Order a report

Custom-made industry research, company ratings, competitor analysis

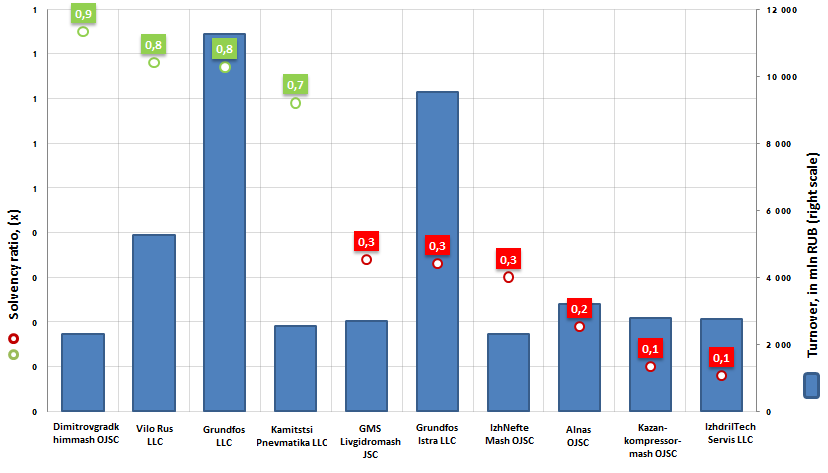

Solvency ratio of the largest manufacturers of pumping equipment

Information agency Credinform prepared a ranking of the largest Russian companies, producing pumping equipment.

The TOP-10 list of enterprises was drawn up for the ranking on the volume of annual revenue, according to the data from the Statistical Register for the latest available period (for the year 2014).

Solvency ratio (х) is the relation of own capital to the balance sum. It shows company’s dependence on foreign loans.

Recommended value is: >0,5.

If the parameter has dropped below the minimum permissible limit, than it means that a company is highly dependent on external sources of borrowings, and by the worsening of conjecture in the market it may lead to liquidity crisis, to unstable financial position.

For getting of the most comprehensive and fair picture of the financial standing of an enterprise it is necessary to pay attention not only to industry-average indicators, but also to all presented combination of financial indicators and company’s ratios.

| № | Name | Registration area | Revenue, in mln RUB, for 2014 | Solvency ratio, (х) | Solvency index GLOBAS-i® |

|---|---|---|---|---|---|

| 1 | Dimitrovgradkhimmash OJSC INN 7302000070 |

Ulyanovsk region | 2 317 | 0,9 | 192 the highest |

| 2 | Vilo Rus LLC INN 7702176142 |

Moscow | 5 267 | 0,8 | 178 the highest |

| 3 | Grundfos LLC INN 5042054367 |

Moscow | 11 249 | 0,8 | 159 the highest |

| 4 | Kamitstsi Pnevmatika LLC INN 7710028420 |

Moscow | 2 541 | 0,7 | 192 the highest |

| 5 | GMS Livgidromash JSC INN 5702000265 |

Orel Region | 2 685 | 0,3 | 271 high |

| 6 | Grundfos Istra LLC INN 5017047704 |

Moscowregion | 9 510 | 0,3 | 272 high |

| 7 | IzhNefteMash OJSC INN 1835012826 |

Udmurt Republic | 2 301 | 0,3 | 229 high |

| 8 | Alnas OJSC INN 1607000081 |

Republic of Tatarstan | 3 198 | 0,2 | 271 high |

| 9 | Kazankompressormash OJSC INN 1660004878 |

Republic of Tatarstan | 2 775 | 0,1 | 290 high |

| 10 | IzhdrilTechServis LLC INN 1831114320 |

Udmurt Republic | 2 762 | 0,1 | 221 high |

The solvency ratio of the leading manufacturers of pumping equipment (top-10) ranges from 0,1 (IzhdrilTechServis LLC) up to 0,9 (Dimitrovgradkhimmash OJSC).

Thus, a number of companies got shortlisted in the Top-10 list has a high degree of dependence on borrowed funds (the solvency ratio is less than 0,5). Their capital doesn’t cover the amount of obligations incurred, and by one-time claiming credit amounts the enterprises will have difficulties with their repayment. Therefore, business needs to maintain a balance between the desire to expand its presence in the market and the ability to cope with a high debt load.

Picture 1. Solvency ratio and revenue of the largest Russian manufacturers of pumping equipment (TOP-10)

Annual revenue of the TOP-10 companies, according to the latest published annual financial statement (for 2014), made 44,6 bln RUB, that is by 11,4% higher than the revenue of the same enterprises for the previous reporting period (40 bln RUB).

The largest company in the industry – Grundfos LLC – shows good financial results, including in terms of solvency level: the ratio of capital sum to the volume of borrowed funds is 0,8, that points to a rather low dependence of the firm on foreign loans.

The company Grundfos is the world leader in the production of high-tech pumping equipment and sets the trends in the sphere of water technology.

The pumps Grundfos have been known to domestic consumers since 60-ies of the last century. The representation of the concern in Moscow was opened in 1992. In 1998 was found the subsidiary Grundfos LLC.

Consistent high quality of products, reliability and energy efficiency of manufactured pumps, as well as well-developed network of branches and service centers in the regions of Russia help the company maintain the leadership position in the market of pumping equipment.

In 2005 it was completed the construction of the first stage of the plant «Grundfos Istra». Own production allows to produce high-quality pumps on the territory of Russia, as well as to reduce delivery times and logistical costs of customers. Today the total area of the factory is 30 000 sq. m.

Several types of equipment are set up in the plant: vertical, centrifugal, cantilever-monoblock pumps with variable-frequency motors; water booster systems and fire-fighting units; control cabinets.

The pumps Grundfos are working in water and wastewater treatment plants of Moscow, St. Petersburg, Rostov-on-Don, Voronezh, Khabarovsk, Syktyvkar, Podolsk, Ivanovo, Yaroslavl and a number of other cities. Also, company’s equipment has been installed on objects of housing and communal services and the largest industrial enterprises of Russia, on life-support systems of airports and sports facilities.

This one and other participants of the ranking of the largest TOP-10 manufacturers of pumping equipment got high and the highest solvency index. This fact points to companies’ ability to pay off their debts in time and fully, while risk of default is minimal.