Order a report

Custom-made industry research, company ratings, competitor analysis

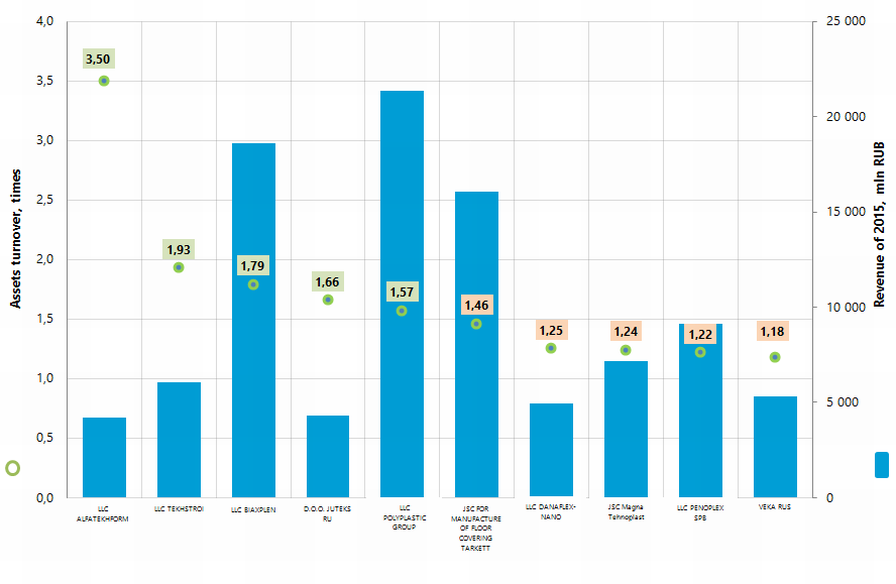

Assets turnover of the largest Russian manufacturers of plastic goods

Information Agency Credinform presents a ranking of the largest Russian manufacturers of plastic goods (except for manufacturers of plastic package). The largest enterprises of the industry (TOP-10) in terms of annual revenue were selected according to the data from the Statistical Register for the latest available periods (2015 and 2014). Then the companies were ranked by assets turnover ratio (Table 1).

Assets turnover (times) is the ratio of sales revenue and company’s average total assets for a period. It characterizes the effectiveness of using of all available resources, regardless the source of their attraction. The ratio shows how many times per year the full cycle of production and circulation is performed, generating the corresponding effect in the form of profit.

Taking into account the actual situation both for the economy in general and in industries, experts of the Information agency Credinform developed and realized in the Information and Analytical system Globas® calculation of actual values of financial ratios that can be normal for the particular industry. For plastic good manufacturers companies practical value of the net profit ratio in 2015 was from 1,47.

For the most full and fair opinion about company’s financial position not only the compliance with standard values, but the whole set of financial indicators and ratios should be taken into account.

| Name , INN, region | Net profit of 2015, mln RUB | Revenue of 2015, mln RUB | Revenue of 2015 to 2014, % | Assets turnover, times | Solvency index Globas® |

| LLC ALFATEKHFORM INN 7705195785 Moscow | 183,2 | 4 226,6 | 30,2 | 3,50 | 196 High |

| LLC TEKHSTROI INN 7743944097 Moscow | 47,3 | 6 076,1 | 218,3 | 1,93 | 212 High |

| LLC BIAXPLEN INN 5244013331 Nizhniy Novgorod region | 1 887,3 | 18 619,0 | 52,7 | 1,79 | 204 High |

| D.O.O. JUTEKS RU INN 3315010390 Vladimir region | 354,0 | 4 310,8 | 6,3 | 1,66 | 210 High |

| LLC POLYPLASTIC GROUP INN 5021013384 Moscow | 1 130,6 | 21 334,7 | 5,4 | 1,57 | 193 The highest |

| JSC FOR MANUFACTURE OF FLOOR COVERING INN 6340007043 Samara region | 683,0 | 16 034,7 | -9,0 | 1,46 | 232 High |

| LLC DANAFLEX-NANO INN 1655177480 The Republic of Tatarstan | 309,5 | 4 970,3 | 54,8 | 1,25 | 232 High |

| JSC Magna Tehnoplast INN 5256076921 Nizhniy Novgorod region | 57,0 | 7 163,8 | -12,6 | 1,24 | 260 High |

| LLC PENOPLEX SPB INN 7825133660 Saint Petersburg | -1,7 | 9 105,1 | 19,1 | 1,22 | 274 High |

| LLC VEKA RUS INN 7728165949 Moscow | 25,9 | 5 296,7 | -6,2 | 1,18 | 245 High |

| Total for TOP-10 group of companies | 4 676,0 | 97 137,8 | |||

| Total for TOP-500 group of companies | 8 930,8 | 397 796,3 | |||

| Average value within group of TOP-10 companies | 467,6 | 9 713,8 | 15,7 | 1,68 | |

| Average value within group of TOP-500 companies | 17,9 | 795,6 | 18,4 | 3,41 | |

| Average value within industry | 1,3 | 72,6 | 4,2 | 1,47 |

In 2015 average values of the assets turnover ratio within TOP-10 and TOP-500 group of companies is higher than the practical value. Five companies from TOP-10 group have indicators that are lower than the practical values and another five have indicators higher than practical values (marked with green and yellow filling, correspondently, in Picture 1).

Picture 1. Assets turnover ratio and revenue of the largest Russian manufacturers of plastic goods (TOP-10)

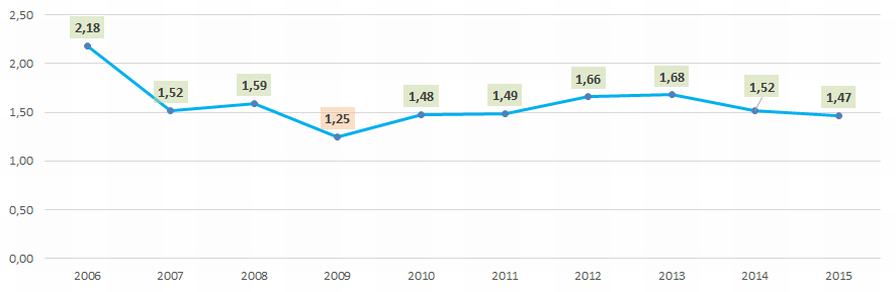

Picture 1. Assets turnover ratio and revenue of the largest Russian manufacturers of plastic goods (TOP-10)Average industrial values of the assets turnover ratio (Picture 2) in general show macroeconomic situation decreasing during crisis periods.

Picture 2. Average industrial values of the assets turnover ratio of Russian manufacturers of plastic goods in 2006 – 2015

Picture 2. Average industrial values of the assets turnover ratio of Russian manufacturers of plastic goods in 2006 – 2015All TOP-10 companies have got the highest or high solvency index Globas®, that shows their ability to meet their obligations in time and fully.

Five companies out of the TOP-10 group in 2015 decreased indicators of revenue or net profit (have loss) compared to the previous period (marked with red filling in the Table 1).