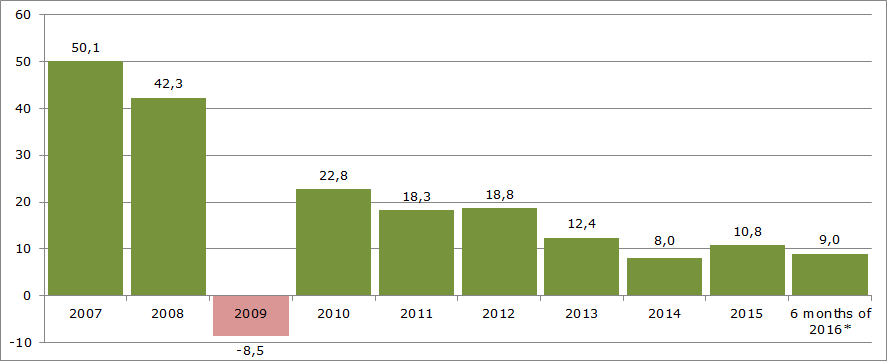

Besides, growth rates of collection of such taxes are recently decreasing because of the macroeconomic situation (Picture 2).

*) – data for 6 months of 2016 are given to the corresponding period of 2015