Order a report

Custom-made industry research, company ratings, competitor analysis

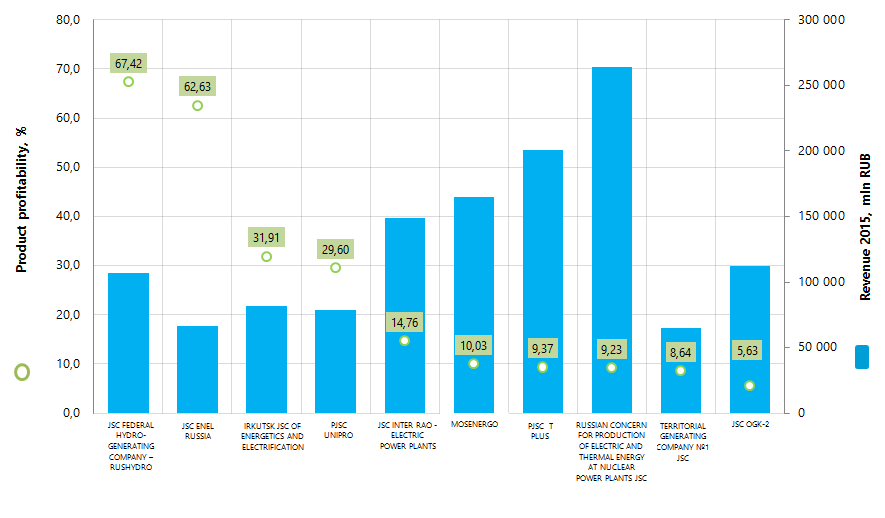

Product profitability of the largest energy producers in Russia

Information agency Credinform presents the ranking of the largest energy producers in Russia on product profitability ratio.

The largest by revenue energy producers (TOP-10) for the last available in the open sources period (2015) were taken for the ranking. Further the companies were ranked in the descending order of product profitability value (Table 1).

Product profitability is calculated as a ratio of profit on sales to operational expenses. In the whole the profitability reflects the production efficiency. The analysis of product profitability allows making a conclusion on release usefulness of various products. There aren’t any recommended values for this group, due to the fact that they differ greatly depending on industry.

| Name, Tax number, Region | Net profit (loss) 2015, mln RUB | Revenue 2015, mln RUB. | Sales revenue 2015 to 2014,% | Product profitability 2015, % | Solvency index Globas-i |

|---|---|---|---|---|---|

| JSC FEDERAL HYDRO-GENERATING COMPANY – RUSHYDRO Tax number 2460066195 Krasnoyarsk territory |

30 022,0 | 107 099,0 | 99 | 67,42 | 207 High |

| JSC ENEL RUSSIA Tax number 6671156423 Sverdlovsk region |

-1 803,0 | 66 197,0 | 89 | 62,63 | 262 High |

| IRKUTSK JSC OF ENERGETICS AND ELECTRIFICATION Tax number 3800000220 Irkutsk region |

12 633,4 | 81 960,5 | 134 | 31,91 | 205 High |

| PJSC UNIPRO Tax number 8602067092 Khanty-Mansiisk autonomous district - Yugra |

15 545,7 | 78 618,8 | 98 | 29,60 | 165 Prime |

| JSC INTER RAO - ELECTRIC POWER PLANTS Tax number 7704784450 Moscow |

-3 306,6 | 149 129,3 | 101 | 14,76 | 267 High |

| MOSENERGO Tax number 7705035012 Moscow |

6 411,0 | 164 508,2 | 104 | 10,03 | 189 Prime |

| PJSC T PLUS Tax number 6315376946 Moscow region |

281,1 | 200 438,2 | 257 | 9,37 | 320 Satisfactory |

| RUSSIAN CONCERN FOR PRODUCTION OF ELECTRIC AND THERMAL ENERGY AT NUCLEAR POWER PLANTS JSC Tax number 7721632827 Moscow |

13 921,6 | 263 756,6 | 104 | 9,23 | 202 High |

| TERRITORIAL GENERATING COMPANY №1 JSC Tax number 7841312071 Saint-Petersburg |

2 676,1 | 65 183,6 | 100 | 8,64 | 217 High |

| JSC OGK-2 Tax number 2607018122 Stavropol territory |

3 001,7 | 112 115,7 | 97 | 5,63 | 224 High |

RUSSIAN CONCERN FOR PRODUCTION OF ELECTRIC AND THERMAL ENERGY AT NUCLEAR POWER PLANTS JSC received the largest revenue in the industry in 2015. This enterprise is placed on the seventh spot by product profitability. The company’s share in the total revenue volume of the TOP-10 companies amounted to a little more than 20%.

JSC FEDERAL HYDRO-GENERATING COMPANY – RUSHYDRO shows the largest product profitability as well as decrease of revenue and net profit in 2015 in comparison with the previous period.

Following the results of 2015, three more companies of the TOP-10 face the decrease of revenue. Decrease of net profit or loss was shown by five more enterprises.

In the whole nine companies of the TOP-10 were given the prime or high solvency index Globas-i by the complex of financial and non-financial indicators. It gives evidence to their ability to meet the debt obligations timely and in full.

PJSC T PLUS was given the satisfactory solvency index Globas-i, due to the information about company being a defendant in debt collection arbitration proceedings, as well as in arbitration cases of bankruptcy.

The average value of product profitability in the TOP-10 group in 2015 amounted to 24,92%, which is greater than the indicator of 2014 amounted to 19,79%.

The total revenue volume of the TOP-10 for 2015 amounted to 1 289 billion RUB, which is by 13% greater than the same indicator for 2014 whereas the total net profit for the same period decreased by 7%.

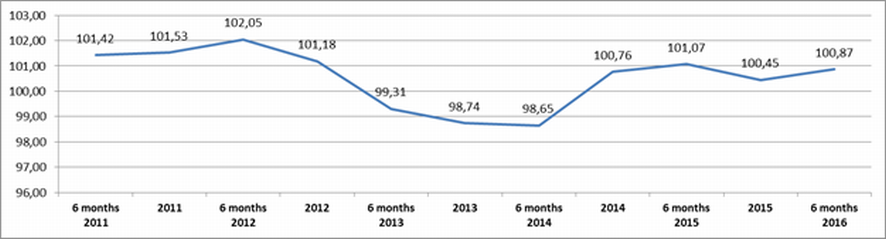

In the whole enterprises of the industry operate profitably. The industry shows the positive dynamic of energy production. According to the Federal State Statistics Service (Rosstat), 1 063 420, 72 mln kilowatt-hours of energy were produced in 2015. It gave Russia the possibility to take the forth place by this indicator, after China, the USA and India, according to Global Energy Statistical Yearbook © Enerdata. The dynamic of energy production in Russia, according to Rosstat, is represented in the Figure 2.