Order a report

Custom-made industry research, company ratings, competitor analysis

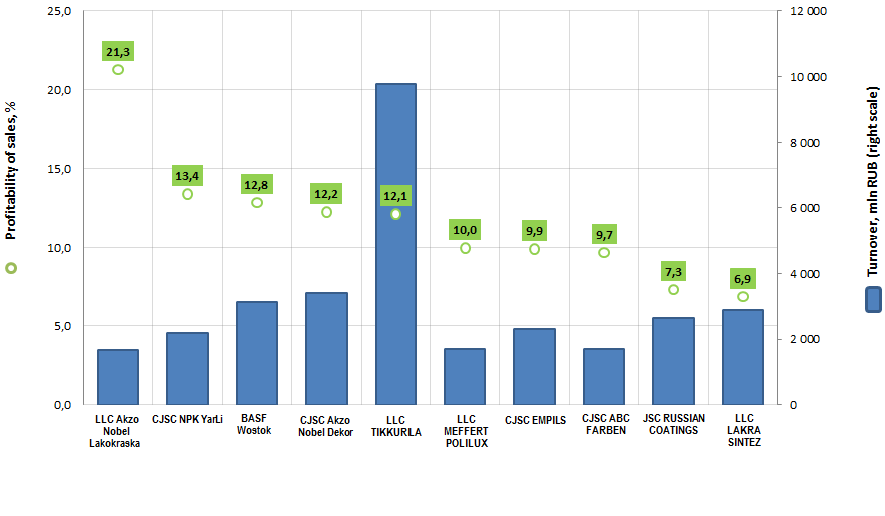

Profitability of sales of the largest paints and varnishes manufacturers in Russia

Information Agency Credinform has prepared the ranking of the largest Russian paints and varnishes manufacturers.

Top-10 enterprises in terms of annual revenue were selected according to the data from the Statistical Register for the latest available period (for the year 2014). The enterprises were ranked by decrease in profitability of sales. Besides, profit dynamics relative previous financial period and solvency index GLOBAS-i® are also represented (see table 1).

Profitability of sales (%) is the share of operating profit in the sales volume of the company.

The ratio characterizes the most important aspect of company’s activity - the efficiency of the industrial and commercial activity and shows the company’s funds, which are remained after covering the cost of production, interest and tax payments.

Profitability of sales is an indicator of the company’s price policy and shows its ability to control the expenses. Differences in competitive strategies and product lines cause a substantial range of ratio values. Therefore it should be taken into account, that at equal values of revenue, operational expenses and profit before tax, the profitability of sales ratio of two companies can be significantly different, due to the influence of interest payments on net profit.

| № | Name | Region | Revenue,mln RUB, 2014 | Revenue growth, % | Profitability of sales, % | Solvency index GLOBAS-i® |

|---|---|---|---|---|---|---|

| 1 | LLC Akzo Nobel Lakokraska INN 5034019048 |

Moscow region | 1 662 | 28,7 | 21,3 | 200 high |

| 2 | CJSC NPK YarLi INN 7602003918 |

Yaroslavl region | 2 193 | 13,7 | 13,4 | 183 the highest |

| 3 | Gesellschaft mit beschraenkter Haftung BASF Wostok INN 7710317252 |

Moscow region | 3 127 | -0,5 | 12,8 | 193 the highest |

| 4 | CJSC Akzo Nobel Dekor INN 5001027607 |

Moscow region | 3 418 | 10,4 | 12,2 | 193 the highest |

| 5 | LLC TIKKURILA INN 7816424590 |

Saint-Petersburg | 9 775 | 3,0 | 12,1 | 221 high |

| 6 | LLC MEFFERT POLILUX INN 5041024497 |

Moscow region | 1 711 | 17,3 | 10,0 | 304 satisfactory |

| 7 | CJSC EMPILS INN 6167008343 |

Rostov region | 2 315 | -2,8 | 9,9 | 253 high |

| 8 | CJSC ABC FARBEN INN 3618003426 |

Voronezh region | 1 692 | 12,4 | 9,7 | 223 high |

| 9 | JSC RUSSIAN COATINGS INN 7605015012 |

Yaroslavl region | 2 628 | 1,0 | 7,3 | 209 high |

| 10 | LLC LAKRA SINTEZ INN 7702177932 |

Moscow region | 2 891 | 7,6 | 6,9 | 199 the highest |

According to 2014 financial results, the average value of profitability of sales ratio of Top-10 enterprises is 11,5%; the highest value is 21,3 % (LLC Akzo Nobel Lakokraska), the lowest value is 6,9% (LLC LAKRA SINTEZ).

The ratio of the industry leader LLC TIKKURILA is above average (12,1%).

Tikkurila concern started its activity in Russia in the 1980-ies, the company exported industrial coatings. In 1990-ies Tikkurila became the first western company, which presented the paint tinting system in Russia. In 1995 Tikkurila opened first European paint plant in Russia.

Today LLC Tikkurila is represented by four industrial areas, which are located in Saint-Petersburg and Stary Oskol: three plants produce decorative paints and varnishes under Tikkurila, Fincolor, TEKS trademarks and one plant produces paints and varnish materials for industrial purposes.

According to 2014 results, the annual revenue of Top-10 enterprises amounted to 31,4 bln RUB; total turnover of Top-10 enterprises increased by 6,2% in the reporting period.

According to 2015 results, 811 ths tons of paints and varnishes based on polymers were produced in Russia (-6% to 2014 level); 420 ths tons of paints and varnishes (+4,5%) and 28,7 ths tons of synthetic organic dyes and colored varnishes (+15,1%).

All enterprises (except LLC MEFFERT POLILUX with net loss in the reporting period) demonstrated high and the highest solvency index GLOBAS-i®, that is a sign of good company’s solvency to investor or partner.