Order a report

Custom-made industry research, company ratings, competitor analysis

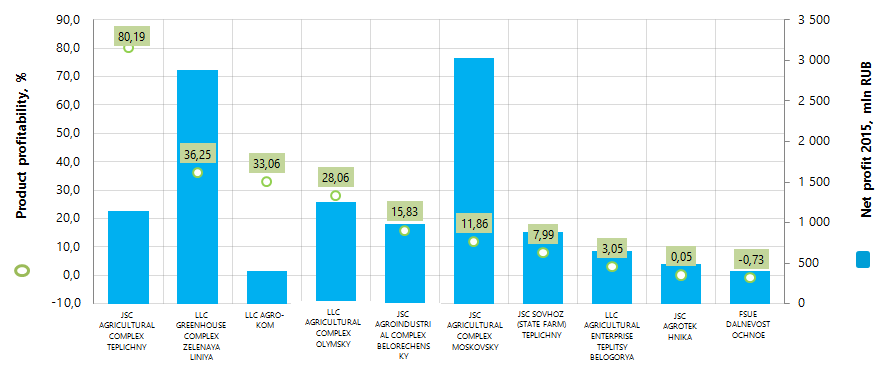

Product profitability of vegetable production enterprises

Information agency Credinform presents a ranking of the largest Russian vegetable production enterprises in terms of product profitability ratio.

The companies with the highest volume of revenue (TOP-10) were selected for this ranking according to the data from the Statistical Register for the latest available period (2015). These enterprises were ranked by decrease in product profitability ratio. (Table 1).

Product profitability is calculated as the ratio of sales profit to expenses from ordinary activities. In general, profitability reflects the economic efficiency of production. Product profitability analysis allows us to make a conclusion whether output of one or another product is reasonable. There are no prescribed values for indicators of this group, because they vary strongly depending on the industry.

For the most full and fair opinion about the company’s financial position, not only product profitability rate should be taken into account, but also the whole set of financial indicators and ratios.

| Name, INN, region | Net profit 2015, mln RUB | Revenue of 2015, mln RUB | Revenue of 2015 to 2014, %% | Product profitability of 2014, % | Product profitability of 2015, % | Solvency index Globas-i |

|---|---|---|---|---|---|---|

| JSC AGRICULTURAL COMPLEX TEPLICHNY ИНН 2312036895 Krasnodar territory |

502,4 | 1 140,0 | 119 | 62,09 | 80,19 | 233 High |

| LLC GREENHOUSE COMPLEX ZELENAYA LINIYA INN 7826084060 Krasnodar territory |

836,7 | 2 877,3 | 244 | 17,90 | 36,25 | 223 High |

| LLC AGRO-KOM INN 0701002574 The Kabardino-Balkar Republic |

71,1 | 404,6 | 94 | 62,36 | 33,06 | 281 High |

| LLC AGRICULTURAL COMPLEX OLYMSKY INN 4608005786 Kursk region |

281,6 | 1 250,0 | 129 | 61,67 | 28,06 | 212 High |

| JSC AGROINDUSTRIAL COMPLEX BELORECHENSKY INN 6639009424 Sverdlovsk region |

134,0 | 977,8 | 100 | 12,95 | 15,83 | 202 High |

| JSC AGRICULTURAL COMPLEX MOSKOVSKY INN 5003003432 Moscow |

159,4 | 3 026,7 | 96 | 19,23 | 11,86 | 246 High |

| JSC SOVHOZ (STATE FARM) TEPLICHNY INN 6501254511 Sakhalin region |

122,5 | 887,7 | 122 | 6,11 | 7,99 | 220 High |

| LLC AGRICULTURAL ENTERPRISE TEPLITSY BELOGORYA INN 3123227670 Belgorod region |

380,6 | 645,8 | 178 | -17,13 | 3,05 | 320 Satisfactory |

| JSC AGROTEKHNIKA INN 4716002207 Leningrad region |

-50,5 | 486,9 | 79 | 10,10 | 0,05 | 550 Unsatisfactory |

| FSUE DALNEVOSTOCHNOE INN 2502003633 Primorie territory |

2,4 | 407,6 | 113 | -5,16 | -0,73 | 245 High |

JSC AGRICULTURAL COMPLEX TEPLICHNY has shown the highest product profitability ratio 80,19%. Enterprise with the largest revenue for 2015 - JSC AGRICULTURAL COMPLEX MOSKOVSKY takes sixth place of the ranking. Its share in total revenue volume of TOP-10 companies is 25%. This enterprise turned out to be among three companies of the TOP-10 list, showing decrease in profit and revenue of 2015 compared to the previous year. FSUE DALNEVOSTOCHNOE has got negative values of product profitability both in 2014 and in 2015.

Summarizing the financial and other indicators, eight out of TOP-10 companies have got high solvency index Globas-i. This demonstrates their ability to pay off the debts in time and to the full extent.

LLC AGRICULTURAL ENTERPRISE TEPLITSY BELOGORYA has got satisfactory solvency index Globas-i due to the information about company being a defendant in debt collection arbitration proceedings.

JSC AGROTEKHNIKA has got unsatisfactory solvency index Globas-i due to the information about bankruptcy claim as well as being a defendant in debt collection arbitration proceedings.

The average product profitability value among TOP-10 companies in 2015 is 21,56%, compared to 23,01% in 2014 . Four enterprises shown decrease in product profitability value.

Total revenue volume of TOP-10 companies in 2015 is 12,1 bln RUB, that is 24% higher than in 2014. Total net profit of this group for the same period increased more than 86%.

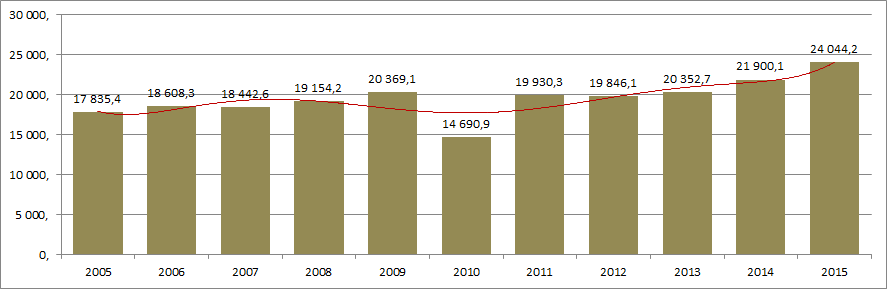

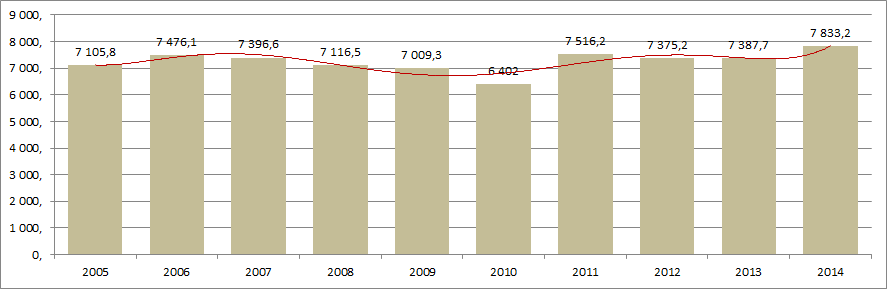

In general, enterprises operate profitably. The industry demonstrates positive dynamics in vegetables production, that is proved by the data of the Federal State Statistics Service (Rosstat)(Picture 2,3).

Vegetables producing companies are located in regions with the best environment for agricultural production and also attracted to the largest distribution areas – Moscow and Saint-Petersburg. According to the data of the Information and analytical system Globas-i, 100 largest companies in terms of revenue volume for 2014 are registered in 44 regions. Most of them are registered in the following regions (TOP-6 regions):

| Region | Number of companies |

|---|---|

| Moscow region | 10 |

| Bryansk region | 7 |

| Samara region | 6 |

| The Republic of Bashkortostan | 5 |

| Leningrad region | 4 |

| Stavropol territory | 4 |